It looks like you're new here. If you want to get involved, click one of these buttons!

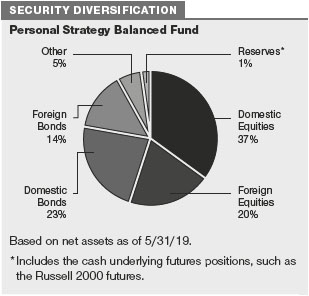

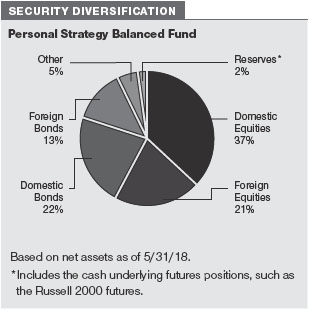

On October 1, 2016, we introduced three new underlying investment strategies to the Personal Strategy Funds. ... The changes include a new allocation to alternatives through a hedge fund-of-funds, as well as initiating an investment in the T. Rowe Price Dynamic Global Bond Fund and an equity index option strategy.

Last year (2022) FBALX lost 18.19%, while TRPBX lost "only" 17.08%. Data from M*.If I recall correctly, the last calendar year in which foreign stocks outperformed US stocks, FBALX still outperformed TRPBX.

https://partners.wsj.com/principal/recalibrating-risk-2023/the-resurgence-of-international-equities/2022 was a difficult year for equities around the world, and U.S. stocks were harder hit than international stocks. The S&P 500 Index fell 18% while the MSCI World Ex-USA Index declined 14%.

30% of stock invested abroad or at least used to benchmark. (18%/60% stock allocation = 30%)Combined Index Portfolio is a blended benchmark composed of 60% stocks (42%-48% Russell 3000 Index and 12%-18% MSCI All-Country World ex USA Index), 30% bonds (Bloomberg Barclays U.S. Aggregate Bond Index), and 10% money market securities (FTSE 3-Month Treasury Bill Index) through 7/1/08. As of 8/1/12 the blended benchmark was composed of 60% stocks (42% Russell 3000 Index and 18% MSCI All-Country World ex USA Index), 30% bonds (Bloomberg Barclays U.S. Aggregate Bond Index), and 10% money market securities (FTSE 3-Month Treasury Bill Index). The indices and percentages may vary over time.

https://www.morningstar.com/articles/136400/fund-times-vanguard-energy-reopens-and-expands-teamFidelity will launch a new fund, Fidelity International Small Cap Opportunities, per an SEC filing dated May 6, 2005. The fund, which will also come in Fidelity Advisor flavor, will invest across regions and countries in companies with market capitalizations of $5 billion or less. Andrew Sassine, who joined Fidelity as an analyst in 1999, will helm the new offering. Expenses for the no-load shares are expected to be 1.39%, which is lower than its typical foreign small/mid-growth category rival's 1.67%. The A share option will cost 1.73%, and is also lower than its typical rival's 2%.

We find this move peculiar, and also unfriendly to the shareholders of the very similar Fidelity International Small Cap (FISMX), which Fidelity just closed on May 5, 2005.

I’d agree with that.TRP’s foreign stock funds have never performed very well, with a few exceptions … .

I pay a lot of attention to Lipper’s ratings. BTW - M* gives TRRIX a “silver” (2nd highest) rating which ain’t too shabby either. I like TRRIX too - or wouldn’t have 10% of portfolio devoted to it. Hard to beat the .49% ER for a pretty diverse basket of managed funds.Lipper loves TRRIX - 5's across the board (except for tax efficiency)

I second the comments posted here. It is SO difficult to find any Foreign funds that perform comparable to Domestic funds. We get our Foreign exposure through a coupla Global funds, and that's it for us. Usually hold about 10% of our stock exposure in Foreign.My experiences with foreign small caps and emerging markets have not been good. I invested in Artisan’s global small cap, and it performed so poorly that they closed it after a few years. I invested in MAPIX, and it was still losing money after more than 7 years. I invested in SFGIX, one of the better EM funds, and it had returned less than 4% annually after more than 11 years. These kind of funds tend to get destroyed in down markets, and it happens quickly.

I’m through investing in foreign SC and EM now, unless some of my broader foreign funds invest in them. My advice to anyone considering these markets, is to be prepared for a long wait before making any money— unless you get lucky with your timing. I’ll be 70 in January, and I might not live long enough to see them make money. Good luck!

© 2015 Mutual Fund Observer. All rights reserved.

© 2015 Mutual Fund Observer. All rights reserved. Powered by Vanilla