It looks like you're new here. If you want to get involved, click one of these buttons!

Wow. That is a sneaky way to take another $ 81.00 from you.Another matter some may not be aware of. In addition to your Medicare Part D plan through a private carrier, if your income is above a certain threshold there is a Medicare Part D IRMAA. This varies from $12.90 to $81.00 per month and deducted from your monthly social security check. It doesn’t pay anything for drugs etc. like your private Part D plan, simply a surcharge based on income.

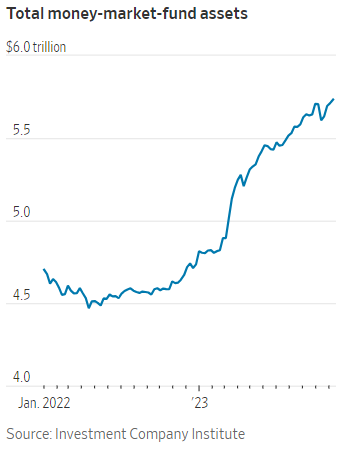

Just saw a Bloomy headline indicating $1T moved from banks to money market mutual funds. If any one has subscription, feel free to post details like how the migration may have impacted bank liquidity, profitability, and solvency. On the flip side, fund companies are minting money with their high ER on MM funds.Given the fungibility of MM AUM and commercial bank deposits, I think bank deposits should be part of the analysis / conversation.

HearI had to go to Google to know what IRMAA is. I guess it means if you are subject to the adjustment, you are more well-off than most people. Appears the government dole is structured so the money goes to the ones who most need it. Hard to argue with that when Medicare is under so much financial pressure.What is IRMAA?

The Medicare income-related monthly adjustment amount, or IRMAA, is a surcharge on Medicare premiums for Medicare Part B (medical insurance) and Part D prescription drug plans. It applies only to Medicare beneficiaries who have a modified adjusted gross income above $97,000 ($103,000 in 2024) for an individual return and $194,000 ($206,000 in 2024) for a joint return. If your earnings are below this threshold, IRMAA doesn't apply to you.

What is IRMAA?

The Medicare income-related monthly adjustment amount, or IRMAA, is a surcharge on Medicare premiums for Medicare Part B (medical insurance) and Part D prescription drug plans. It applies only to Medicare beneficiaries who have a modified adjusted gross income above $97,000 ($103,000 in 2024) for an individual return and $194,000 ($206,000 in 2024) for a joint return. If your earnings are below this threshold, IRMAA doesn't apply to you.

Thank you for contributing towards deficit reduction!Medicare wasn't up big. So, IRMAA? It's painful the 1st year it hits, then one gets used to it. For couples, it's 2x ITMAA.

Yes, IRMAA. Still a bummer. It will only get worse as I get older because of my increasing RMDs.

Yes, IRMAA. Still a bummer. It will only get worse as I get older because of my increasing RMDs.Medicare wasn't up big. So, IRMAA? It's painful the 1st year it hits, then one gets used to it. For couples, it's 2x ITMAA.

© 2015 Mutual Fund Observer. All rights reserved.

© 2015 Mutual Fund Observer. All rights reserved. Powered by Vanilla