It looks like you're new here. If you want to get involved, click one of these buttons!

Comment: Knowing Trump, I'm sure he's using this paper loss to offset actual income somehow, somewhere.Stock plunge wipes out Trump Media’s extraordinary market gains

Shares in Trump Media & Technology Group (TMTG ), owner of Truth Social, closed below $17 on Wednesday, reversing all their gains since the company’s rapid rise took hold in January.

The former president has been prohibited by a lock-up agreement from starting to sell shares in the firm until late September. While his majority stake in the firm is still worth some $2bn on paper, its value has fallen dramatically from $4.9bn in March.

As a business, TMTG is not growing rapidly. It generated sales of just $4.13m in 2023, according to regulatory filings, and lost $58.2m.

Nor is Truth Social growing rapidly as a platform. While TMTG has not disclosed the size of its user base, the research firm Similarweb estimated that in March it had 7.7m visits – while X, formerly Twitter, had 6.1bn. That same month, however, TMTG was valued at almost $10bn on the stock market.

First, you take things out of context. If you want to present what I do, please be accurate. The 3% loss is only for bond funds + a tedious trading + selling to MM in high risk markets.If you followed FD's guidance, you regularly purchased and sold funds

at very opportune times and never experienced losses greater than 3%!

What's not to like?

Easy, peasy... ;-)

When US LC are not doing well (2000 - 2009), it's an easy way to lose money for years!

However, FD does not believe in diversification (regardless of the empirical data)

and would like everyone to know he wouldn't be caught dead in an underperforming fund

for any appreciable length of time.

Might be worth a gambit at $15.98. I see a reasonable chance the election ends up in the courts. Stock would soar briefly in that event. Then sell it fast before the final verdict is rendered.Some would say $1 is quite generous.

It was irregular. The following are not the "norm" either...losing twice 40-50% during 2000-2009 or BND making only 1.7% annually for 10 years or QQQ making over 1600% since 04/2009.The Bloomberg Aggregate Bond Market Index, which BND tracks, dates back to 1976.

Let's put this in perspective.

Prior to 2022, the index experienced only four calendar year losses:

1994 - (-2.9%)

2013 - (-2.0%)

2021 - (-1.5%)

1999 - (-0.8%)

The Bloomberg Aggregate Bond Market Index's 13% loss in 2022 was, by far, its largest loss ever.

The performance that year was highly irregular.

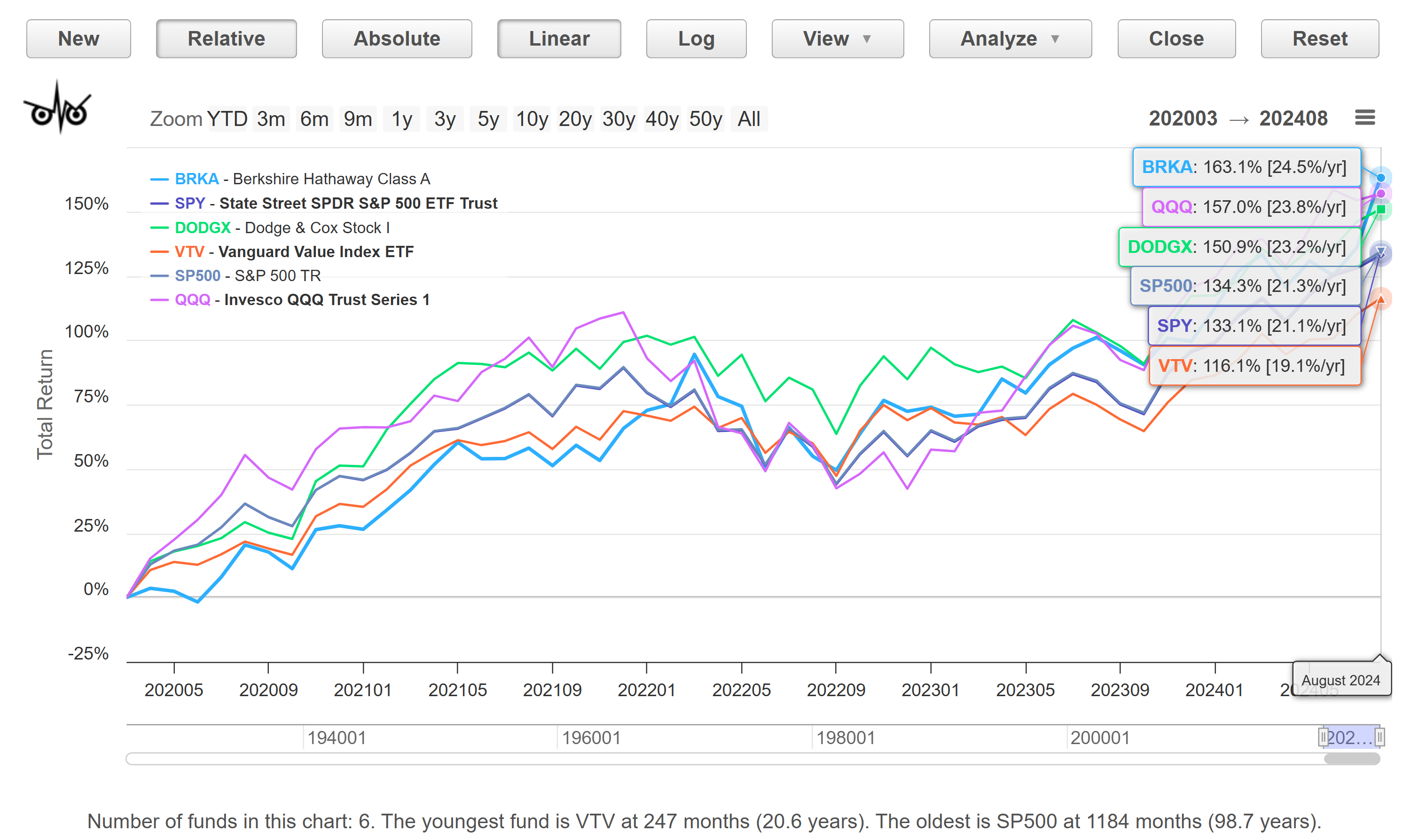

For years now the top high tech drove the US stock market to new highs and much more than international, SC, and value. You could used SPY,VOO or QQQ was better. These companies are globally well known.I do my best to steer clear of The Crowded Trade. It's fun, too, to uncover a good stock that's not getting much or any attention. No more penny stocks for me, though. Diversify, but do not di-worse-ify. Growing cash at the moment. Bullish, but valuations are very high. My plan is to let my stuff ride. When there's a pullback, I'll buy.

It's still $15.98 overpriced though....DJT closed at $16.98 per share, down another 6% today, Wednesday Sept 4. It's obvious that Biden and the Democrats HAVE RIGGED THE STOCK MARKET TOO !!!!!

© 2015 Mutual Fund Observer. All rights reserved.

© 2015 Mutual Fund Observer. All rights reserved. Powered by Vanilla