COVID-19 and the portfolio I honestly hope this virus runs its course shortly and dies away on it's own.

Well, now we're at this point; where the general public, who hasn't been paying attention are going to have reports shown more frequently on their tv's. The below two, are the pronouncements that go past the algo trading or whatever else one chooses to determine "profit taking".

I continue to watch data reports regarding COVID-19, and this in itself is troublesome. And as has been discussed previous, supply chain issues in many market areas; and also to the point of further restrictions in travel, via whatever means. Visa/MC have reduced profit estimates from just 1 month ago, as usage will be down. And what about the Walmarts and $ stores; among all of their product lines. A simple example is that 8

5% of all toys/games related are imported from China.

Sanofi and Gilead have noted, among other researchers; that any type of successful vaccine is generally anticipated to have about a 12 month time frame

I'm not going to drag this further.

WHO press conference, 'Now is the time to prepare', Feb. 24

CDC warns of 'severe disruptions', Feb. 2

5There is

no mercy in the equity market place at this time, as; even our healthcare and med. tech. is getting the big head slap, which are our only equity exposure at this time.

Lastly, if you have an alternative view of this post; please comment. I'm only writing about what I interpret to be the current circumstance. Other viewpoints are needed.

Seriously.....take care of you and yours,

Catch

BUY - SELL - OR PONDER February 2020 @MikeM For awhile means what 10-15-20 % drop ? I missed my chance back in 2018 4/th quarter drop.

Derf

BUY - SELL - OR PONDER February 2020 Yup. See my previous post above yours. Will continue to nibble as appropriate

lots folks especially near retirement has bailed long time ago. probably best to have 50/50 if near retired/retired

anyone buying today or next few days once the dust maybe settling down?

BUY - SELL - OR PONDER February 2020 lots folks especially near retirement has bailed long time ago. probably best to have 50/50 if near retired/retired

anyone buying today or next few days once the dust maybe settling down?

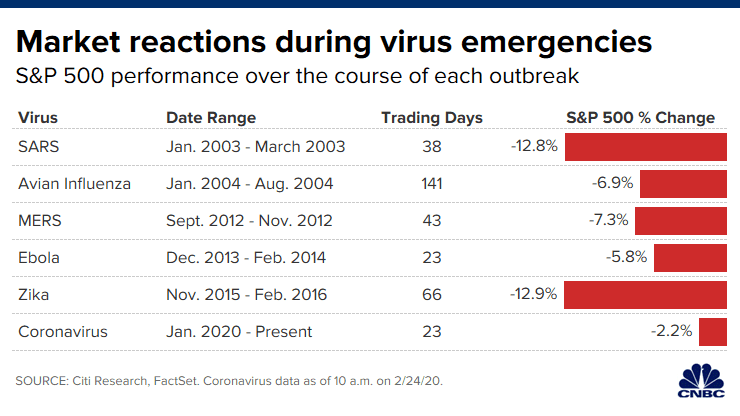

COVID-19 and the portfolio Scroll down 1/2 of the page for the graphic.

Market reactions during virus emergencies

Daily Financial News Aggregator

A look ahead for the overnight potentials in the markets...... NOTE:

Obviously, there are massive gyrations in the markets this morning.

Currently, at

5 minutes past the market open; there is no access to the Fidelity site for log-in.

I'm sure this circumstance is common to other vendor sites, too.

My presumption, is that enough retail investors are at least checking portfolios; overwhelming the servers and/or the networks ability to connect.

This

site page is an interesting overview, near real time, of global ETF's for all of the major market sectors.

COVID-19 and the portfolio A lot of it depends on your time horizon. My wife and I will remain fully invested in US growth funds and don't anticipate making any changes due to COVID-19. We don't have any emerging market or overseas funds because the US is the premier global economy and we expect it to remain so for years to come.

However, if the virus starts to seriously disrupt the global supply chain then some of our tech and large-cap funds could definitely be impacted in the short term. But over a 15-20 year time frame I'm not concerned.

Another factor to consider is that the Chinese communist state has almost certainly deliberately misrepresented the number of infections and deaths. The real number may be 10, 100, or even 1000 times higher than they claim. China's chronic dishonesty may well prove to be the real virus.

Still, I would strongly advise against making any knee-jerk changes to a portfolio which, like us, you might have taken years to craft.

COVID-19 and the portfolio First post. Hello all. I think this disease will effect mkts a lot. I have most everything at TRowe inc. my Roth and 403b. Have been in PRHSX and PRGTX along with PRNEX when prices drop for energy or the fund fall into the low 30s at least. Few weeks ago I move most everything to PREMX and PRULX just keeping some shares of the others to keep them open. I got bit a few times when funds closed....

I have been stalking you all here for a few weeks and know many of you just sit tight and rebalance but I do feel that moving things to bond funds like I have when I have made good gains and the market seems to be about to burst works for me. Of course if GTX drops down to the $14-$15 range I will shift again perhaps. I know I have missed some gains the last 10 years but am still above 8% and some years more still. I am in my mid 40s and need to build not just maintain. Wife's things are with Janus because it sounds like her mom's name (you should see her pick the final 4 LOL) Thanks for adding me, I have been looking for a place like this. Split my board time here and on WUS.

COVID-19 and the portfolio @Derf We don't do dice for investments and the Magic 8 Ball is in the shop for repairs.

I will check Khan Academy for die rolling data outcomes relative to investments.

@WABAC2019-2020 flu season data was noted here recently; but this is the current data for week ending Feb. 1

5 --- CDC estimates that so far this season there have been at least 29 million flu illnesses, 280,000 hospitalizations and 16,000 deaths from fluHowever, traditional flu season illness or deaths have not affected our investment portfolio in the past. Obviously, my death from influenza related conditions would have an impact on portfolio decisions.

Risks build in world's largest bond funds I "love" GMO forecasts. In 12/31/2010 GMO 7 years forecast (

link)

was that US LC would make 0.4% + 2.

5% inflation = 2.9% and US SC would make -1.9%+2.

5%=+0.6%. GMO was way off, for 7 years SPY made 13.6

5% annually return while IWM made “only” 11.6

5%

Investors prospered by staying the course Investors prospel by staying the course

https://www.google.com/amp/s/www.stltoday.com/business/local/report-investors-prospered-by-staying-the-course/article_8a368181-c1ac-5665-9ce9-e1c4335ec5d4.amp.htmlInvestors in “allocation” funds, which hold a mix of stocks and bonds, earned more than the funds themselves, indicating that the majority of investors put more money in the funds when prices were low than when prices were high. Target-date funds, which fall into this group, are likely the main reason for the category’s better performance. These funds, which invest in a mix of stocks and bonds that grows more conservative as investors near retirement, are predominantly held in workplace retirement plans, in which investors tend to hold for the long term and invest at regular intervals.

Investors showed the worst timing when they invested in alternative funds — investments designed to provide returns that aren’t correlated with stock or bond markets. Those funds didn’t benefit from a general upward trend, surrendering an average 0.61% annualized return over the 10-year rolling periods. But investors fared much worse, losing 2.0

5%

Tdf maybe good ways to go long term

{kind=link}