It looks like you're new here. If you want to get involved, click one of these buttons!

From Fidelity:For investors looking to actively position their portfolios in anticipation of a turn in rates, here is a look at 5 asset classes and investments that have historically performed well when rates fall. Of course, past performance is no guarantee of future results.

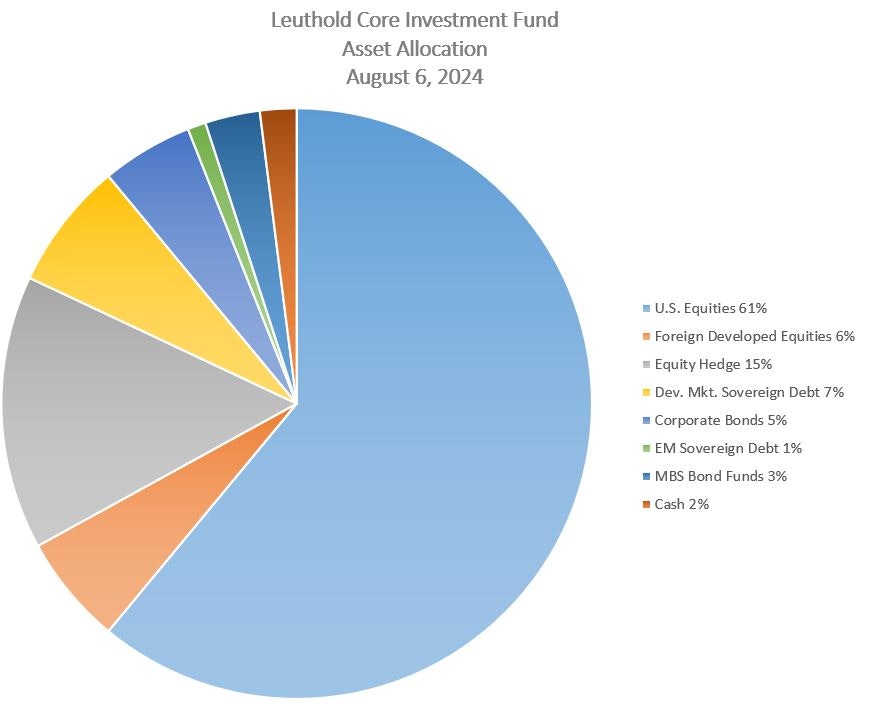

66% gross, 51% net, I'd guess.

66% gross, 51% net, I'd guess.This was along my line of thinking as well, but the market seems to be pricing in a bit more. It's not like corporate earnings are hitting it out of the park, and the consumer is wavering.IMO, Fed is not going to drop FF rates in a hurry to 4% or below, unless it sees long term inflation expectations dropping to 2% AND r* at 4% or lower. I can make a case for a total of 50 bps or less cuts this year.

CPI Figures Tee Up September Move for Central Bank

Cooler than expected inflation in July prompted traders to lower the odds of the Federal Reserve cutting interest rates by a half point in September. But Wednesday’s inflation news did clear the runway for the Fed to begin cutting rates, and the size of the September move could depend on labor market data yet to come.

Traders are pricing in a 37% probability that the Fed lowers rates by a half-point after its meeting next month, according to the CME FedWatch tool. The probability was greater than 50% just a day earlier and even higher one week ago. The tool sees a 63% chance of a quarter-point cut.

The Fed might not stop there. Traders expect additional cuts at the two other meetings this year, putting a 44% probability on the Fed cutting rates by a whole percentage point by the end of the year. That implies two additional quarter-point cuts if the September cut is a half-point.

July’s consumer price index rose 2.9% from a year ago, slower than the 3% gain expected. Core inflation not counting food and fuel rose 3.2%. The cost of housing accounted for 90% of the increase in consumer inflation last month.

A broad array of products and services showed price drops, including airfares, down 1.6% from June, men’s suits, sport coats, and outerwear, down 4.2%, and used cars and trucks, down 2.3%. Prices for video and videogame rentals and subscriptions rose 7.6%, while hot dogs rose 4.4%.

What’s Next: The Social Security cost-of-living adjustment for 2025 could shrink to 2.6% from this year’s 3.2% increase, according to Mary Johnson, an independent Social Security and Medicare analyst and former analyst with the Senior Citizens League. In July she forecast adjustment to be a 2.7% increase.

© 2015 Mutual Fund Observer. All rights reserved.

© 2015 Mutual Fund Observer. All rights reserved. Powered by Vanilla