It looks like you're new here. If you want to get involved, click one of these buttons!

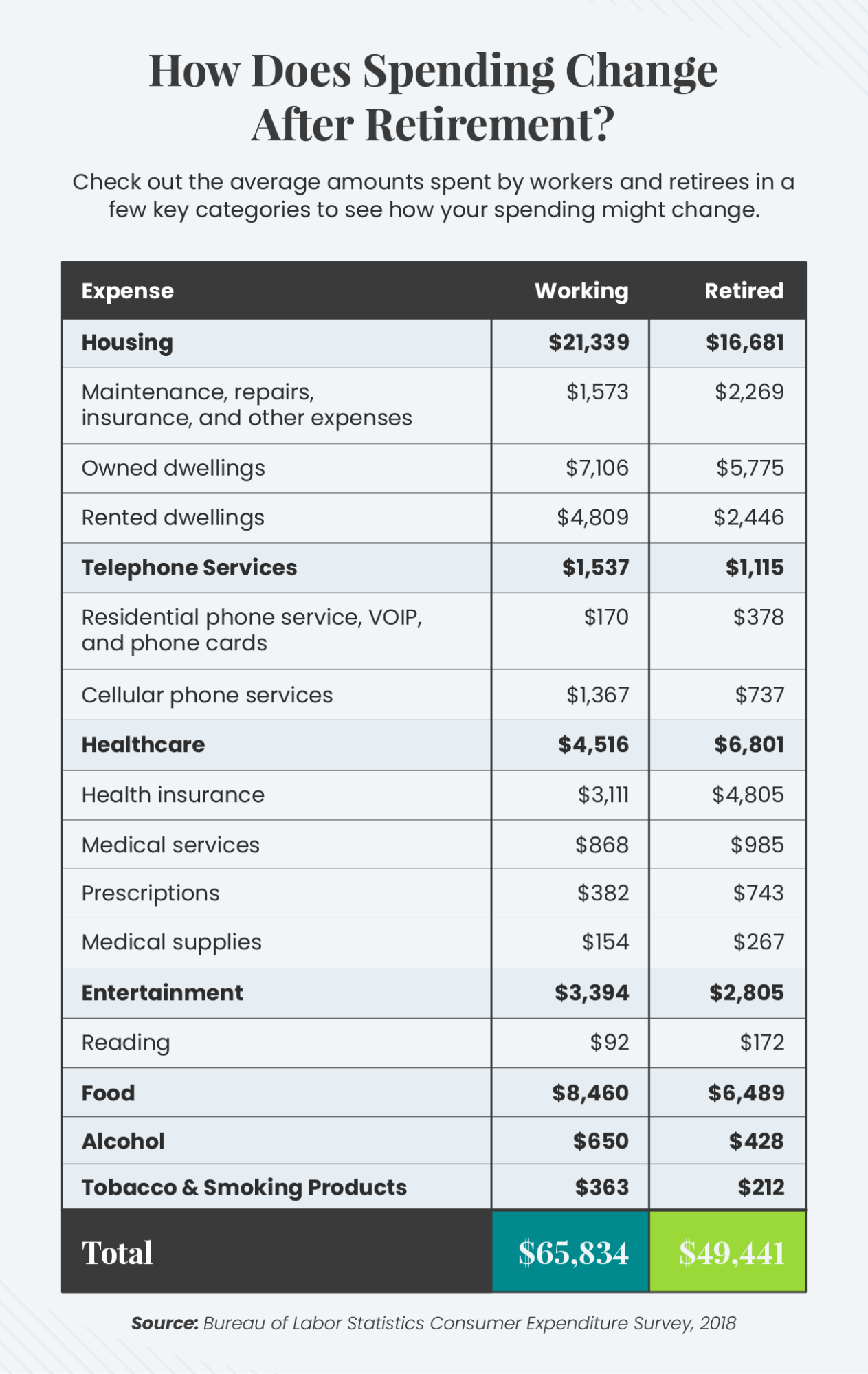

https://annuity.org/retirement/retirement-statistics/Three-quarters of Americans agree the country is facing a retirement crisis, making research around the topic more relevant than ever. We dug into the data on every angle of retirement and compiled the most important statistics below. Read on to learn about what today’s retirees face, from financial challenges to lifestyle decisions and more.

https://www.sec.gov/Archives/edgar/data/1474103/000119312512175846/d296312d485bpos.htmPrior to April 30, 2012, the fund was a series of a corporation named Legg Mason Charles Street Trust, Inc. ... Effective October 5, 2009, ... the fund’s name [was changed] from Global Opportunities Bond Fund to Legg Mason Global Opportunities Bond Fund. Effective May 21, 2010, ... the fund’s name [was changed] from Legg Mason Global Opportunities Bond Fund to Legg Mason BW Global Opportunities Bond Fund.

https://www.sec.gov/Archives/edgar/data/1474103/000119312517331311/d473516d497k.htmEffective December 29, 2017, the fund will be renamed BrandywineGLOBAL – Global Opportunities Bond Fund.

* * * * * *

The change to the fund’s name is being effected as part of a rebranding of Legg Mason funds subadvised by Brandywine Global Investment Management, LLC (“Brandywine Global”). Legg Mason Partners Fund Advisor, LLC continues to serve as the investment manager to the fund, and Brandywine Global continues to serve as subadviser. The fund’s investment objectives, strategies and policies are not changing as a result of the name change.

You might want to explain what you mean by "just as great in its own right." It must include metrics beyond TR but I'm not seeing how any other metrics could cause someone to see these two HYB funds as "equally great."Obviously the Diamond Hill HY team is great, I've been with them for years and very happy. My existing Brandywine fund (LFLAX) has been just as great in its own right.

You might want to check that...Futures are trending downward for tomorrow. Even though S&P is down 1.5%, it is still up over 10% for the year.

central banks will soon issue their currency in digital formAt some point in the next five to 10 years, when each of us becomes the owner of a sovereign-backed digital currency, we will look back on the summer of 2021 as a turning point.

The message delivered last week by the Bank for International Settlements in its annual report could not be more clear. Most central banks will soon issue their currency in digital form, making it directly available to each of us on our mobile phone and instantly exchangeable over long distances — just like email.

© 2015 Mutual Fund Observer. All rights reserved.

© 2015 Mutual Fund Observer. All rights reserved. Powered by Vanilla