It looks like you're new here. If you want to get involved, click one of these buttons!

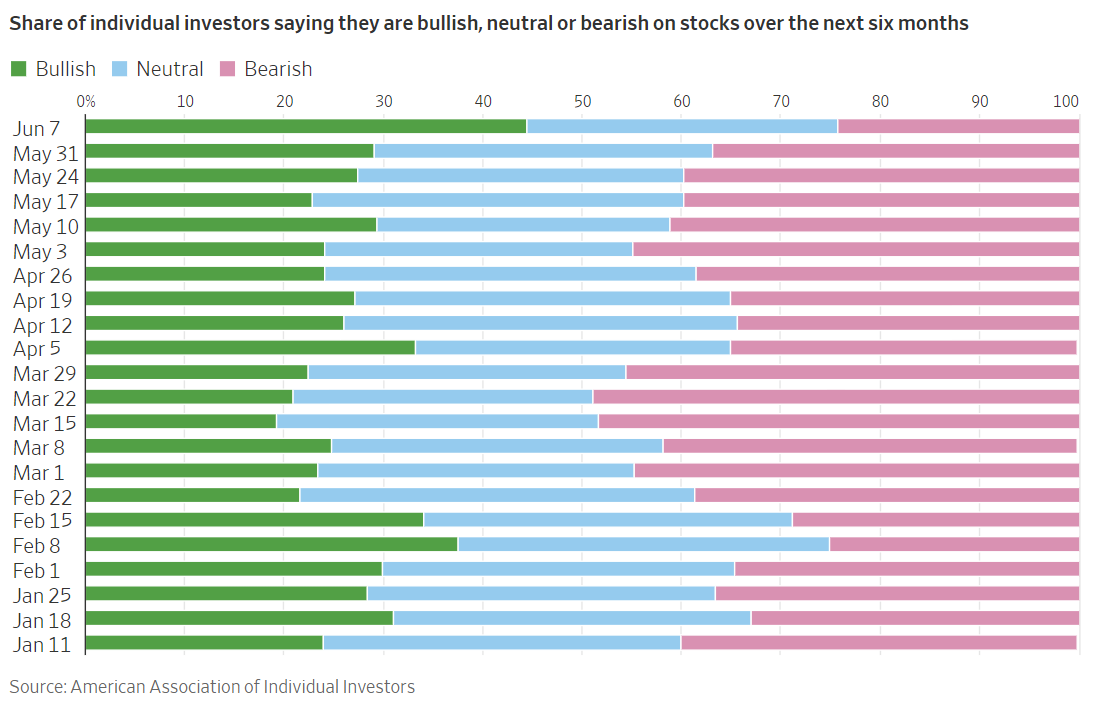

That is all.U.S. equity funds had their biggest weekly outflow in 10 weeks in the seven days to June 7 as investors, worried about rising inflation and an economic slowdown, pulled out their money.

[ellipses]

Refinitiv Lipper data showed investors offloaded a net $16.44 billion worth of U.S. equity funds in their biggest weekly net selling since March 29.

[ellipses]

Among U.S. funds, large- and mid-cap funds experienced net outflows of $7.53 billion and $1.07 billion, respectively. However, small-cap funds saw net inflows totalling approximately $1.15 billion.

Tech sector funds faced outflows of $1.31 billion after five consecutive weeks of inflows, while industrials and consumer discretionary funds pulled in $616 million and $399 million, respectively.

Money market funds received inflows of $19.83 billion, according to the data, reflecting investors' continued preference for these funds as net buyers for the seventh consecutive week.

U.S. bond funds witnessed withdrawals of $561 million, following five consecutive weeks of inflows.

Investors sold U.S. general domestic taxable fixed-income and short/intermediate investment-grade funds amounting to $1.79 billion and $1.45 billion, respectively, while purchasing government funds totalling $1.76 billion.

Hotels are seeking millions from S.F. for damage when they were homeless shelters.

Hotel Union Square’s cleanup bill was steep — $5.6 million to repair rampant smoke damage, broken light fixtures, mold and other problems.

As city supervisors consider shelling out millions to settle the dispute over damages at one of San Francisco’s hotel homeless shelters, taxpayers could be on the hook for millions more to settle similar claims from other hotels that participated in the program.

In September 2021, the owners of Hotel Union Square filed a claim with the city, alleging unhoused residents who the city had placed there had caused $5.6 million in damages — and cost the Dallas-based hotel operator hundreds of thousands more in lost rent.

City officials created the Hotel Program in 2020 during the COVID-19 pandemic and used it to house more than 3,700 high-risk residents in 25 hotels. With federal and state funding drying up, the city has gradually closed most of the hotels.

Your comment sounds like a pitch to be a buy and hold investor now. That seems a bit out of character for a well known trader.Lots of negativity on bonds here. I can understand the allure of cash when you can get 5.08% at firms like Schwab. Yet many bond funds are on pace for double digit returns in 2023. Albeit much of those gains were front loaded in January/February. There is even more negativity on commercial real estate. Yet one of the few pure plays on commercial real estate in the open end bond universe is doing just fine YTD and far outperforming cash.

As I said in a post on the Treasury thread, I don't agree with the terminology of Treasuries flooding the market. I read the Treasury article as a slow, gradual, introduction of shorter term securities, likely trying to avoid spooking the market. That could be good for slightly higher interest rate CDs, but also a trend of bonds gaining some traction. I keep expecting FR/BLs to become more "interesting".Read the YBB thread above. Doesn't bode well for bonds if Treasuries higher yield flood the market.

I agree with Derf's comments above that "flood" is not an accurate descriptive term. This statement, "Treasury plans to increase issuance of Treasury bills to continue financing the government and to gradually rebuild the cash balance over time to a level more consistent with Treasury’s cash balance policy. Initial increases in bill issuance will be focused on shorter-tenor benchmark securities and cash management bills (CMBs), including the introduction of a regular weekly 6-week CMB (the first of which will be announced on June 8)." I see phrases like "gradually rebuild cash balance" and "initial increases...will be focused on shorter-tenor...securities", as suggestive of slow and careful actions, not a "flooding" of issuance of Treasuries. I expect both Treasuries and CDs to reflect these more gradual increases, to not spook the market, and not lead to an unnecessary recession.Looks like the bond market will take a hit as a consequence. Gains made this year could be in jeopardy. Great...

© 2015 Mutual Fund Observer. All rights reserved.

© 2015 Mutual Fund Observer. All rights reserved. Powered by Vanilla