Very busy at this house; but take a bit of time to catch this or that for the markets.

The tariff wars (pending or otherwise) are receiving the threats from other countries; as in, "okay, slam a tariff; we'll play the game" and await you "crying uncle".

So, we have Canada, Mexico, EU, India and China as the major announcers OF "tariffs to you", too.

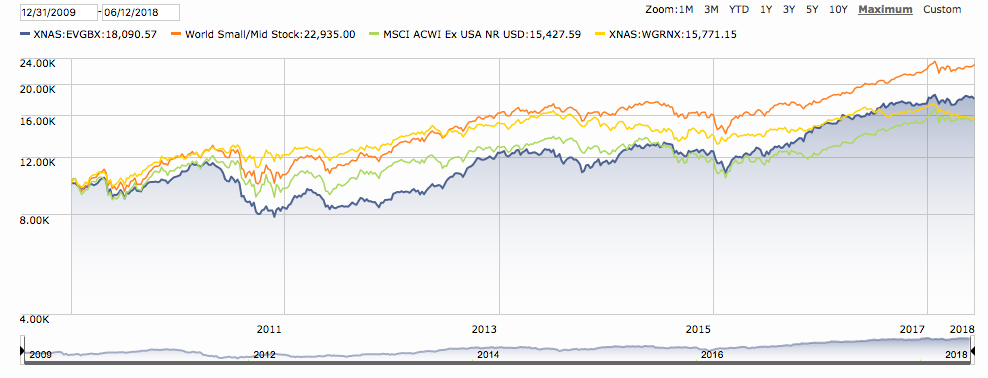

SP-500, to use as a U.S. gauge, is so-so YTD; and one knows a lot of this gain is from the better performing sectors, tech., health, con. discretionary...............so, if these areas start to go to heck; well others suffer, too.

One finds the global today (June 18) not being very happy, not a trend yet, eh?

https://www.barchart.com/etfs-funds/etf-monitor?orderBy=percentChange&orderDir=descI'll provide a flash back from 10

years ago (June 16, 2008, Monday).

Our portfolio had its high value point on Oct. 31, 2007 (Halloween Day). International holdings had begun to become more erratic, but most U.S. equity was still fairly happy.

News, data and related going into the end of 2007, especially in Dec. 2007 kept my attention. We watched an erratic equity market for another 6 months; along with the news and data. December of 2007 had very large swings in daily equity.

On June 16, 2008, Monday; we sold 87% of our portfolio.

An existing bond fund holding was kept in place, PTTRX . The equity sells monies were moved into either "stable value" or money market, depending upon the choices at the time. During this period, both stable value and MM were yielding about 5% APR.

With a smile and a head shake I thought about the date this past weekend and being 10

years out from June, 2008.

Currently, we're 51% equity, 95% which is U.S.; all being in tech. and healthcare.

We'll be watching this week more so, as time allows.

Good fortune to all,

Catch