It looks like you're new here. If you want to get involved, click one of these buttons!

Is WB seeing something that we are not seeing in coming years? After all, he is 96 years old.Pg 18. Berkshire Hathaway (fwd P/E 23.4; P/B 1.6; P/E 19 on look-through earnings; WB owns/controls 14%). Stocks are rallying, but Warren Buffett (96) keeps selling, leaving billions on the table. His recent sales seem to be poorly timed. He has almost stopped buybacks. The cash (mostly T-Bills) is now $311 billion (31.1% of market-cap). BRK stock has done well (+28% YTD, and another near-trillion-dollar company) and its operational businesses will benefit from the economic boom. WB has been waiting for an elephant-size acquisition for years, but that $311 billion may just become a nice parting gift from WB to the next CEO, likely Greg Abel (62). A huge uncertainty is what the post-Buffett BRK will look like?

Hey, we listened to you folks crying for 4 years during Obama and 4 years during Biden. You listened to us the last Trump term so we owe you 4 more years of moaning about Trump. Then we'll be back to even so we can start again after the next election. :^)This is fun to listen to the crybabies! Carry on

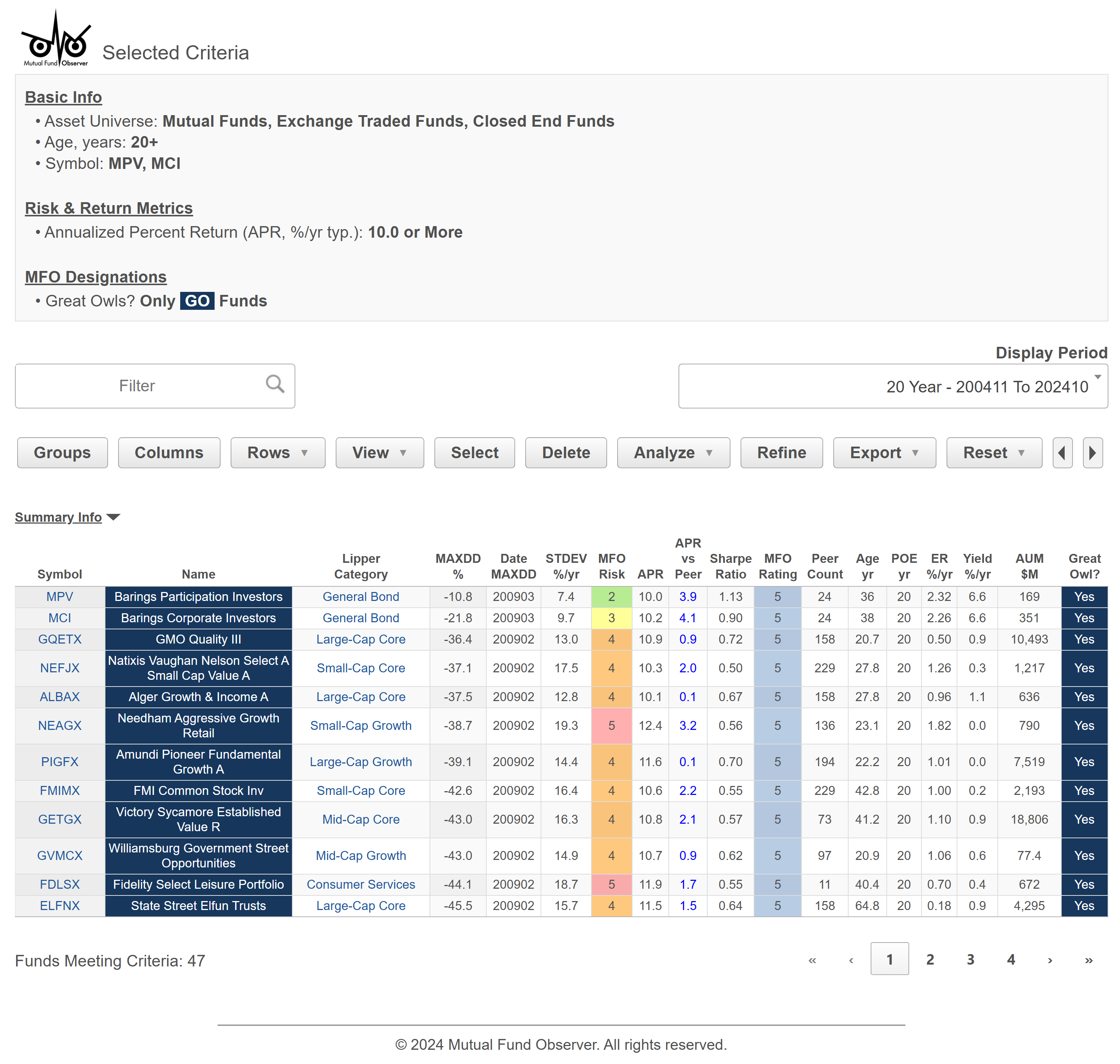

I would have been surprised if it was an alternative. If I knew what went into M*'s definition of quality I'ld be surprised if those factors weren't in MFO Premium. I spent many years working with data, among other things, so running screens is my idea of fun.@WABAC FWIW: The correlation between MRFOX and SPGP is .87 (So it's not really an alternative); MRFOX LT APR is 16.4%; SPGP is 14.4%; STDEV MRFOX 13.2; SPGP 16.4; MRFOX = Great Owl; SPGP No. Also, SPGP has underperformed the SP500 YTD, 1yr.; 3yr.; and 5yr.; but outperformed for 10yr. by .83%. Perhaps this information is helpful. Best.

© 2015 Mutual Fund Observer. All rights reserved.

© 2015 Mutual Fund Observer. All rights reserved. Powered by Vanilla