It looks like you're new here. If you want to get involved, click one of these buttons!

Just looked at IEI which is 7-10 Treasuries. I’ve decided to stay put. The international etf has a bit in EM bonds. I believe there’s some appreciation potential there as well (but don’t repeat that)7-10 yr Treasury IEF may have the most kick from 10-yr.

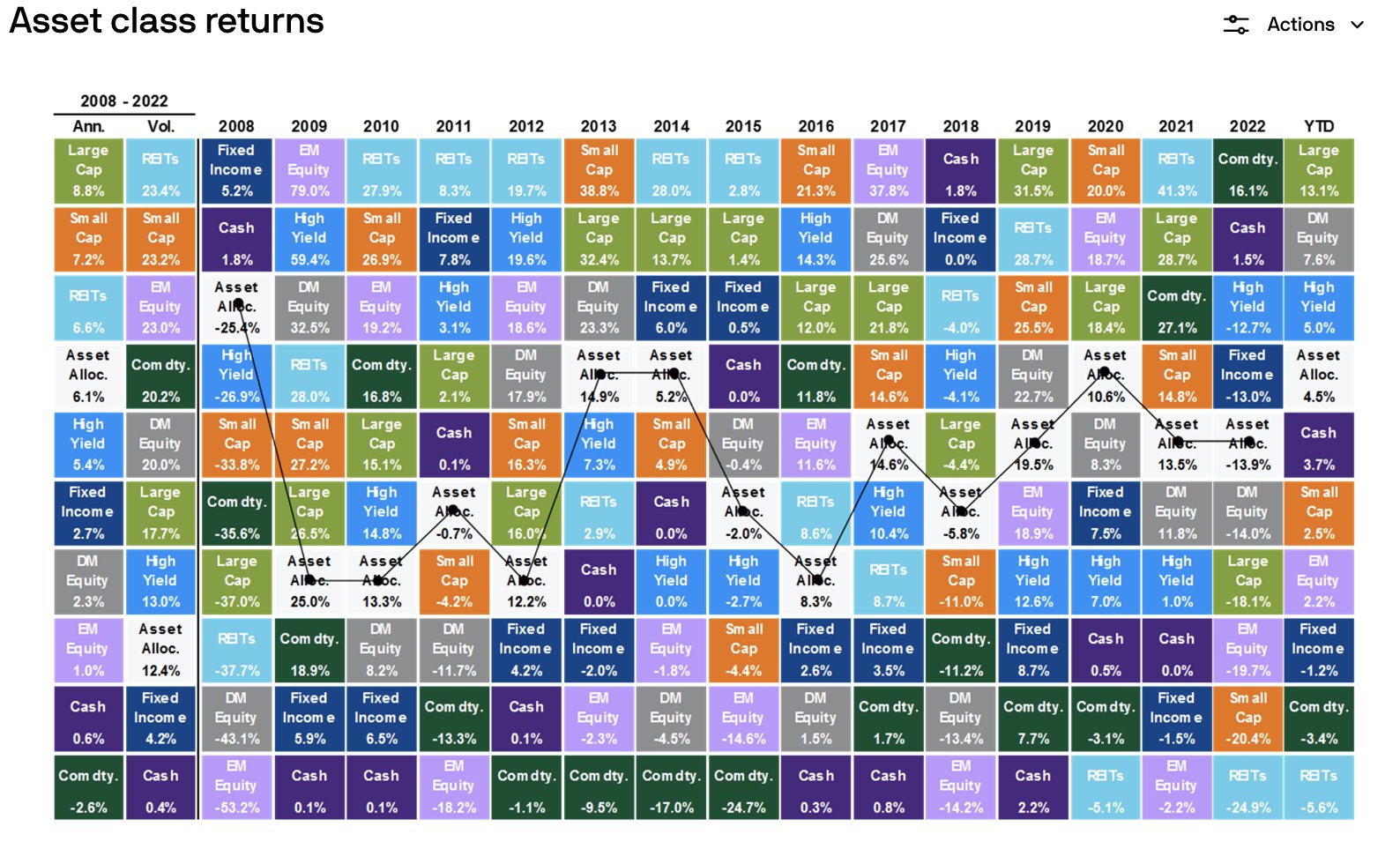

The FT allows subscribers to share a limited number of articles with non-subscribers, so that link should work for folks who want to look at the argument but don't have an FT account.On average, research shows around 100 per cent of their total returns can be ascribed to their choice of policy benchmark [i.e., their strategic asset allocation], along with around 90 per cent of their return volatility. The outcomes of those judgments are often complex.

Jan Loeys, JPMorgan’s veteran asset allocation guru, says in a recent client note that this complexity is both pointless and counterproductive. Pointless, because investors need only two assets: a global equity one and a local bond one, with the relative amounts driven by their ability to withstand short-term drawdowns and return needs. (Less is more when it comes to strategic asset allocation," FT.com, 10/17/2023)

Many investors think that the 20-year is a good buy now. 20 years of 5% interest will work for many folks. But once interest rates start declining you will make a nice CG on the bonds you own. Any kind of market timing is difficult. If one doesn't hit the highest yield, 5% is still great and most likely will be great a few years from now.BTW, the expected yield on the 20-year Treasury bond auction today is 5.156%

© 2015 Mutual Fund Observer. All rights reserved.

© 2015 Mutual Fund Observer. All rights reserved. Powered by Vanilla