It looks like you're new here. If you want to get involved, click one of these buttons!

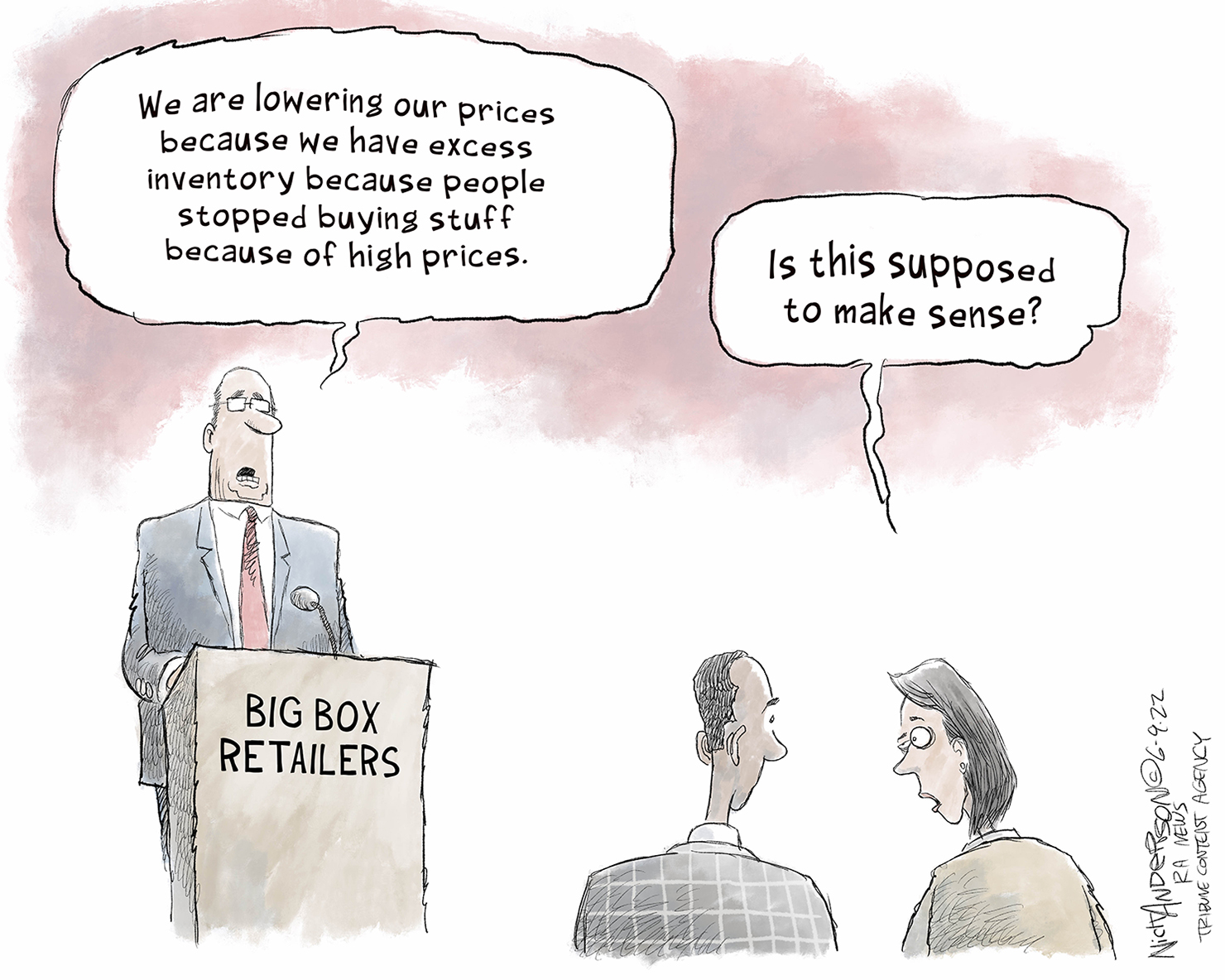

https://www.nytimes.com/2022/06/07/business/target-profit-inflation.htmlTarget, like many retailers that faced skyrocketing demand in the early months of the pandemic, stocked up on goods as snarled supply chains delayed shipments. But consumers are now turning away from goods like furniture, appliances and other products for staying home and shifting to spending more on experiences and going out.

* think you meant CPI, not CPU, correct?You can view a list of available Treasury inflation-protected securities (TIPS) offerings by visiting Fixed income, bonds & CDs. TIPS can't currently be purchased on our mobile app.

TIPS are issued with 5, 10, and 30-year maturities at a specific frequency in auction. On the announcement date, security terms and important dates are posted on Fidelity.com. To view the auction schedule for treasuries, visit US Treasury Bonds and select “Auction Schedule”.

To view available TIPS auction offerings, log in and visit Treasury Inflation-Protected (TIPS) auction offerings.

OK, so what was the point of your smart drivel?The captain obvious explanations are not needed for me. I know them. I have heard them. I view them as more lies told by the regulators/politicians.

Between Jan 2010 - May 2022, the price level has increased 35%. Since Jan 2000, a 73% increase in the price level.- That is using the CPI, which severely undercounts real changes in cost of living. - The source of that stat is from bls.gov's CPI price calculator.

A 35% debasement of buying power over 12 years is not "price stability"

These jokers have failed. The institutions have failed -- They have a "mandate" then they construct policies with the predictable result of avoiding the mandate.

In part 2 of our interview with industry pioneer Steve Liberatore, we explore both ESG fixed income investing, as well as the relatively new area of impact investing where bond proceeds are directed to a specific project or goal and the results are measurable.

+1. Yes indeed. Gotta remember to buy some more PRWCX if it falls a couple of bucks further.Giruox has been a master in using bond & cash positions to counteract his equity risk. His goal is to provide equity-like return while maintain below market risk over a 5 years period.

https://npr.org/2022/06/10/1103995329/inflation-americans-spending-consumer-behavior-pricesThe Labor Department said Friday that consumer prices in May were 8.6% higher than a year ago — the largest increase since December of 1981. Prices rose 1% between April and May, led by jumps in the price of gasoline, groceries and rent.

Shoppers who swallowed price increases for much of the pandemic without batting an eye are starting to blink now that gasoline prices have topped $5 a gallon in much of the country and grocery prices continue to climb at a rapid rate.

https://bls.gov/osmr/research-papers/2017/pdf/st170010.pdfThe Consumer Price Index (CPI) and Personal Consumption Expenditures Price Index (PCE) are two U.S. inflation metrics that use different methodologies, and therefore produce different estimates. The differences can be grouped into four effects: formula, weight, scope, and 'other.' This research evaluates two effects, weight and scope, and discusses their implications. The weight effect is a result of differences in how consumer expenditure data are sourced. CPI sources data from consumers, while PCE sources from businesses. The scope effect is a result of the different types of expenditures CPI and PCE track. For example, CPI only tracks out-of-pocket consumer medical expenditures, but PCE also tracks expenditures made for consumers, thus including employer contributions. The implications of these differences are considerable. Many contracts and government programs are tied to inflation, from rental agreements to social security.

© 2015 Mutual Fund Observer. All rights reserved.

© 2015 Mutual Fund Observer. All rights reserved. Powered by Vanilla