It looks like you're new here. If you want to get involved, click one of these buttons!

*snip*

In his previous interviews he mentioned that bank loans (or floating rate bonds) are attractive because of their high yield (3%) and short duration (1-2 years). Even though bank loans are rated junk, they are safer because they are high in capital structure in case of the banks defaulting on the loans. Also he mentioned that utilities are attractive and stable while offer 3-4% yield.

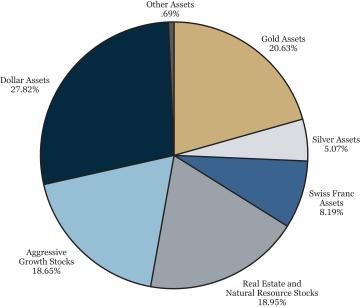

Good question, Without digging thru the latest report, I’m pretty confident the gold and silver reflected on the chart below are in bullion or certificates of ownership representing each. It’s possible they also hold a few mining stocks, but those would probably be reflected in the “stock“ holdings rather than being listed under gold.Is the gold position in PRPFX, gold metals, or miners, are good hedge against inflation?

You are correct. Giroux has stated in his annual semi-annual reports (within past 1-2 years) that he views bonds as a terrible investment under current conditions. (Not an exact quote - but a close approximation). I don’t pretend to understand his methodology and how he keeps volatility as low as he does. But seems to work for him. Probably playing with some derivatives to hedge bets.One of the portfolio stats that jumped out at me was that bond holdings only accounted for 1.4% of fund assets. I'm a bond novice compared to many here who are able to speak with incredible knowledge, but this fact certainly says much about Giroux's views on bonds. His main focus on bonds for a bit has been short-term high yield, so it seems he's even moved on from that area.

Simplicity itself. Section 852(b)(6) gives RICs (including ETFs) special tax treatment. So striking this section takes away that special treatment. ETFs would no longer be able to divest themselves of gain without owing taxes on the gain.SEC. __17. RECOGNITION OF GAIN ON CERTAIN DISTRIBUTIONS BY REGULATED INVESTMENT COMPANIES.

(a) IN GENERAL.—Section 852(b) is amended by striking paragraph (6).

(b) EFFECTIVE DATE.—The amendments made by this section shall apply to taxable years beginning after December 31, 2022.

Jeffrey Colon, The Great ETF Tax Swindle: The Taxation of In-Kind Redemptions, 122 Penn St. L. Rev. 1 (2017)Throughout the history of U.S. investment companies, in-kind distributions have been exempt from tax at the fund level. As Congress began to limit and finally prohibit in 1986 the tax-free distribution of appreciated property by corporations, it continued to specifically exempt open-end funds from this rule. There is scant discussion in the legislative history for the justification for this exemption or why closed-end funds were not also eligible. Perhaps the simplest explanation for the legislative silence is that when [the tax code was changed to narrow the exemption], in-kind distributions from open-end funds were rare.

© 2015 Mutual Fund Observer. All rights reserved.

© 2015 Mutual Fund Observer. All rights reserved. Powered by Vanilla