It looks like you're new here. If you want to get involved, click one of these buttons!

Thurs, Dec 11 6:30-8:00MoMath is pleased to announce the 2025 edition of Simplified, a lecture honoring the memory of Peter Carr, a Founding Trustee of the National Museum of Mathematics.

The Black-Scholes-Merton model transformed finance by showing how to value an option using expected payoff and stochastic calculus. But just five years later, Stephen Ross proved that no probability was required at all — just a careful accounting of prices and cash flows over time. In this talk, Keith Lewis revisits and extends Ross’s breakthrough, offering a clean, intuitive framework for understanding derivative valuation. By treating cash flows and prices as equal components of any trading strategy, Lewis shows how we can model and manage risk without heavy technical machinery. Whether you're steeped in quantitative finance or just curious how modern markets really work, this talk offers a simplified (and powerful) lens for understanding the mathematics behind the money.

the-game-changing-cat-bond-incentivizing-adaptation?srnd=homepage-americasAs the Trump administration stalls federal funding for projects intended to make states more resilient to climate change and private insurers decline to cover properties in high-risk zones, North Carolina just proved there’s another way to fund disaster preparedness: a $600 million catastrophe bond that rewards homeowners and their insurer for installing “super roofs.”

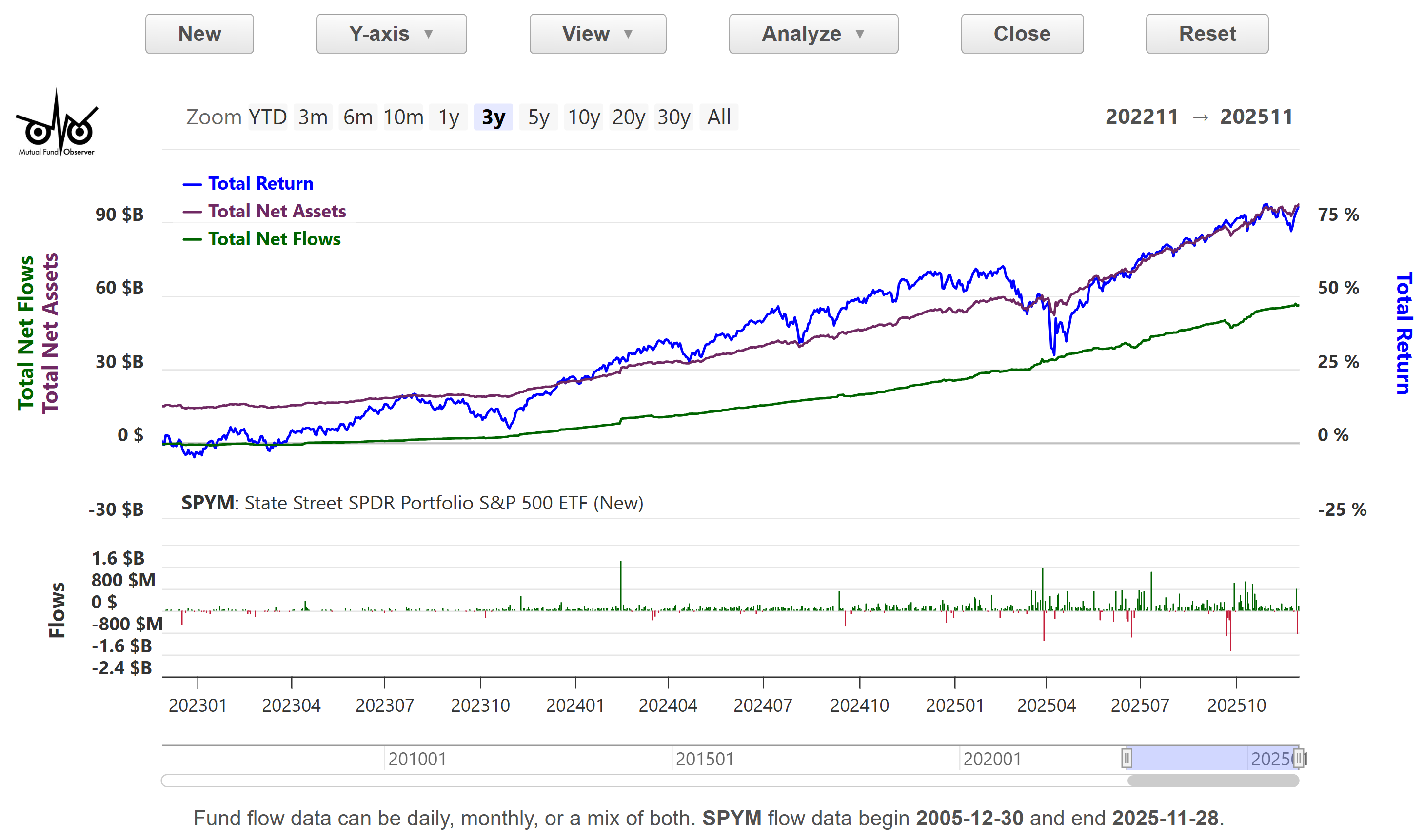

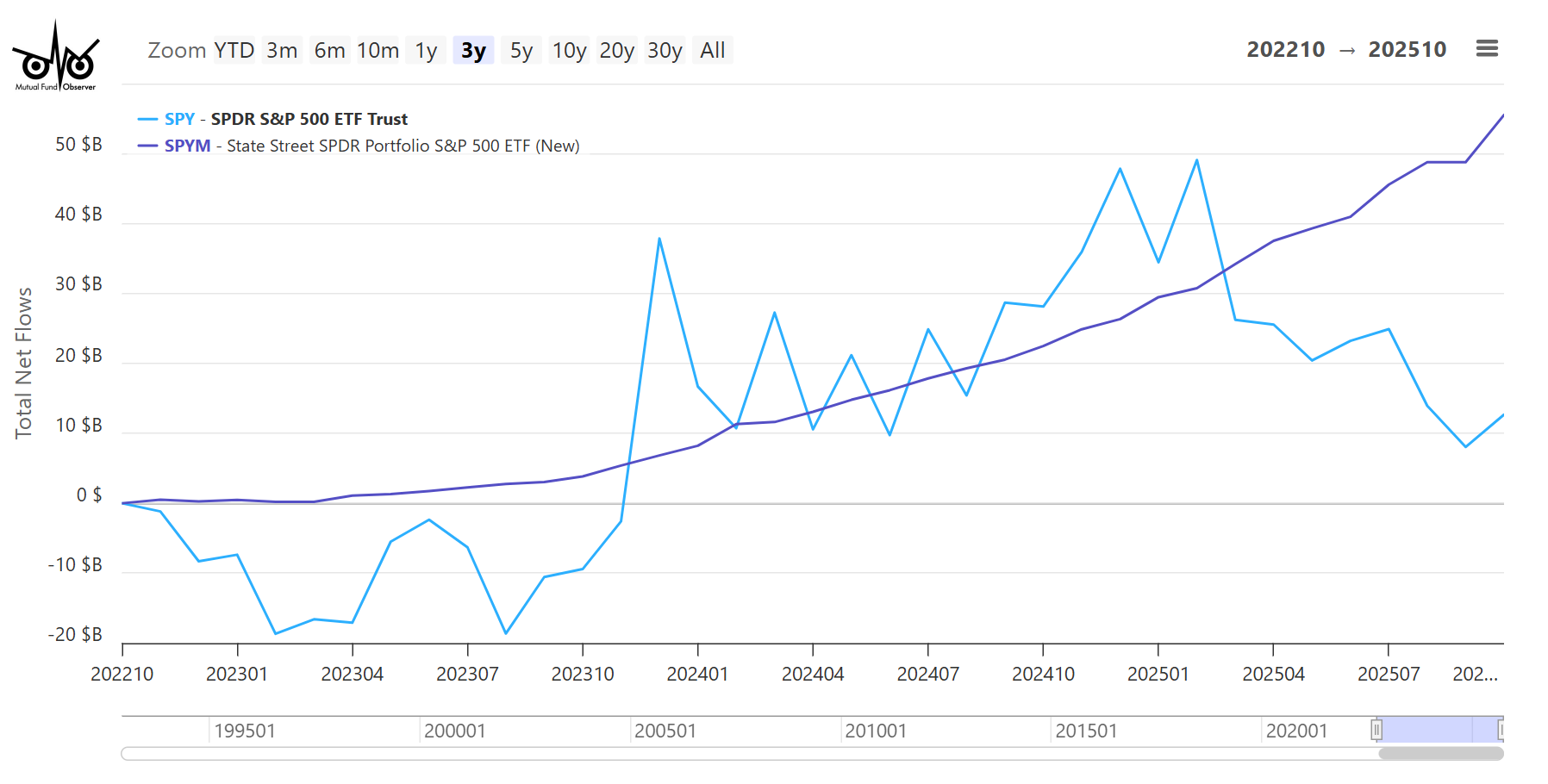

Fidelity and iShares have a partnership deal that goes back around 15 years, before Fidelity created its own ETFs (aside from ONEQ), before brokerages started selling stocks and ETFs commission-free.My own owned ETF is an iShares beast connected to BlackRock. I'm wondering what will happen to my stake in EWS. Paying a fee to buy, sell or add shares is a no-go for me.

https://www.schwab.com/legal/financial-and-other-relationshipsMost NTF funds pay Schwab's standard OneSource/NTF fund fee of 0.40% per year; however, the annual fee can range up to 0.45% of the fund assets held at Schwab. ...

Fees on new institutional class shares acquired or held at Schwab, are typically 0.17% per year but can range up to 0.19%. ...

Most TF funds pay Schwab an annual asset-based fee, typically 0.10% annually of the average fund assets held at Schwab, although the fee can range up to 0.25% ...

In my experience, Schwab is very willing to waive the $75 fee for purchasing Vanguard funds on their platform.How do these etf fees compare to OEF fees charged for brokerage platform availability?

The rack rate for shelf space at brokerages like Fidelity and Schwab is 40 basis points for NTF and a lot lower (10-15 basis points?) for TF funds. Some families get discounts. The brokerages have disclosure statements if you want the exact figures. Funds that refuse to pay to play, like Vanguard are sold with high ($75-$100) transaction fees at these brokerages.

Sure, the Fed can cut rates, but it will be like pushing string.

U.S. manufacturing contracted for the ninth straight month in November, with factories facing slumping orders and higher prices for inputs as the drag from import tariffs persisted.

The Institute for Supply Management survey on Monday also showed some manufacturers in the transportation equipment industry linking layoffs to President Donald Trump's sweeping duties, saying they were "starting to institute more permanent changes due to the tariff environment." They added "this includes reduction of staff, new guidance to shareholders and development of additional offshore manufacturing that would have otherwise been for U.S. export."

/snip

Despite subdued orders for factory goods, manufacturers paid more for inputs last month, a sign that inflation could remain above the Fed's 2% target for a while. The survey's prices-paid measure increased to 58.5 from 58.0 in the prior month.

© 2015 Mutual Fund Observer. All rights reserved.

© 2015 Mutual Fund Observer. All rights reserved. Powered by Vanilla