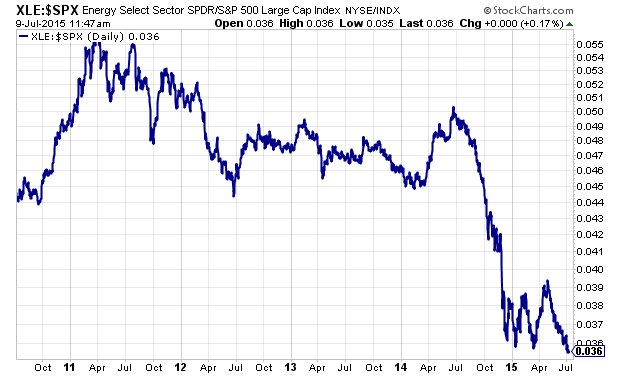

What is interesting is a comparison of the resource (Oil, Natural Gas) and the Energy Service companies (Drillers, shippers, refineries, Midstreams, chemical, etc.).

Low energy prices are like low interest rates for some companies because it lowers their input costs.

Also, frackers are stuck between a fracked rock and a hard place. "Refracking" will be a term we hear being mentioned going forward. It happens when a well is left idle and needs to be reopened. What some "refracked" wells are enjoying is an increase in previous output by as much as an additional 30%.

Storage (contango) will also be a goal for some energy producers.

The Energy sector (VDE, XLE) is one of my bottom fishes:

bottom-fishing-for-funds-and-etfsTicker-------Off 52 wk Low---Off 52 wk highXLE, VDE.....1.42%....................28% - Energy

FCX.............2.87%....................63% - Natural Gas

USO.............11.4%...................

55% - US Oil Producers

UNG.............

5.06%...................46% - Natural Gas

And here's commodities:

GCC............1.8%......................23% - Commodities

Might be a good time to dca (dollar cost average) into these inflation fighting insurance policies. Especially those that have most of their downside worked into the price and still pay a dividend.

In my opinion, "cheap" dividend paying stocks can act like bonds.

Finally,

"A strong dollar also has a negative impact on the oil price, which rebounded this spring as the dollar went

through a period of temporary weakness. Brazil and Russia, both major oil exporters, would go through

another round of pain if oil heads back down. Manufacturing-focused countries in East Asia, among them

South Korea and Taiwan, would likely benefit from cheaper energy."

Source:

USAA Investment_Outlook_Mid_Year