It looks like you're new here. If you want to get involved, click one of these buttons!

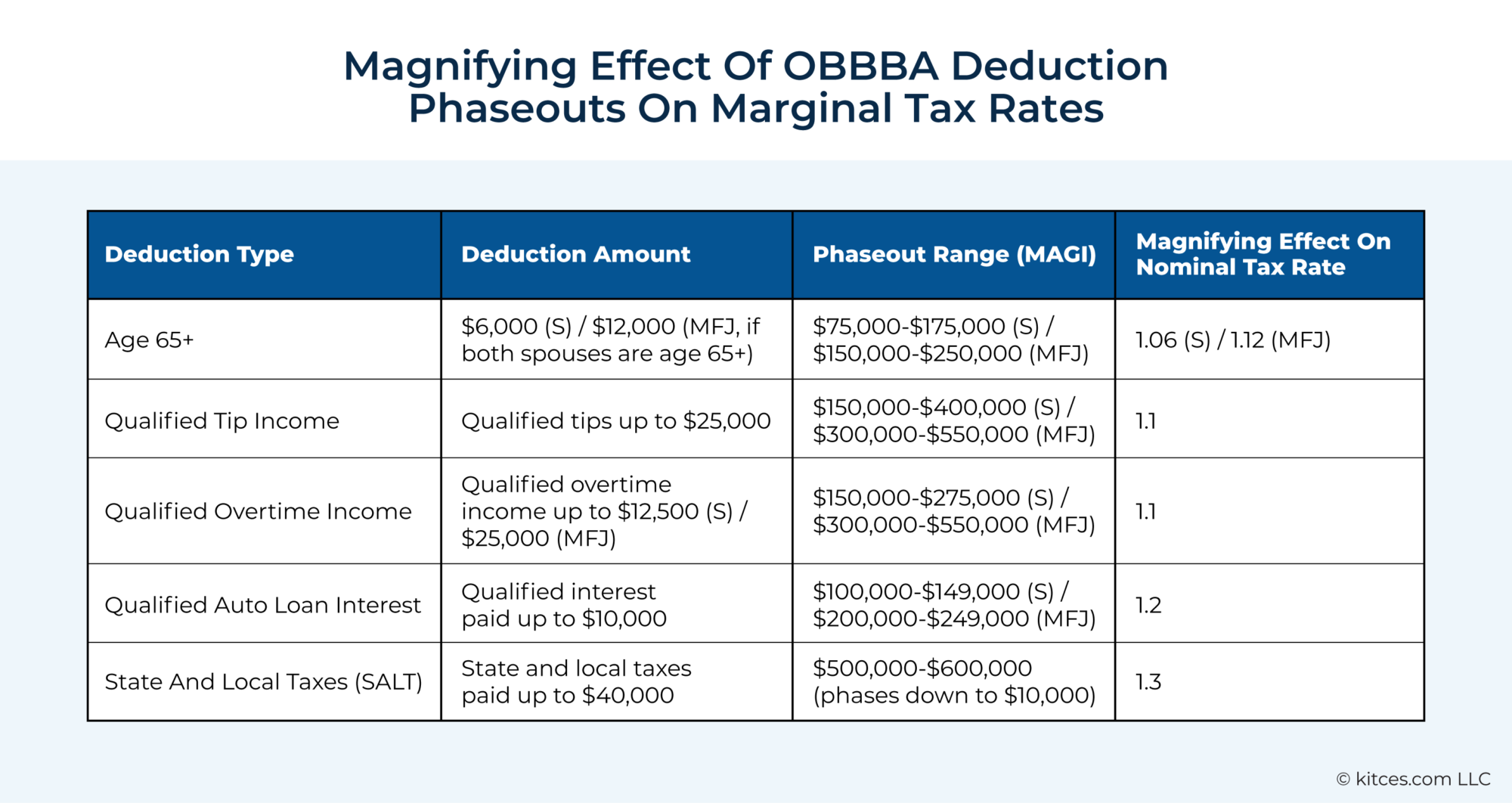

I'm in the process of helping a non-married taxpayer decide on the size of their 2025 Roth conversion. Someone below RMD age who won't need the RMD amounts later. So converting more now is better.It's worth remembering that paying AMT on an ISO exercise creates an AMT credit, which can offset regular tax in future years to the extent that the taxpayer's regular tax exceeds AMT. For clients who receive ISO grants only sporadically or on a one-time basis, paying AMT in one year isn't necessarily a problem if they'll eventually recover it through the AMT credit.

Post of the year @Hank. Thanks for your cogent comments.@hank: Wow. Did the markets turn on a dime today. We’ll see if it lasts.

Um....the markets are in a bipolar state, tending toward nonsense. Stunning shift in attitude today.

Agree. And I think it’s overly-simplistic and non-productive as an investor to attribute market behavior to any single individual whether you love or loath him. Honestly, is this how people invest today? Based on their view of the political leadership?

My sense is many markets have beenexpensive (the nice term for overvalued) for many years (and still are). Depending on one’s time horizon it may or may not be appropriate to own various assets. But to attribute everything to a single individual or party? No. Neither Democrats nor Republicans have control of the economy. Why pretend one party does? Herbert Hoover did not cause the Great Depression and Franklin Roosevelt did not end it (but ramping up for war in Europe had a lot to do with ending it.) Economies have a mind of their own.

End of rant.

Agree. And I think it’s overly-simplistic and non-productive as an investor to attribute market behavior to any single individual whether you love or loath him. Honestly, is this how people invest today? Based on their view of the political leadership?@hank: Wow. Did the markets turn on a dime today. We’ll see if it lasts.

Um....the markets are in a bipolar state, tending toward nonsense. Stunning shift in attitude today.

Am I selling tech? No. It's mostly all in my taxable account, and I mostly bought at much lower prices. I'm not buying either.During the dot-com era, the big infrastructure builders were incumbent telecommunication businesses and global long-haul telcos and equipment names whose regulated local and long-distance franchises generated stable, utility-like cash flows that underwrote the internet and fiber infrastructure capex binge. Today’s infrastructure arms race is driven by the hyperscalers—Microsoft MSFT, Alphabet GOOG, Amazon AMZN, Meta Platforms META, Oracle ORCL—whose reported free cash is increasingly strained by data center and GPU capex, and whose overall earnings quality is propped up by extending server/chip “useful lives” to five to six years, versus the two to three we believe it will be. And they’re treating very large and increasing stock-based compensation as a non-cash item that is being added back to cash flow metrics.

More at the link.Let’s take GPU pricing. You can call up distributors, which have publicly listed phone numbers, and some are authorized Nvidia distributors. My question: Why is the Nvidia H200, which was released late last year, selling at a 50%-60% discount if there’s such a shortage? On Nvidia’s website, they’re selling at $40,000-plus. NetworkOutlet.com quoted $25,900 just a couple of days ago. If there’s such a shortage, why are there tens of thousands available? Nvidia’s latest and most powerful AI chips, Blackwell, are also offered at a discount.

Next, GPU rentals. Why are they in freefall? We’ve gotten quotes at under $4 per hour for Nvidia’s Blackwell GPU rentals. Would you let a $50,000 car rent for $4 if the car only has a three-to-four year life? Meanwhile, [Amazon Web Services] charges around $12-$13 for Blackwell. The bulk of new cloud growth is coming from AI startups. If they’re paying $4 per hour versus $12, then AWS can’t compete. Margins for AWS are already coming under pressure. Revenue growth was OK. Why? Because large tech is also investing in Anthropic, OpenAI, and so on. They go back and buy compute [computational resources] from these guys. Nvidia has invested in over 50 startups, which then go back and buy Nvidia chips.

Many officials at the Federal Reserve did not think the central bank should lower interest rates in December when they voted last month for a second cut in a row, according to minutes from October’s meeting. The record of the latest gathering, released on Wednesday, highlighted a divide that has only deepened since officials opted for a quarter-point cut that brought interest rates down to a range of 3.75 percent to 4 percent. Some policymakers who supported the reduction could have also supported the Fed standing pat, the minutes said, while several were against a cut.

“In discussing the near-term course of monetary policy, participants expressed strongly differing views about what policy decision would most likely be appropriate at the committee’s December meeting,” the minutes said.

October’s decision was already divisive. It featured a rare two-way dissent. Stephen I. Miran, whom President Trump recently picked to join the Fed’s board of governors, again voted for a larger, half-point reduction and Jeffrey R. Schmid, president of the Federal Reserve Bank of Kansas City, voted against any move at all. It was the third meeting in a row in which the interest rate decision was not unanimous.

If the Fed does not cut interest rates next month, that will surely inflame tensions with President Trump, who has repeatedly lambasted Mr. Powell and attacked the politically independent central bank for not lowering borrowing costs as swiftly as he would like. On Wednesday, Mr. Trump revived a threat to remove Mr. Powell before his term ends in May, saying that he would “love to fire his ass.”

The core of the disagreement revolves around how to balance a labor market that has started to show some signs of strain against inflation, which has gained momentum because of Mr. Trump’s tariffs and moved even further from the Fed’s 2 percent target. Some officials appear more inclined to look past the temporary price pressures stemming from tariffs and assume that, over time, their impact will fade. Instead, they harbor much greater concern about companies pulling back on hiring and the prospects of unemployment spiking.

In a separate camp sit officials who worry far less about the slowdown in monthly jobs growth, which they believe is a function of a reduction in the supply of available workers as a result of Mr. Trump’s immigration crackdown. They do not believe interest rates are weighing too heavily on economic growth and instead believe that the Fed should be far more focused on the fact that inflation has remained stuck above the central bank’s target for nearly five years.

New economic data typically plays a pivotal role in helping to resolve outstanding differences between officials and has proved crucial for allowing Mr. Powell to forge broad support for policy decisions. But the recent government shutdown, which stretched on for over 40 days and was the longest on record, has upended the release of a range of monthly reports, including those tracking payrolls growth and inflation. That has meant the Fed has not had a clear view of how the economy is faring since August.

The government data drought will start to ease this week, with September’s jobs report released on Thursday and another metric tracking prices for that month for goods and services that companies use to make products out the next week. The Bureau of Labor Statistics, the agency responsible for collecting the data and publishing its findings, said on Wednesday that it was delaying the release of the November jobs report to Dec. 16, roughly a week after the December interest rate decision. The agency said it would also publish part of October’s jobs report at that point.

Without important data in hand, the December decision looks even more uncertain than it did just a few weeks ago. Several policymakers have already made clear that they do not think the Fed should cut at that point. But the case for cutting still has powerful backers. One of the most vocal supporters is Christopher J. Waller, a governor who is in the running to replace Mr. Powell as Fed chair. In a speech this week, Mr. Waller emphasized that the labor market was near “stall speed” and that inflation concerns were overblown.

True to a degree. I used to play tennis with a guy that sold his business for 10-15 million in 1995. He has been invested in 90+% munis.Winning, as it relates to investing, means having the financial means to achieve your goals.

Beating some arbitrary benchmark is irrelevant.

its the same here. most will say "our guy says we are doing great" and have no idea whether they are or not and are just happy that someone says its doing great.None of my friends like to talk about investing. From the little that they’ve said, it seems that they all use financial advisors. I’ve got no problem with that, but find investing very interesting and would enjoy talking about it.

The Tacoma Narrows Bridge was nicknamed "Galloping Gertie."OMG.

I've seen the videos of Tacoma Narrows failing in the wind!

Bouncing around like a magician's trick.

Holy cow.

© 2015 Mutual Fund Observer. All rights reserved.

© 2015 Mutual Fund Observer. All rights reserved. Powered by Vanilla