It looks like you're new here. If you want to get involved, click one of these buttons!

https://ir.ofscreditcompany.com/shareholder-services/dividend-reinvestment-plancommon stockholders may now receive a number of shares based on 95% of the market price per share of common stock at the close of regular trading on The Nasdaq Capital Market on the valuation date fixed by the Board for such distribution

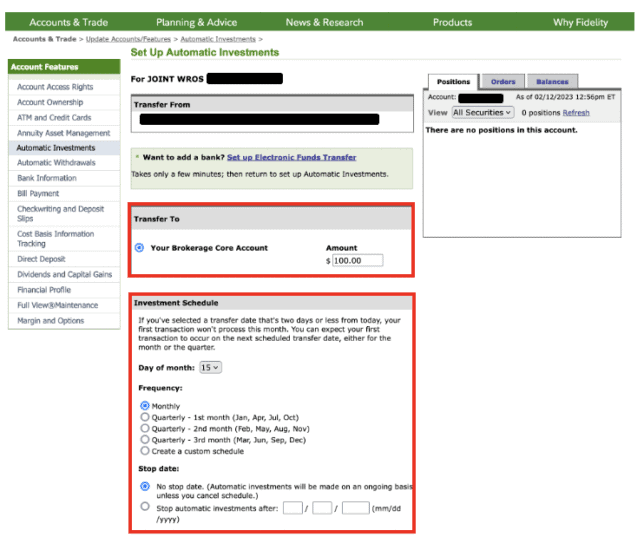

https://www.fidelity.com/bin-public/060_www_fidelity_com/documents/customer-service/brokerage-retirement-cust-agree-and-commission-sched.pdfNote ... that the stock price at which your reinvestment occurs is not necessarily the same as the price that is in effect on the dividend payable date. This is because we generally buy the shares of domestic companies two business days before the dividend payable date [likely now one day before with T+1], at the market price(s) in effect at the time, in order to help ensure that we have shares on hand to place in your account on the dividend payable date.

https://admainnew.morningstar.com/directhelp/Glossary/Performance/Total_Return.htmReinvestments are made using the actual reinvestment price,

NT Ext Eq Mkt Indx Fd DC Lending Tier 5 Not Rated — 0.02

Unlock

1,649,659,963

1,649,659,963

––

Jun 30, 2024

Vanguard Total Stock Mkt Idx Inv 0.43 0.00

Unlock

868,400

0

0.00% Jul 31, 2024

Vanguard Institutional Extnd Mkt Idx Tr 0.38 0.02

Unlock

756,598

4,126

0.55% Jul 31, 2024

Vanguard Small Cap Index Not Rated 0.34 0.01

Unlock

687,760

1,863

0.27% Jul 31, 2024

Fidelity Extended Market Index 0.14 0.02

Unlock

281,449

281,449

––

Jun 30, 2024

Vanguard Small Cap Value Index Inv 0.12 0.01

Unlock

231,593

1,049

0.46% Jul 31, 2024

Vanguard Small Cap Growth Index Inv 0.10 0.02

Unlock

192,865

-735

0.38% Jul 31, 2024

iShares Russell Mid-Cap Growth ETF 0.10 0.03

Unlock

192,396

152

0.08% Aug 28, 2024

iShares Russell Mid-Cap ETF 0.09 0.01

Unlock

181,128

132

0.07% Aug 28, 2024

Russell 1000 Index Fund Not Rated 0.09 0.00

Unlock

174,341

0

0.00% Jul 31, 2024

Blackrock Russ 1000 Eq Idx Composite Not Rated 0.09 0.00

Unlock

174,341

174,341

––

Jun 30, 2024

State St Russell Sm/Mid Cp® Indx NL Cl C 0.08 0.01

Unlock

161,788

116,888

260.33% Jul 31, 2024

Schwab US Mid-Cap ETF™ 0.07 0.02

Unlock

131,950

0

0.00% Aug 30, 2024

iShares Russell 1000 Growth ETF 0.06 0.00

Unlock

128,597

48

0.04% Aug 28, 2024

Fidelity Nasdaq Composite Index 0.05 0.03

Unlock

105,223

30,800

41.39% May 31, 2024

BlackRock Extended Equity Market K 0.05 0.02

Unlock

104,537

104,537

––

Jun 30, 2024

iShares US Technology ETF 0.05 0.01

Unlock

99,370

-39

0.04% Aug 28, 2024

BlackRock Russell 2500™ Index F 0.05 0.03

Unlock

93,367

93,367

––

Jun 30, 2024

Fidelity Total Market Index 0.05 0.00

Unlock

90,922

90,922

––

Jun 30, 2024

Fidelity Series Total Market Index 0.03 0.00

Unlock

68,109

68,109

––

Jun 30, 2024

Total (for Top 20) 2.36 1,654,384,697

1,650,626,972

W/E August 30, 2024..... A week of price swings with few + NAV'sMy intention, at this time; is to present the data for the select bond sectors, as listed; through the end of the year (2024). This 'end date' will take us through the U.S. elections period, pending actions/legislation dependent upon the election results, pending Federal Reserve actions and market movers trying to 'guess' future directions of the U.S. economy. As important during this period, are any number of global circumstances that may take a path that is not expected; and/or 'new' circumstances. In the 'cooking pot' we currently have the big ingredients of the middle east and also, how much damage Ukraine may inflict upon Russia and the response.

Annual income twenty pounds, annual expenditure nineteen nineteen and six, result happiness. Annual income twenty pounds, annual expenditure twenty pounds nought and six, result misery.

It was never possible to replicate his screen at the M* retail level. Years ago he wrote how to approximate his screen with Premium Screener and with some third party screeners.Kinnel seems to imply you have to subscribe to M* Institutional database to run the screen. I haven't tried it in Fund investor. But why publish articles for individual investors based on a screen only available to high end clients?

TRAIX management fee is 59 basis points, still not the lowest quintile. It would have to be below 50 basis points to qualify.PRWCX didn't make the cut because its cost isn't much below average. But TRAIX's is, and it is available to individual Summit Preferred Services customers at T. Rowe Price with a $50K min. ("Must be a share class accessible to individual investors with a minimum investment of no greater than $50,000.")

© 2015 Mutual Fund Observer. All rights reserved.

© 2015 Mutual Fund Observer. All rights reserved. Powered by Vanilla