Lawrence McDonald: "How To Listen When Markets Speak." Subtitle: Risks, Myths, and Investment Opportunities in a Radically Reshaped Economy.

Almost finished. The case he's making is cogent and crisply, sharply written. A quick read, though very meaty. His thesis is that smart investors, looking forward, must move from growth to value--- specifically into basic materials. Oil, gas. Gold, silver, copper, palladium, platinum.

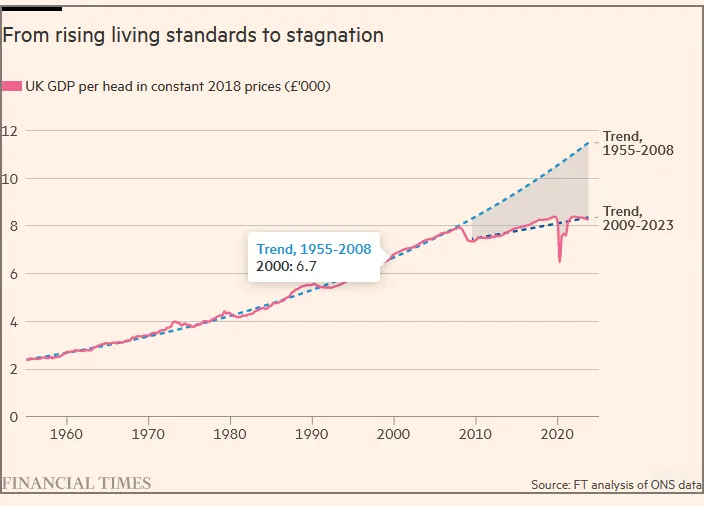

We are in decline, economically. I have said as much for several years, myself. Some of the reason for it is that the world has emerged and grown and thrived, following WW II. We're not the 800-pound gorilla in the room which can throw its weight around the way the USA was able to do, decades ago. A big part of the decline, says McDonald, is geopolitics and overspending Inevitably, the gummint will NOT be able to literally pay down the debt, ever again. It's too massive. In order to handle it, the gummint will have to continuously roll it all over as it matures, and play interest rate games to help cover it.

McDonald has no use for economic sanctions, like the sanctions imposed on Russia and specific Russians, following the Russian invasion of Ukraine. (Crimea was previously stolen, annexed.) Russia has friends in other directions. Most are not even communist. Russia is still feeding raw materials to China so the Chinese can manufacture stuff. Gotta keep the power on. And they're not operating with any "Green Revolution" imposed upon themselves.

I was not surprised, in his treatment of that stuff in particular, that he simply ignored the ethical implications of not responding to the Putin-monster, and just letting him have his way. There is no investing conversation or essay or book which will go near anything to do with ethics. Obama, so I read, confronted Putin at a meeting of big-wigs, and told him flat-out: "We can do stuff to you." Granted, because of the multi-polar economic and political environment today, sanctions are proving to be as useful as trying to use your finger to push a string across the table.

Breathtaking quotations that gobsmacked me:

"44% of all US dollars ever created, were created in 2020 and 2021." Ya, that was the Covid era. But holy jaypers. DEVALUATION, much?????

"The US dollar has lost 93% of its value since the year 1900."

******************************************

McDonald includes summaries of some interviews he's had with some remarkably smart Shining Lights in the Investment Industry. I just finished up reading his account of a conversation with Charlie Munger. Final, distilled thoughts from that meeting actually lifted my spirits. I've made my share of mistakes in investing, but in broad terms, I could take some satisfaction, realizing I'd been doing these things by instinct, for the most part:

Charlie told him: "Trade and invest less. Sit back and wait for those top two or three opportunities that come along each year. Measure your level of conviction and allocate your capital accordingly. Above all, never trade or invest out of boredom or a desire to find something to do. Keep up your high level of passion for markets. Growing wiser is a combination of humility and diligent curiosity. Without the first, the second is useless."

How frequently do you trade? Might Include

- Tactical trades

- Repositioning

- Closing out a fund or other investment

- Acquiring a new fund or other investment

- Portfolio rebalancing

What’s the purpose here? None, except to have some fun. I get the idea folks here trade a lot. My longest stretch without trading something the past 5 years is probably only a month. The core OEFs (7 or 8 funds) haven’t changed in at least a year. But I’ll rebalance a few of them every 6-12 months. It’s “around the edges” (approx. 20% of holdings) that’s held in ETFs, CEFs, individual stocks) that has gotten churned quite a bit.

Anybody out there that hasn’t traded at least once in the last 12 months?

The Federal Reserve. Over many years, Presidents and politicians have..... @yogibearbullAgree fully. Argentina is the 'poster child' of global countries, of how broke everything can become and remain over a very long time frame.

So much corruption, by so many over the

years, that it has become a non-biological DNA.

And the new president's radical, suggested reforms.....

BBC article, February, 2024

The Federal Reserve. Over many years, Presidents and politicians have..... Congress staggered the terms of Fed Chait and US Presidents by 2 years.

A recent tradition is almost monthly meetings between the Fed Chair and the Treasury Secretary (representative of the Administration) to provide regular and orderly communications.

The Fed Chair also as semiannual testimonies before the House and Senate subcommittees.

IMO, no further formal communications are needed for the Administration and the Congress.

Anyone is still free to make a public comments or send letters to the Fed.

The Federal Reserve. Over many years, Presidents and politicians have..... .....expressed desires to have some form of control and/or a large input into the operations of the Federal Reserve.

We all understand the impact of the Federal Reserve and its impact upon the economy, and our investments.

I'm not expressing an opinion; but providing the latest proclamation by a prominent politician.

The statement, August 8: “I feel the president should have at least [a] say in there,” Trump said during a news conference at his Mar-a-Lago residence in Florida. “Yeah, I feel that strongly. I think that in my case, I made a lot of money, I was very successful, and

I think I have a better instinct than, in many cases, people that would be on the Federal Reserve or the chairman.”

Story

HERE.

Go Anywhere Funds… @hank,

@catch22 and other MI residents might be amused to know that FBBAX has approximately 1% of its AUM in KEWL, the Keewenau Land Association. This former forestry products company has considerable subsurface mineral rights. The Upper Peninsula of MI is the ultimate fly-over region (speaking from the point of view of a non-native), but one could imagine a revival if profitable mining returned to the UP. To complement that unusual holding, the fund has Phillip Morris. Go-anywhere does not appear to imply ESG.

I used to tour the UP by road several times a summer. Some beautiful locals on the big water. Other than quick one-day trips to the island for bicycling, I haven’t been back in several

years, Given my “druthers” I’d drive 4-5 hours east from the Sault into Canada. But I digress. Yes - the UP once boasted a thriving mining industry.

To FBBAX - ISTM Phillip Morris is a favorite of funds that emphasize a stable income stream and / or low volatility. Hasn’t been a bad hold in recent

years. (I get the ESG point. Nice job connecting the dots Ben.) Whenever possible, I like to “hold to the fire” any fund I look at by checking how it performed in 2008 - the worst year for equities in my lifetime. FBBAX

lost 30.66% in 2008 (according to Yahoo) which was actually a bit better than its category (and probably better than the S&P). This knowedge, however, does not compel me to want to send $$.

Buy Sell Why: ad infinitum. @hank- now it's important to realize that the bank bond we're referring to has no FDIC or other government backing- it's a regular commercial bond, with Deutsche Bank having an "A" rating, which isn't the top rating. So it can't be directly compared to CDs or Treasuries as far as safety. But it should be just fine, I would have considered something like that also, but we're a fair amount older than Mike, and 20

years is a long time if by some miracle they don't call it in a couple of

years.

January MFO Ratings Posted “Tough Month for Tech”Seems like there was a rather active poster here a couple months back who was really pounding the drums for tech. Derided some regulars who weren’t drinking the

“AI” laced Kool-Aid. Can’t remember his name.

To be fair, a lot of money has been made in tech over the past year(s). I’m not qualified to say whether the sector is attractively priced now (or how it might look in the midst of a recession). But my experience says most market sectors run in cycles. These cycles appear to have become exaggerated / intensified in recent

years due to the technical capabilities at work at trading desks as well as on everybody’s pocket computer.

Thanks

@Charles for sharing these charts. Very helpful.

Buy Sell Why: ad infinitum. FWIW, I picked up a 20 year corporate bond from Deutsch Bank at 6%. It won't be called for at least 2 years (aug. '26), so I'll take the higher return with the expectation it will inevitably be called in 2026.

Deutsche Bank Aktien 6% 08/16/2044 Callable

CUSIP: 25161FXT0

Go Anywhere Funds… Thanks

@BenWPI wonder how the anverage retail investor today would react if his “go-anywhere” fund lost 15% in a year when the Dow, NASDAQ and S&P all gained? Obviously the manager had decided to go somewhere non-mainstream. May have been wrong. May have been a year or two early. Might have built a large position in something while price was depressed.

Real

hedge funds operate a lot differently than retail funds. They attract wealthy clients who can ride out multi-year losses. They impose limits on how much, if any, they can withdraw for the first several

years. And often the operator receives a predetermined % of the gains - adding incentives to take risk. SEC restrictions may be lesser or non-existent. More risk taking. Much different animal.

Go Anywhere Funds… The First Foundation Total Return fund (FBBAX) does fit the moniker of a go-anywhere fund. It invests in an eclectic mix of international equities (49%), domestic equities (26%) and fixed income (13%). Cash is currently around 10%. The equities represent the full range of market caps and styles. The fund has had some top quintile years and some bottom ones as well. My personal take is that “go-anywhere” sounds sexy, but it does not translate into an investment strategy that one would recommend to a good friend or a family member. I don’t mind trying out a niche fund for a while with money I don’t need for something important, which is what I did with FBBAX.

Go Anywhere Funds… If looking for a hedge fund like mutual fund, aka liquid alternative, look into QDSNX. High expenses but AQR has a good bench. If a core fund that does well in down markets, then PRPFX & LCORX are worthy considerations. Invested in PRPFX for my parents over 20 years ago and it's performance in down years is excellent. Still a core holding in the portfolio.

Mr. Market is upset this morning Hey

@OJ, here are the very simple terms in which I understand the whole thing. The FRED high yield spread measure is the yield difference between junk corp bonds and Treasuries. (There's lots of detail on what's counted in the text below the graph.) Junk of course is more credit risky, so you expect a premium in yield to put your $ into junk.

The premium (spread) has been historically small for quite a while, falling from ~6% 2

years ago to ~ 3% recently, which has meant really juicy returns for hi yield over that time. For a while, just about every week, the talking heads on Bloomberg Real Yield have chatted about when and if those spreads will "widen" (increase) and slow down those juicy returns.

Now the spread has shot up to nearly 4% in a matter of days. It took roughly 8 months to go down

from 4% to the low 3's.

Just for reference, back ~ 20

years ago when I was learning about and investing in some HY, the common wisdom was that the spread hitting 4% (on the way down) was a pretty definite

sell signal for HY. Recent

years have blown that assumption out of the water. But what's next?

Sure feels like a phase shift could be happening. Or maybe it's just another big market freakout. In any case, it's unusual to see that much change in only about a week.