Here's a statement of the obvious: The opinions expressed here are those of the participants, not those of the Mutual Fund Observer. We cannot vouch for the accuracy or appropriateness of any of it, though we do encourage civility and good humor.

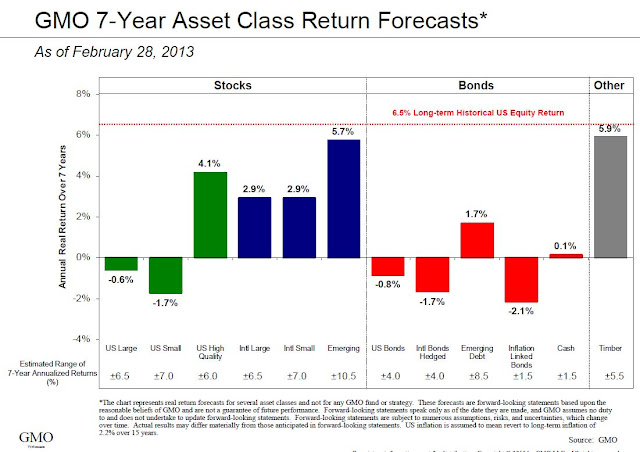

For folks who haven't looked much at GMO projections, I'd make four quick notes.

1. GMO has a pretty good historic track record for getting these things right.

2. the returns shown are "real," that is, inflation-adjusted. The nominal returns would then be 2-3% higher.

3. the different asset classes are substantially different confidence intervals. That is, the developed market stock estimates are accurate - in GMO's estimation - to within about 650 bps. The emerging markets estimate comes with a "give or take 1050 bps" disclaimer.

4. finally, this might be the first time they've included cash as a distinct asset class. And, in their estimation, one likely to outperform the broad US stock market averages.

Yes, this part about quality stocks always confused me. According to M*, such funds like JENSX invest in quality stocks, and of course by definition GMO Quality III GQETX invests in quality stocks. Performance of GQETX practically coincides with that of JENSX, but, unlike JENSX, GMO fund GQETX is extremely tax inefficient for a stock fund, and you can buy it only if you have $10M or more to invest there. Perhaps using VIG may help, or maybe COBYX? Any comments about BEGIX, which looks pretty stable and did very well for almost 10 years since inception?

They have very good track record indeep, starting from predicting bull run in 1982. He predicted the following, all the based on reversal to the mean

- In 1982, he said U.S. market was ripe for a "major rally."

- In 1989, he correctly called the top of the Japanese economy.

- In January 2000, he warned of an impending crash in tech stocks which took place two months later.

- In April 2007, Grantham said we are now seeing the first worldwide bubble in history covering all asset classes.

- They also predicted the out performance of many of the asset classes that were cheap in 2001, REIT, Smallcap value, Emergin Market, etc.

GMO's predictions are based on the idea that profit margins and price-earnings ratios are mean-reverting over a period of years. Here is the link to Duke University professor Edward Tower' study on their predictions

GMO actually lists that in their FAQ and the answer is: "GMO defines quality companies as those with high and stable profitablility, and low debt. Please refer to the white paper entitled "The Case for Quality - the Danger of Junk" located in the US Equity section of the site's Library for further detail."

Very vague answer so you do indeed need to see the white paper for more detail and you can find that here. However, in reality the paper doesn't go into a whole lot more detail....The only criteria they include with the previous 2 (high, stable profitablity & low debt) is low earnings volatility. So just figure the stocks are going to fall into at least the top half in each of those categories. You will notice 1 quality that is absent from their definition but you will find in many others (SPHQ) is Dividends...and that can make a dramatic difference.

Based on their holdings here is a sample of stocks that fit their criteria Oracle Corp. 5.3% Johnson & Johnson 4.7% Google Inc. (Cl A) 4.4% Coca-Cola Co. 4.2% Cisco Systems Inc. 4.2% Pfizer Inc. 3.8% Microsoft Corp. 3.8% Philip Morris International Inc. 3.5% Chevron Corp. 3.3% Express Scripts Holding Co 3.0% International Business Machines Corp. 2.9% Procter & Gamble Co. 2.8% Wal-Mart Stores Inc. 2.7% PepsiCo Inc. 2.7% Hewlett-Packard Co. 2.6%

I wonder what would be returns of high quality international stocks? It seems that for US stocks they expect 4.7% premium, per year. As of now, it looks like international stocks are going to have almost 3% real return even if one does not try to find quality. So maybe if one can find high quality international, they can earn 7.5% per year (real returns)? M* emphasizes ARTGX and ARTKS for quality. Is it the same quality as the one discussed by GMO?

For comparison take a look at the Credit Suisse Investment Returns Yearbook 2013 edition. I have posted a link to the pdf at this thread. They did look at Reversion To Mean and estimated equity returns. The folks are from London School of Business.

Quoting from the text:

"For major markets with a low risk of default, we therefore estimate an annualized forward-looking 20-year maturity premium of around 0.8%, in line with the long-run premium on the world bond index. We noted above that bonds of this maturity now have an expected real return of close to zero. Since the maturity premium is the amount by which bonds are expected to beat cash, this implies that the annualized return expected from cash over this same horizon is around –0.8%. The real return from a rolling investment in bills is thus likely to be firmly negative, even before tax."

"After adjusting for non-repeatable factors that have favored equities in the past, we infer that investors expect an equity premium (relative to bills) of around 3%–3½% on a geometric basis and, by implication, an arithmetic mean premium for the world index of approximately 4½%–5%."

"Current levels of risk or risk aversion do not therefore justify an equity premium above the long-term estimate of 3%–3½% (relative to bills). Those who argue to the contrary may well have forgotten that equity markets almost always face a wall of uncertainty. We do not live in uniquely uncertain times."

"Because of their slow reaction to information, investors’ decisions reflect past returns and can be characterized by herding. The herding pushes prices higher (or lower) and this can create a feedback loop. Thus, prices may deviate from fundamental value for a long time."

"When stocks are overvalued, the subsequent return can be expected to be lower than in normal times; when stocks are undervalued, the subsequent return can be expected to be higher. The eventual return to normalcy offers profit opportunities to astute investors who are not subject to these behavioral biases ... The weakness of this view is the assumption that investors do not learn about their behavioral biases, and that there are not enough smart, fundamental investors around to prevent this mispricing from persisting."

"As in the case of equities, there appears to be a tendency towards mean reversion. Buying the bond market at a high coupon-to-price ratio, or at a low price-coupon ratio, has on average been rewarded with superior real returns, as government bond prices have reverted towards the mean. For bonds, like equities, there is historical evidence of mean reversion. ... The key question, then, is whether mean reversion is identifiable only with hindsight, or whether it is apparent and profitably exploitable on an ongoing basis."

"Having examined the long-term historical evidence for return predictability, we conclude that much of the popular evidence for mean reversion is attributable to optical illusions that employ perfect hindsight.

Comments

For folks who haven't looked much at GMO projections, I'd make four quick notes.

1. GMO has a pretty good historic track record for getting these things right.

2. the returns shown are "real," that is, inflation-adjusted. The nominal returns would then be 2-3% higher.

3. the different asset classes are substantially different confidence intervals. That is, the developed market stock estimates are accurate - in GMO's estimation - to within about 650 bps. The emerging markets estimate comes with a "give or take 1050 bps" disclaimer.

4. finally, this might be the first time they've included cash as a distinct asset class. And, in their estimation, one likely to outperform the broad US stock market averages.

For what it's worth,

David

He predicted the following, all the based on reversal to the mean

- In 1982, he said U.S. market was ripe for a "major rally."

- In 1989, he correctly called the top of the Japanese economy.

- In January 2000, he warned of an impending crash in tech stocks which took place two months later.

- In April 2007, Grantham said we are now seeing the first worldwide bubble in history covering all asset classes.

- They also predicted the out performance of many of the asset classes that were cheap in 2001, REIT, Smallcap value, Emergin Market, etc.

GMO's predictions are based on the idea that profit margins and price-earnings ratios are mean-reverting over a period of years. Here is the link to Duke University professor Edward Tower' study on their predictions

http://public.econ.duke.edu/Papers//PDF/GMO_Predictions1.pdf

In fact, Mr. Tower participated in the discussions with Boglesheads in Diehard forum at M* after he published this research.

GMO actually lists that in their FAQ and the answer is: "GMO defines quality companies as those with high and stable profitablility, and low debt. Please refer to the white paper entitled "The Case for Quality - the Danger of Junk" located in the US Equity section of the site's Library for further detail."

Very vague answer so you do indeed need to see the white paper for more detail and you can find that here. However, in reality the paper doesn't go into a whole lot more detail....The only criteria they include with the previous 2 (high, stable profitablity & low debt) is low earnings volatility. So just figure the stocks are going to fall into at least the top half in each of those categories. You will notice 1 quality that is absent from their definition but you will find in many others (SPHQ) is Dividends...and that can make a dramatic difference.

Based on their holdings here is a sample of stocks that fit their criteria

Oracle Corp. 5.3%

Johnson & Johnson 4.7%

Google Inc. (Cl A) 4.4%

Coca-Cola Co. 4.2%

Cisco Systems Inc. 4.2%

Pfizer Inc. 3.8%

Microsoft Corp. 3.8%

Philip Morris International Inc. 3.5%

Chevron Corp. 3.3%

Express Scripts Holding Co 3.0%

International Business Machines Corp. 2.9%

Procter & Gamble Co. 2.8%

Wal-Mart Stores Inc. 2.7%

PepsiCo Inc. 2.7%

Hewlett-Packard Co. 2.6%

Quoting from the text:

"For major markets with a low risk of default, we therefore estimate an annualized forward-looking 20-year maturity premium of around 0.8%, in line with the long-run premium on the world bond index. We noted above that bonds of this maturity now have an expected real return of close to zero. Since the maturity premium is the amount by which bonds are expected to beat cash, this implies that the annualized return expected from cash over this same horizon is around –0.8%. The real return from a rolling investment in bills is thus likely to be firmly negative, even before tax."

"After adjusting for non-repeatable factors that have favored equities in the past, we infer that investors expect an equity premium (relative to bills) of around 3%–3½% on a geometric basis and, by implication, an arithmetic mean premium for the world index of approximately 4½%–5%."

"Current levels of risk or risk aversion do not therefore justify an equity premium above the long-term estimate of 3%–3½% (relative to bills). Those who argue to the contrary may well have forgotten that equity markets almost always face a wall of uncertainty. We do not live in uniquely uncertain times."

"Because of their slow reaction to information, investors’ decisions reflect past returns and can be characterized by herding. The herding pushes prices higher (or lower) and this can create a feedback loop. Thus, prices may deviate from fundamental value for a long time."

"When stocks are overvalued, the subsequent return can be expected to be lower than in normal times; when stocks are undervalued, the subsequent return can be expected to be higher. The eventual return to normalcy offers profit opportunities to astute investors who are not subject to these behavioral biases ... The weakness of this view is the assumption that investors do not learn about their behavioral biases, and that there are not enough smart, fundamental investors around to prevent

this mispricing from persisting."

"As in the case of equities, there appears to be a tendency towards mean reversion. Buying the bond market at a high coupon-to-price ratio, or at a low price-coupon ratio, has on average been rewarded with superior real returns, as government bond prices have reverted towards the mean. For bonds, like equities, there is historical evidence of mean reversion. ... The key question, then, is whether mean reversion is identifiable only with hindsight, or whether it is apparent and profitably exploitable on an ongoing basis."

"Having examined the long-term historical evidence for return predictability, we conclude that much of the popular evidence for mean reversion is attributable to optical illusions that employ perfect hindsight.