About the 4% rule It's not necessary to follow Bengen's 4% w/COLA SWR for US moderate-allocations to appreciate its significance.

Before-Bengen, the thinking was to start with long-term stock returns, use 3-4% margin to account for return variability, and use the net as withdrawal rates. But the problem was that many of these strategies failed.

Even today, there is a widely followed radio personality who uses this as 12 - 4 = 8% withdrawal rate. But no need to go back to 1930s, this strategy would have failed if started in 2000.

So, Bengen found this 4% w/COLA that would have survived even the worst 30-yr stretches in the US. But one can use something higher and hope for the best. BTW, Bengen is still around, may be 75 or so, and is himself amused by how people got so stuck to his Rule.

The main point is that starting point should be the 4% w/COLA, not the long-term stock returns.

Treacherous September is Leaving Traders Everywhere on Edge - Bloomberg Market Analysis There’s ALOT riding on this fridays jobs report. As long as the numbers are over 125k, things should be okay. If they fall below 100k we are in deep doo-doo!

There's ALWAYS 'a lot' riding on the jobs report, CPI, PCE, PCM, CPI, ISM, etc.....and it's always billed as an "all-important" report as well. Fear, doom, blood, and panic sell, remember.

I'm too old a trading duck to get worried about these reports. I used to trade around them earlier in life, now I just roll my eyes and try to be away from the computer when the numbers come out, because ... *shrug* .... why not.

Treacherous September is Leaving Traders Everywhere on Edge - Bloomberg Market Analysis Among Bloomberg headlines, I couldn't make sense out of,

"Pimco Sees BOJ Hike as Soon as January, Likes Long-Term (Japanese) Bonds"

Normally, buying bonds ahead of rate hikes isn't a great idea. Does Pimco think that expected bond hits have already occurred? Or, that yen strength will compensate for bond losses? Or, Pimco is talking about rate futures?

On search, I found an open blurb at UK-Bloomberg, but it didn't make things any clearer.

Thanks for the question

@yogibearbullI agree with your analysis. I can only speculate PIMCO may be waiting until the BOJ raises rates further before making a substantial purpose. Alternatively, they may be playing the shorter part of the curve or - possibly just holding

yen for the time being. It does sound like Bloomberg doesn’t have all their ducks lined up straight here, However, the chief of fixed income at TRP is cited as sharing a similar sentiment.

I did find the identical Bloomberg article reprinted at

Yahoo if you want to take a look.

Here’s the Bloomberg article re T.Rowe’s take on the matter:

Yahoo(Note - I’ll be traveling today. Sorry won’t be able to respond to other questions.)

Treacherous September is Leaving Traders Everywhere on Edge - Bloomberg Market Analysis My results == 2 of the last 4 years Sept was down, 4 of the last 4 years Oct. was down. You would think the odds say Oct should be up this year or will it be a self fulfilling outcome due to all the stories, comments? One other item, over the last 4 years I've never been up more than 7 months of the year. 3 years were up 7 months and down 5, 1 year (2022) up 5 months down 7. This year I'm already up 7 months so far. (This is not scientific detail as my spending and hence monthly outcome is different from anyone else but gives me a ball park picture of how Mr. market behaves.

Treacherous September is Leaving Traders Everywhere on Edge - Bloomberg Market Analysis There’s ALOT riding on this fridays jobs report. As long as the numbers are over 125k, things should be okay. If they fall below 100k we are in deep doo-doo!

Treacherous September is Leaving Traders Everywhere on Edge - Bloomberg Market Analysis ”(Bloomberg) -- September has traditionally been a terrible month for traders and risks being even harder to navigate in 2024 given lingering questions about the Federal Reserve’s anticipated interest-rate cut.

“Bonds, stocks and gold have typically suffered losses in the month, as traders reassessed their portfolios after the summer break. The S&P 500 Index and Dow Jones Industrial Average have had their biggest percentage losses since 1950 in the month of September. Bonds have slid in eight of the last 10 Septembers, while bullion has dropped every time since 2017.”Story at Yahoo FinanceInterestingly, gold slipped below $2

500 Sunday evening for the first time in several weeks after testing $2600 recently. This in the face of a very bullish

Barron’s. article.

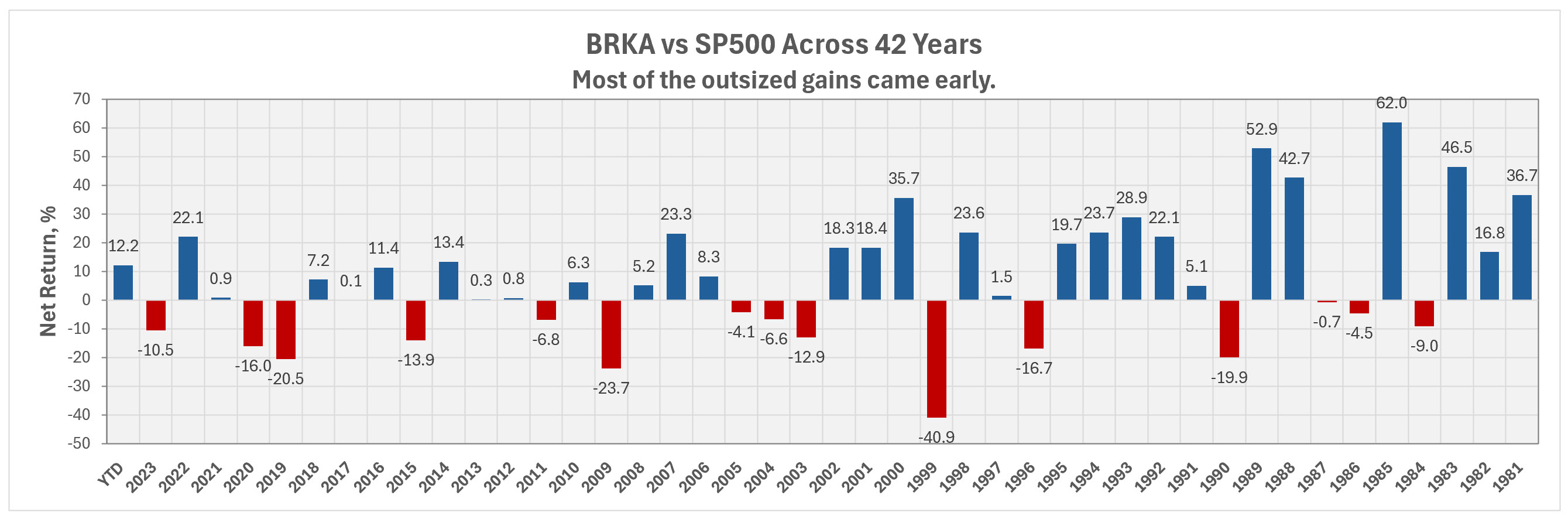

31 Years of Stock Market Returns You guys are pouring on the pessimism a little thick here, don't you think? Like Emily (below) I'm planning for a future that's a little brighter.

BONDS The week that was.... December 31, 2024..... Bond NAV's...Most positive. FINAL REPORT 2024 Thanks for the explanation. My biggest bond fund holding is FADMX, followed by FTBFX, FCNVX, PTIAX and FAGIX. I’ve stuck mostly to Fidelity funds for simplicity and ease in rebalancing. I also have a considerable number of CDs and Treasuries in ladders extending out 5 years. Now that interest rates are dropping, I’m reinvesting maturing issues into bond funds.

31 Years of Stock Market Returns except when you’re over 75 the number of years you have to fund left are less than 20 and very possibly less than 10

Fidelity Automatic Account Builder changes This is a nice feature I learned from

@msf years ago. In the long run, it help to build sizable positions in institutional shares of OEFs. The $

5 spend pays itself many times over from having lower expense ratio.

Does Schwab offers similar fearure ?

Fidelity Automatic Account Builder changes The changes to Fidelity automatic investment features have been implemented many months ago, may be even in 2023. That feature is not as good as it used to be, say in 2022. That feature used to be very flexible and you used to be able to use it for a next day trade.

Fidelity wants maximum number of $49-50 commissions not $5 commissions.

31 Years of Stock Market Returns +1 Anna & Catch.

Rarely do we share our age or what our investments are intended for. If you are 25 - close your eyes. All will be well. If you are 50, maybe squint a little. But if you are over 75 and counting on those investments to sustain you and yours thru your lifetime, tread very cautiously.

About the 4% rule Not surprising that the 4% Rule fails globally

Wade Pfau has a long 1+ hour podcast (8/1/24), and an early segment within is for testing the 4% Rule globally. It failed for most countries. It almost worked for Australia but it was a 3% Rule instead. So, the 4% Rule is something unique to the US and possibly Canada.

Edit - As the YouTube link opened as an embedded link, note the the relevant segments starts around 7:40.

Link to related 2010 paper,

https://tinyurl.com/3299f69j