It looks like you're new here. If you want to get involved, click one of these buttons!

@ a 4% SWR that $1.8M would provide $72K of income for spending. Seems like a reasonable retirement spending amount.Americans believe they need to save an average of $1.8 million for retirement

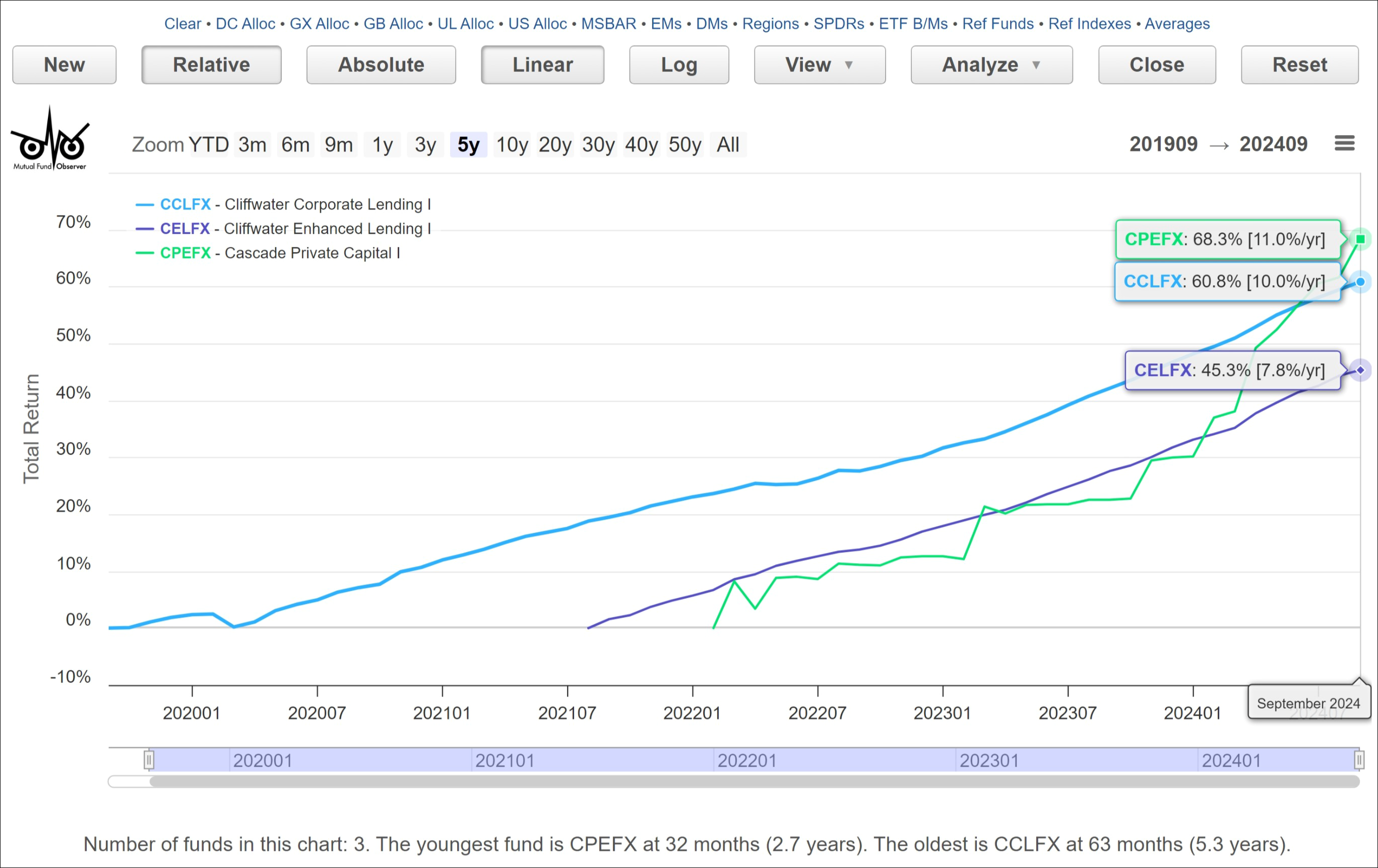

Maybe one is fWAR and the other is bWAR. :)Thanks! That was stupid of me, I even have a view like that set up for exactly that purpose. Though I hadn't included the 30 day SEC yield column before.

Definitions matter. If you look at the M* SPAXX page I linked to, under the "Performance" tab you'll see a one month return of 0.36%.

Now look at the "Chart" tab. Click on the 1M setting. A different gain - 0.37% (actually 0.3727%). At least there we can see that this return is from 9/24/24 through 10/25/24.

Emphasis in original. The contrast between the two descriptions (legacy and brokerage platforms) seems to be saying that all money used for transactions comes out of the settlement account, even if it sits there for only an instant ("until you use it").Your brokerage account comes with a settlement fund that's used to pay for investments and hold assets from investment sales and other transactions. Money from bank transfers or redemptions remains in the settlement fund until you use it to purchase investments or transfer it out of your account.

The first option is to pay for the purchase from the settlement account. The middle option is to "transfer [the] full order amount". This is where Vanguard may be moving money into the settlement account and automatically, instantaneously applying it from there to the fund purchase.If you wish to use your settlement fund to pay for this order, select the amount needed to cover funding option. If you’d like to maintain your settlement fund balance, select transfer full order amount, or select fund order later.

Important, please read

This purchase exceeds the funds available balance in your account’s settlement fund. You must transfer money into your settlement fund within 2 business days. Otherwise, securities in the account may be sold to pay for the purchase, and the account may be restricted from further trading.

That's about the same as FSIXX (4.69%), available at Fidelity w/$1M min, or at Merrill w/$1 (sic) min.And 7-day for SUTXX at Schwab is 4.68%, YTD = 4.08%, also as of 10-25-24.

30 day and 7 day SEC yields measure different things.If M* can be believed the SEC yield for SPAXX is 4.31 to 4.29 for RPHIX though the total return for the latter is still slightly ahead.

© 2015 Mutual Fund Observer. All rights reserved.

© 2015 Mutual Fund Observer. All rights reserved. Powered by Vanilla