It looks like you're new here. If you want to get involved, click one of these buttons!

"great" post." It is refreshing to have an established bond analyst to discuss the process of exploring various sectors of bonds and their inefficiencies."

But I don't see why we need an "established bond analyst" when we already have FD1000.

Well, if your toilet ain’t working, do you want ageneral therapist who claims to know a lot about everything from gutter repair to toasters? Or do you want a dedicated plumber with all the right tools?

Could the National Guard stop the bleeding? Maybe put 500 on Crypto detail?Expect increased chatter about a national crypto reserve in the coming weeks. Managed by Orange Julius Corp of course!

I'm troubled by Vanguard omitting the fee adjustment formula from the SAI. Three numbers are needed: (1) the base rate; (2) the maximum fee adjustment; and (3) the rate of adjustment (how many basis points added to management fee for how many percent outperformance).Morningstar calculates that performance-fee funds have generated an average alpha -- or risk-adjusted outperformance relative to the appropriate broad market index -- of 0.22 percent annually over the last 15 years through September [2017]. By comparison, active funds that charge a flat fee generated an average alpha of 0.29 percent.

...

fulcrum fees leave lots of opportunities for misalignment. They create incentives for managers to take more risk when they’re losing to the benchmark and less risk when they’re winning, regardless of whether those changes are best for investors. [Rest of paragraph contains complaints about how fulcrum fees might be abused, e.g. by picking the wrong benchmark - something neither Fidelity nor Vanguard does.]

The FLPSX prospectus says that its base rate is not more than 0.67% [item (1) above]For Fidelity® Dividend Growth Fund, Fidelity® Low-Priced Stock Fund, Fidelity® OTC Portfolio, and Fidelity® Value Discovery Fund, each percentage point of difference, calculated to the nearest 0.01% (up to a maximum difference of ±10.00), is multiplied by a performance adjustment rate of 0.02% [item (3) above]. The maximum annualized performance adjustment rate [item (2) above] is ±0.20% of a fund's average net assets over the performance period.

The fund’s record is now [YE 2010] so bad that it is paying customers to invest. This isn’t a joke. The expense structure of Aggressive Investors 1, as well as other Bridgeway funds, calls for higher management fees when the fund beats its benchmark and lower fees when it trails. Based on the formula, Bridgeway’s sponsor is now paying into Aggressive Investors 1 at an annual rate of 0.51% of assets.

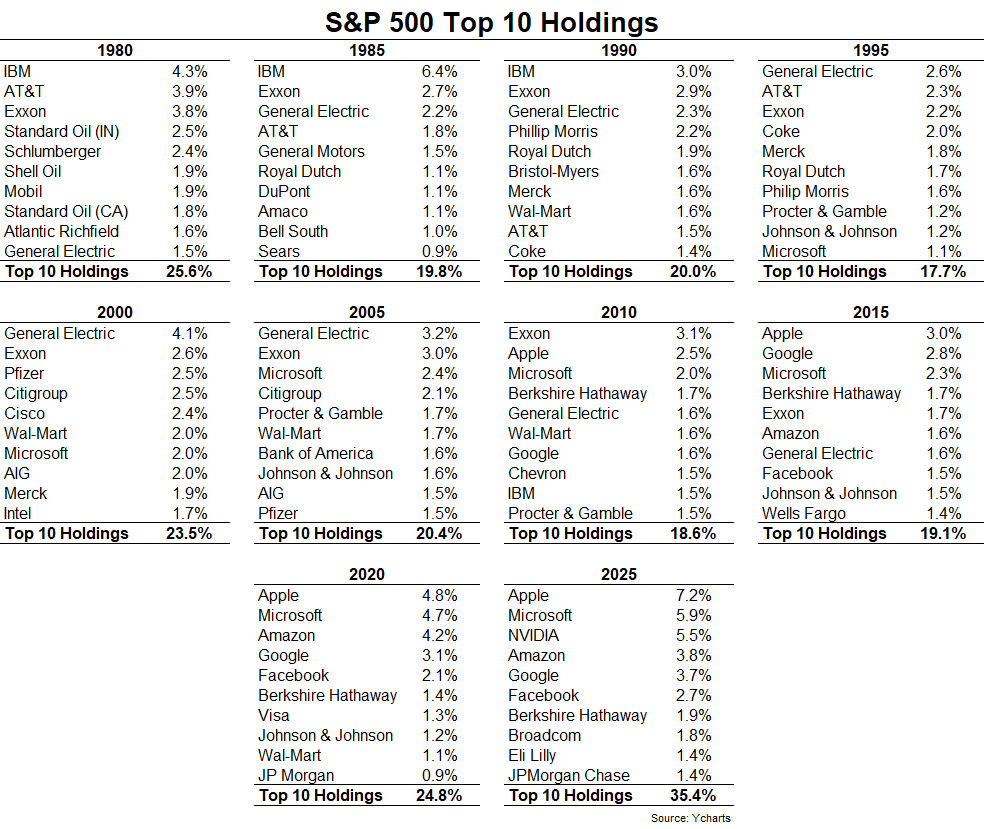

Article:The S&P 500 without its top ten companies would have likely delivered lower returns in recent years but has historically demonstrated strong, and often superior, long-term performance compared to the highly concentrated, market-cap-weighted index.

In just over a month, the crypto market has lost $1.2 trillion in value. The steady declines since mid-October have erased much of the gains received by both small and large investors. Among the latter is a very well-known figure: U.S. President Donald Trump, who is also partly responsible for the euphoria the sector experienced until October.

But the Trump effect has completely vanished, with digital assets falling back to levels seen before his term. His direct support of the sector and entry into crypto businesses fueled short-term excitement, but investors have forgotten about that now. Today, the focus of the debate is the potential AI bubble and interest-rate cuts. And the Trump business empire has felt the shock of reality: since September, it has lost at least $1 billion of its fortune (dropping from $7.7 billion at the beginning of September to the current $6.7 billion), according to the Bloomberg Billionaires Index, a decline largely due to the Trump family’s growing ties to crypto projects.

The Trump family went all-in on digital assets: they launched tokens, created companies, invested in the industry, pardoned convicted crypto tycoon Changpeng Zhao, and legislated in favor of the sector, pushing major cryptocurrencies to historic highs. But in this market — marked by extreme volatility and speculation — no one is spared, not even the president. A good example of this was the launch, a few days before Trump’s inauguration, of the memecoin $TRUMP, a token with no backing whatsoever beyond being linked to the tycoon’s image. Minutes after its release, euphoria broke out and the token reached a value of more than $15 billion. But like every speculative wave, the excitement was short-lived, and its price plunged by up to 76% within a few hours.

In these past months, $TRUMP has gone through ups and downs, but since mid-August its declines have intensified, and it has lost around 40% of its value; since its launch, it is down 85%. As of today, the size of the Trump family’s stake in the project is unclear; according to Bloomberg estimates, those close to him hold around 40% of all outstanding tokens. At current prices, that stake is worth about $310 million, implying a loss of $117 million since the end of August.

But this is only the tip of the iceberg when it comes to the Trump family’s crypto empire. With their flagship project, the crypto platform World Liberty Financial, they issued the WLFI token, which has plunged 38% since early September: those close to the president hold an amount of tokens that reached an accounting value of roughly $6 billion at its peak, but which today are worth half that — about $3.15 billion — according to Bloomberg data. These assets, however, are not included in the agency’s calculations, as they are not traded on organized markets.

© 2015 Mutual Fund Observer. All rights reserved.

© 2015 Mutual Fund Observer. All rights reserved. Powered by Vanilla