It looks like you're new here. If you want to get involved, click one of these buttons!

So how does this help me? Do I want to own the ETF or OEF?Markets also cooperated by being mostly in bullish trend leading to fund inflows. Remember, VG has been the king of fund inflows.

Flipside of the connection between VG OEFs and ETFs is that when there were large redemptions/outflows in 2020 (and in any other years), both the VG OEF and the related VG ETF had similar CG distributions. See the short table below.

Self-standing non-VG bond ETFs didn't have this issue. Much of the benefit from the ETF structure is from the combination of indexing and nontaxable in-kind trading. There are some additional benefits from the VG patented structure of having OEF and ETF classes. VG didn't license its patent to anybody else and others didn't really beg VG for that license. But things may change in/after 2023.

2020 CGs for several VG bond funds

VEDTX /EDV 3.16%

VBLAX /BLV 2.69%

VBILX /BIV 0.71%

VSIGX /VGIT 0.71%

VSBSX /VGSH 0.60%

Ding. Ring that bell. This is not over, yet. If I had a slug of extra cash, I'd throw it in my HY fund, TUHYX. 6.57% yield, but currently a 9.41% SEC Yield. Buy low, sell high. That fund is wayyyyyy down there. Good income producer, about now.This current bump up from the June lows seemed way too easy. Reading the latest Barron's, there's more than a bit of anxiety in the market, and some are voicing this pretty clearly, which I find odd. I'm holding at the moment, waiting. It feels like there's another shoe ready to drop.

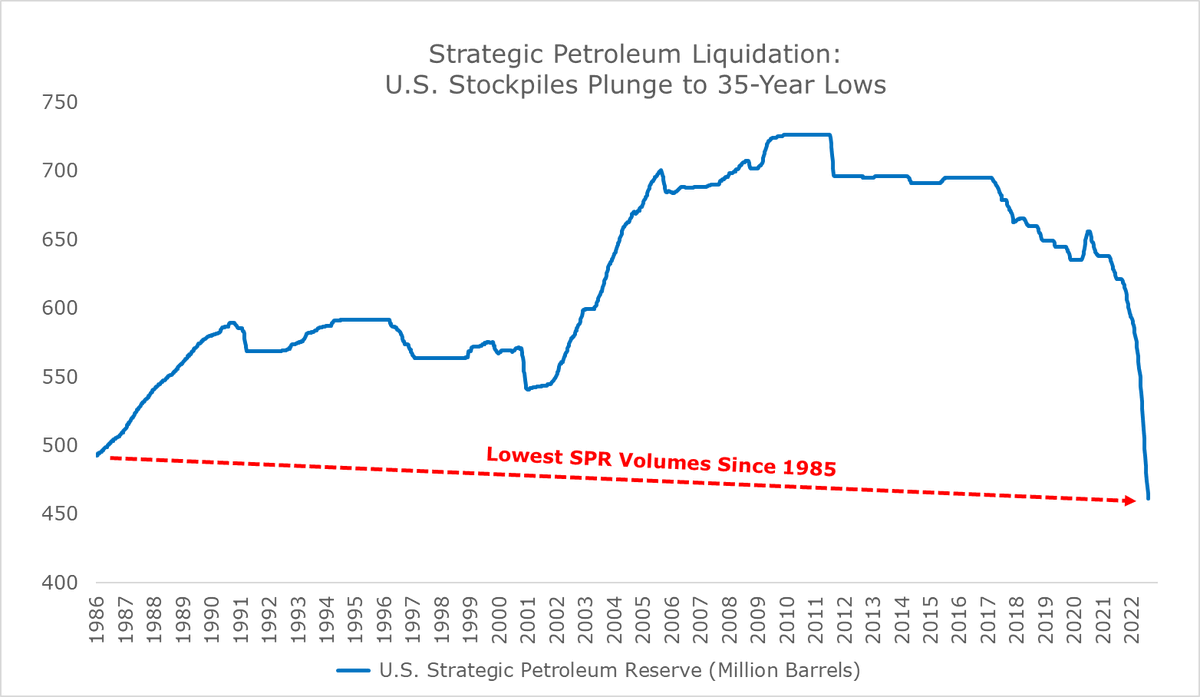

Guy's got an agenda. But I won't argue with the chart provided. WOW. Lowest since '85. Not much reserve left to tap, then.

Notably, we find that 1,050 out of 2,870 funds made a change to their prospectus benchmarks

at least once over a 13-year period. Because we collect data on funds’ benchmarks beginning

in 2005, the first year in which we can detect changes is 2006. The average fund in our sample

reports 1.44 benchmarks per year and makes 0.84 benchmark changes during our sample

period.

Not surprising. I had some choices like that in some retirement plans my employers got us into.Funds that make at least one benchmark

change make an average of 2.27 changes during this period, suggesting that there is a serial

component to this behavior. Funds making at least one benchmark change also report

significantly more benchmarks each year (1.74) than the group of funds that never makes a

benchmark change (1.23).

Same here.PRWCX/TRAIX down -6.1% YTD 8/19/22, but very happy to have bulk of our investments with the fund.

© 2015 Mutual Fund Observer. All rights reserved.

© 2015 Mutual Fund Observer. All rights reserved. Powered by Vanilla