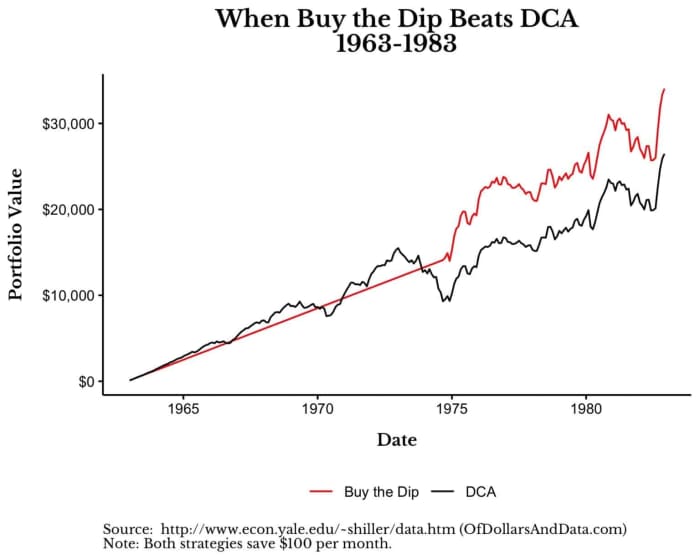

Selling or buying the dip ?! BTD sounds good in theory, but then so does "buy low, sell high". Easier said than done.

1. Where does the cash come from?

2. When does one pull the trigger, i.e. how much does the dip need to be to buy?

The examples below are not intended to "prove" that BTD doesn't work. Sometimes it does, sometimes it doesn't. Obviously if one waits for too large a dip before buying, one is stuck holding cash forever. And if one pulls the trigger on small dips, one risks losing a little bit on most buys - there are frequent small dips that don't bring the market back down to below where you started.

So I'm curious about how people choose their thresholds and where they get their cash.

Here are some sample scenarios starting on Oct 1, 2020 (roughly a year ago), comparing BTD with "buy when cash is available". I use VFIAX as the investment vehicle and market proxy. Red font indicates longer delays (more than a month) before investing on a dip.

For Q1 (where does the cash come from), I have worked through two hypotheticals:

a) One starts with $1200 on Oct 1

b) One has a spare $100 (perhaps from income) at the beginning of each month ($1200 total)

For Q2 (when to buy the dip), I've worked through 1%, 2%, 3%, 4%, 5%, 6%, 7% triggers. There were no dips of 8% or more over the past year.

Lump sum investing: 33.6844% gain on $1200 = $404.21 gain (returns from M*)

Lump sum, invest on dip (on day fund drops specified percentage):

1% dip (Oct 12-Oct 14): 29.4760% gain on $1200 = $353.71 gain

2%, 3% dips (Oct 12 - Oct 19): 31.8043% gain on $1200 = $381.65 gain

4% dip (Oct 12 - Oct 27): 33.1892% gain on $1200 = $398.27 gain

5%, 6%, 7% dips (Oct 12 - Oct 28): 38.0612% on $1200 = $456.73 gain; these are winners

To come out ahead in this time frame with a lump sum and waiting for a dip, one must wait for a 5% - 7% dip. Any faster trigger and one gains less. Any slower trigger, i.e. waiting for an 8%+ dip that never comes, and one is left holding cash and losing out on a $400 gain.

Monthly $100 investing (not waiting for dip):

Oct 1: 33.68% x $100 = $33.68 gain

Nov 2: 36.40% x $100 = $36.40 gain

Dec 1: 23.07% x $100 = $23.07 gain

Jan 4: 21.64% x $100 = $21.64 gain

Feb 1: 19.13% x $100 = $19.13 gain

Mar 1: 15.08% x $100 = $15.08 gain

Apr 1: 11.56% x $100 = $11.56 gain

May 3: 6.87% x $100 = $6.87 gain

June 1: 6.47% x $100 = $6.47 gain

July 1: 3.45% x $100 = $3.45 gain

Aug. 2: 1.78% x $100 = $1.78 gain

Sept. 1: -1.44% x $100 = -$1.44 (loss)

Total gain: $177.69

----------------------

Monthly $100 investing, waiting for a 1% dip:

Oct 1, dip Oct 12-14, 29.48% x $100 = $29.48 gain

Nov 2, dip Nov 16-18, 26.40% x $100 = $26.40 gain

Dec 1, dip Dec 8 -11, 22.97% x $100 = $22.97 gain

Jan 4, dip Jan 8 - 15, 19.38% x $100 = $19.38 gain

Feb 1, dip Feb 12-22, 15.87% x $100 = $15.87 gain

Mar 1, dip March 1 - 3, 17.37% x $100 = $17.37 gain

Apr 1, dip April 16 - 20, 8.39% x $100 = $8.39 gain

May 3, dip May 7 - 10, 6.94% x $100 = $6.94 gain

June 1, dip Jun 14 - 18, 7.30% x $100 = $7.30 gain

July 1, dip July 12 - 16, 3.23% x $100 = $3.23 gain

Aug 2, dip Aug 16 - 18, 1.39% x $100 = $1.39 gain

Sept 1, dip Sep 2 - 10, -0.29% x $100 = - $0.29 (loss)

Total gain: $158.43

----------------------

Monthly $100 investing, waiting for a 2% dip:

Oct 1, dip Oct 12-19, 31.80% x $100 = $31.80 gain

Nov 2, dip Jan 25 - 27, 19.92% x $100 = $19.92 gain

Dec 1, dip Jan 25 - 27, 19.92% x $100 = $19.92 gain

Jan 4, dip Jan 25 - 27, 19.92% x $100 = $19.92 gain

Feb 1, dip Feb 12-25, 17.27% x $100 = $17.27 gain

Mar 1, dip March 1 - 3, 17.37% x $100 = $17.37 gain

Apr 1, dip May 7 - 12, 10.23% x $100 = $10.23 gain

May 1, dip May 7 - 12, 10.23% x $100 = $10.23 gain

June 1, dip Jun 14 - 18, 7.30% x $100 = $7.30 gain

July 1, dip July 12 - 19, 4.89% x $100 = $4.89 gain

Aug 2, dip Sept 2 - 14, 0.30% x $100 = $0.30 gain

Sept 1, dip Sept 2 - 14, 0.30% x $100 = $0.30 gain

Total gain: $159.45

----------------------

Monthly $100 investing, waiting for a 3% dip:

Oct 1, dip Oct 12-19, 31.80% x $100 = $31.80 gain

Nov 2, dip Jan 25 - 29, 21.08% x $100 = $21.08 gain

Dec 1, dip Jan 25 - 29, 21.08% x $100 = $21.08 gain

Jan 4, dip Jan 25 - 29, 21.08% x $100 = $21.08 gain

Feb 1, dip Feb 12-26, 17.82% x $100 = $17.82 gain

Mar 1, dip March 1 - 4, 19.12% x $100 = $19.12 gain

Apr 1, dip May 7 - 12, 10.23% x $100 = $10.23 gain

May 1, dip May 7 - 12, 10.23% x $100 = $10.23 gain

June 1, dip Sept 2 - 20, 2.25% x $100 = $2.25 gain

July 1, dip Sept 2 - 20, 2.25% x $100 = $2.25 gain

Aug 2, dip Sept 2 - 20, 2.25% x $100 = $2.25 gain

Sept 1, dip Sept 2 - 20, 2.25% x $100 = $2.25 gain

Total gain: $161.44

----------------------

Monthly $100 investing, waiting for a 4% dip:

Oct 1, dip Oct 12-27, 33.19% x $100 = $33.19 gain

There are no 4% or greater dips after October, so $1100 remains uninvested

Total gain: $33.19

----------------------

Monthly $100 investing, waiting for 5%, 6%, 7% dip:

Oct 1, dip Oct 12-28, 38.06% x $100 = $38.06 gain

There are no 4% or greater dips after October, so $1100 remains uninvested

Total gain: $38.06

Selling or buying the dip ?! @stillers: "(2) I will continue with stock allocations stretched to the top of my allocation range UNTIL the risk/reward of bond funds, CDs and/or MMkts significantly improves."

Would a rise to say 2.

5 -3.0 % be enough in CD's to peak your interest ?

Derf