It looks like you're new here. If you want to get involved, click one of these buttons!

My bond funds didn't take a hit. I had IOFIX,JASVX and HOBIX.I sold almost everything. My portfolio lost just -0.1% from its last top.

But you must still have taken the hit yesterday in the downdraft? How can you be sure you will buy back in at a better price than you sold? How long are you willing to be out of the market? To each his own, but given that you're almost all in bond funds (I think) how much can really be gained by market timing, even if you mostly guess right on your buys and sells? Just wondering, not criticizing,

Again, the thread is not about me but after you couldn't come up with anything to debunk the original post you resort to make it personal. I never said that what I do is the only game in town, it works extremely well for our portfolio. I actually posted many times that the average Joe should buy several funds (indexes+managed) and hardly trade.It's all good, FD. PIMIX is still good for long term holders. I'm meeting my goals. That is what is important to me. Keep convincing yourself that getting 5% per year with low SD is the only game in town. I guess there's a reason people live in Georgia :o}

https://seekingalpha.com/article/4377703-update-on-non-agency-mbs-sectorWe noted how AlphaCentric Income Opportunities saw a "run on the fund" where shareholders all liquidated en masse causing a downward spiral in prices.

(Writing about CEFs)....most NAVs are still well below where they were in February even when including the distribution paid since. As we've noted, these securities take the elevator down and stairs back up. We still expect prices to return to around an average price of 90 cents on the dollar but that it would take at least 6 months and more like 18-24 months to do so.

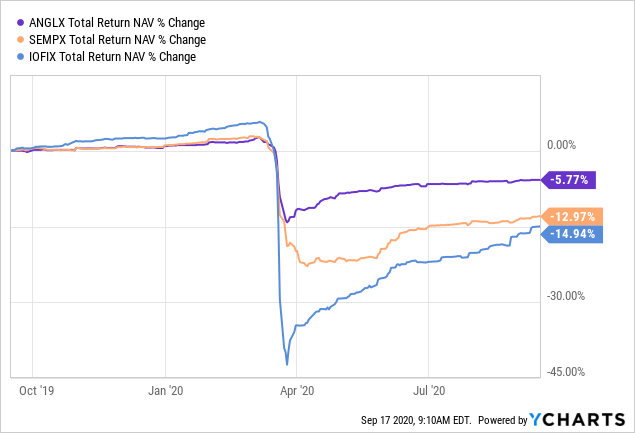

FD, what is the source for the chart you posted? Many thanks.Numbers as of 9/30/2020.

Observations for one month as of 9/30/2020:

Multi- Flat for the month but securitized shined with 1-2.9%/

HY Munis – Flat for the month but Nuveen (NHMAX,NVHAX) did better.

Inter term – (-0.1%) for the month. TGLMX (mostly securitized) did 0.4%.

Bank loans – up 0.3-4% for the month.

Uncontrain/Nontrad -0.2 for the month. Securitized(JASVX,DFLEX)

HY+EM – HY -0.9 and EM=-1.7% for the month with correlation to stocks.

Corp – down month. PIGIX -0.4%.

SP500(VFIAX)-Down monthth at -3.8, YTD=5.55%.

PCI-CEF huge upside at 7.1%. YTD still at -13.7%

My own portfolio

I started the month with IOFIX+DFLEX and replaced DFLEX with JASVX+NHMAX. It’s pretty obvious that funds loaded with securitized bonds are doing well. HY Munis don’t have a momentum yet but I bought NHMAX because it’s in my taxable and it showed a better momentum than others but the last 2 days are down, I was too early but now I’m watching closely. It was another good month for me.

I'm a trader and don't recommend what I do to others. My posts are generic unless someone asks me specifically about my portfolio.@FD1000; I'm guessing you bought in around 3/25/20 ?

Derf

Nope, I sold over 90% at the end of 02/2020 and the rest days later.

Made several good trades with QQQ+PCI in 03/2020.

Start investing back in bond funds to over 99+% in 04/2020.

I had a huge % in GWMEX for several months. I owned IOFIX only in the last several weeks.

I wish I was brave enough to buy IOFIX on 3/25/2020. It made over 50% since then.

How do you square owning IOFIX with your later comment in this string to avoid risky funds?

How do you square owning IOFIX with your later comment in this string to avoid risky funds?@FD1000; I'm guessing you bought in around 3/25/20 ?

Derf

Nope, I sold over 90% at the end of 02/2020 and the rest days later.

Made several good trades with QQQ+PCI in 03/2020.

Start investing back in bond funds to over 99+% in 04/2020.

I had a huge % in GWMEX for several months. I owned IOFIX only in the last several weeks.

I wish I was brave enough to buy IOFIX on 3/25/2020. It made over 50% since then.

Nope, I sold over 90% at the end of 02/2020 and the rest days later.@FD1000; I'm guessing you bought in around 3/25/20 ?

Derf

© 2015 Mutual Fund Observer. All rights reserved.

© 2015 Mutual Fund Observer. All rights reserved. Powered by Vanilla