It looks like you're new here. If you want to get involved, click one of these buttons!

+1@yogibearbull. Thank you!

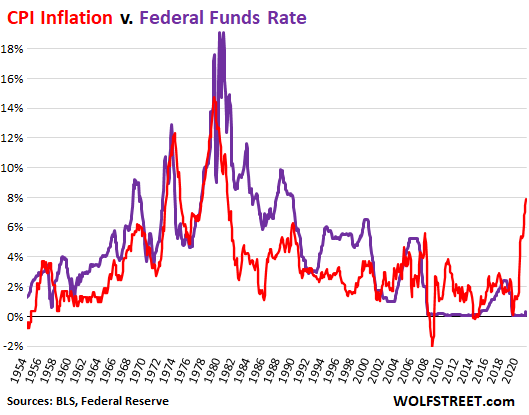

“I daresay you haven’t had much practice. Why, sometimes I’ve believed as many as six impossible things before breakfast.”The Fed lag is a bit hard to look past … with CPI now at 7.9%.

Treasury securities can be bought at new-issue at Treasury Direct & major brokerages (Fidelity, Schwab, etc; commission-free). Treasury publishes general schedules well ahead and makes specific announcements a few days before the new issue. They can also be bought in the secondary market at brokerages.how does one go about buying the 2-yr treasury bonds? By the time we go to buy, they probably go down 10 bps in yield but still will be better than any CDs.

I'm just buying VGSH, good enough for me.how does one go about buying the 2-yr treasury bonds? By the time we go to buy, they probably go down 10 bps in yield but still will be better than any CDs.

© 2015 Mutual Fund Observer. All rights reserved.

© 2015 Mutual Fund Observer. All rights reserved. Powered by Vanilla