It looks like you're new here. If you want to get involved, click one of these buttons!

HOW has the stock market returned 8-10% per year? — is a whole another question.

And the mode (i.e. the most common data point), rather than the average, tells that story. And answering HOW means looking at characteristics of individual stock performance through time.

Hendrik Bessembinder did that research. He has looked at the history of about 29,000 stocks in the United States, over the 90 years worth of good data we have for empirical stock analytics. He's also looked, on a slightly shorter time horizon because of available data, at about 64,000 stocks outside the U.S.

The mode is -100%.

The most common outcome from buying a stock is that you lose all your money.

Mind blown? Great. But read on, because it has implications for portfolio design, especially if you're a long-term investor.

do-stocks-outperform-treasury-billsjust 86 stocks have accounted for $16 trillion in wealth creation, half of the stock market total, over the past 90 years.

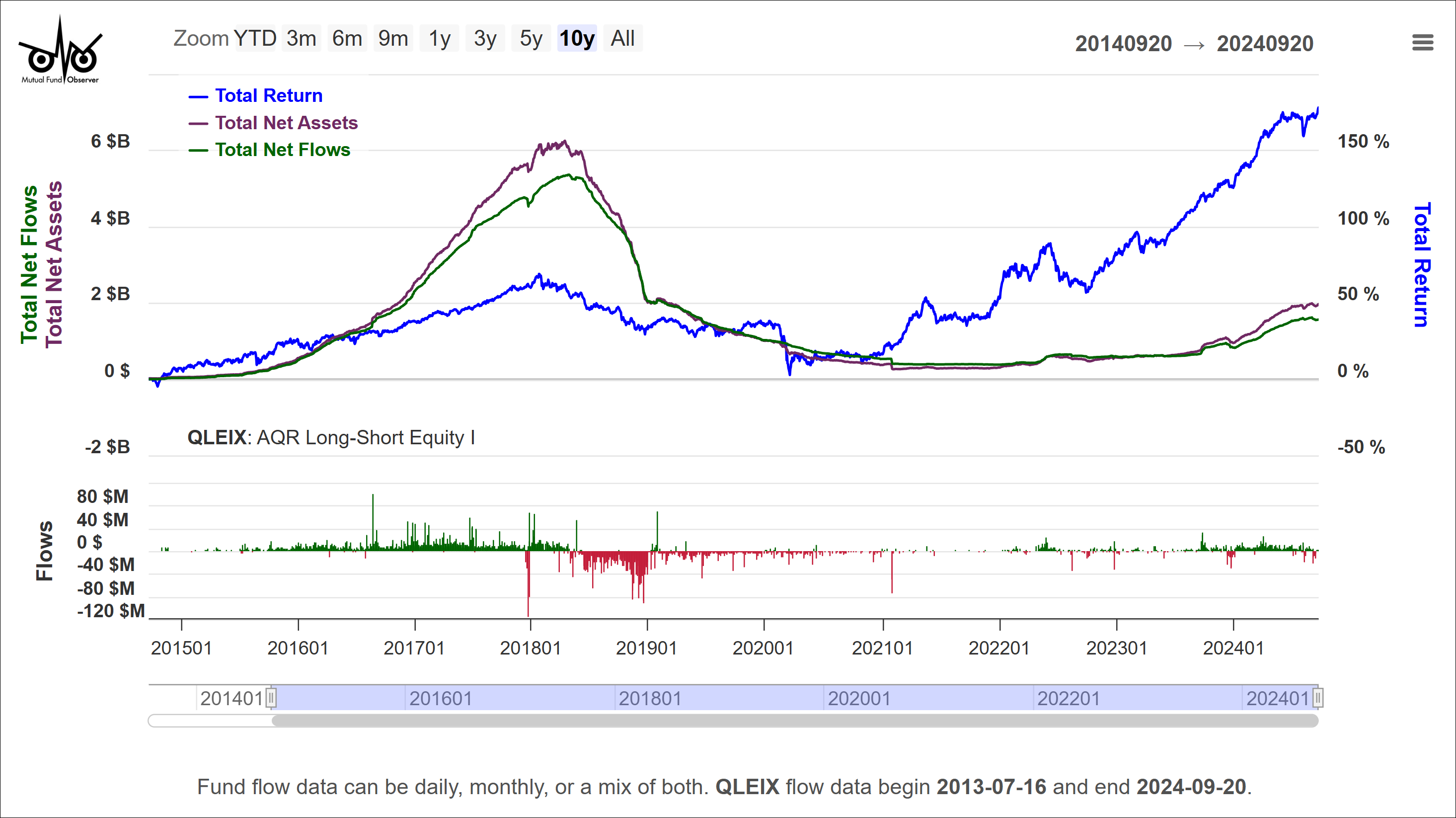

@FD - Have you looked at M* performance numbers? QLEIX +20.71%YTD / +23.75 1 YR. Albeit, it may not have moved much the past 6 months. Since when has 6 months become an appropriate time horizon to measure anything’s performance - except perhaps cash?The 3 years for QLEIX looks good because of 2022. This is where ALT funds excel.

Then, you have years when they trail and way in the back.

BY the time most investors realize markets are going down and load on these funds, they miss most of the meltdown, then, they miss the beginning of the uptrend of the regular funds, which is the strongest period.

It takes discipline to hold funds like that.

© 2015 Mutual Fund Observer. All rights reserved.

© 2015 Mutual Fund Observer. All rights reserved. Powered by Vanilla