It looks like you're new here. If you want to get involved, click one of these buttons!

and,The deflationary thesis holds more weight for three primary reasons.

Weakening rates of population growth and excessive levels of unproductive debt are two long-term structural forces that have been working to undermine the rate of economic growth, widen the output gap, create excess capacity, and exert a general disinflationary force on the economy. Both of these forces will persist.

Recessions exacerbate excess capacity. The current recession is one of the worst economic crises the country has ever faced. The rate of inflation nearly always declines during recessions and typically does not trough for years after the conclusion of the recession and the eventual reduction in excess capacity. A severe recession usually knocks several hundred basis points off the rate of core inflation, placing current measures firmly below the zero bound. The strength of the recovery will determine how persistent the deflation will be.

While the Federal Reserve has engaged in a rapid expansion of its balance sheet and the monetary base, both the money multiplier and the velocity of money will work against the increase in money growth. Velocity tends to decline as debt levels rise. There's no reason to believe the velocity of money will rise significantly. In fact, most evidence points toward a very aggressive collapse in the velocity of money, a force that will continue to negate monetary policy actions as it has for the last several decades.

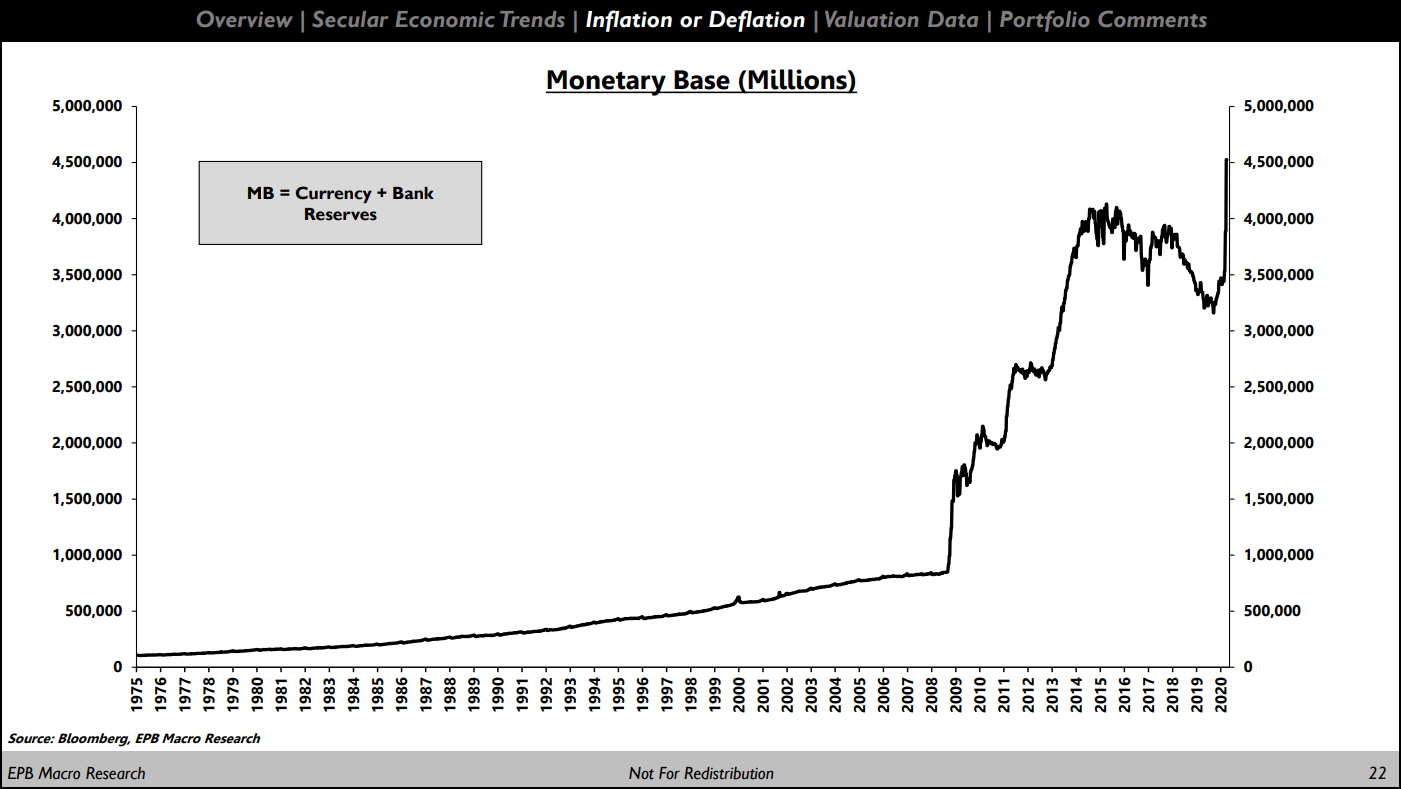

Difference Between Monetary Base and Money Supply:...various measures of inflation expectations reveal that the bond market is currently expecting deflation for at least the next three years and rates of inflation below 1.5% for more than 10 years.

High Level of Unproductive Debt:Often we conflate Federal Reserve "money printing" with an equal and consistent increase in the money supply. This is not the case.

When the Federal Reserve buys an asset from the private sector, the Federal Reserve increases excess reserves, which represents an increase in the monetary base, not the money supply.

https://static.seekingalpha.com/uploads/2020/4/23/48075864-15876672613202152_origin.png

Unemployment Factors:High levels of debt are often misunderstood. Commonly, we hear that debt levels are getting too high and that inflation will ensue. The data actually proves that higher levels of debt, particularly unproductive debt that does not generate an income stream, leads to deflation, not inflation.

On Assets to Hold:In the prior two recessions, it took 47 months and 75 months, respectively, to regain the number of jobs that were lost. In this recession, the number of job losses will erase upwards of 20 million paychecks based on preliminary data from the report of the initial claims.

Gold can perform well during periods of inflation or periods of deflation. The direction of real rates tends to be a more critical factor. As such, my analysis suggests a combination of Treasury bonds, gold, and higher than normal levels of cash is the best way to move forward in the current environment.

© 2015 Mutual Fund Observer. All rights reserved.

© 2015 Mutual Fund Observer. All rights reserved. Powered by Vanilla

{kind=link}

{kind=link}