Objective and strategy

The fund seeks long-term capital appreciation by investing in micro-, small- and mid-cap financial services stocks with market caps up to $5 billion. The financial services industry includes banks, savings & loans, insurance, investment managers, brokers, and the folks who support them. The managers anticipate having 40% of the portfolio in non-U.S. stocks with up to 10% in the developing markets. The fund holds about 100 stocks. The managers look for companies with excellent business strengths, high internal rates of return, and low leverage. They buy when the stocks are trading at a significant discount.

Adviser

Royce & Associates, LLC, is owned by Legg Mason, though it retains autonomy over its investment process and day-to-day operations. Royce is a small-company specialist with 18 open-end funds, three closed-end funds, two variable annuity accounts, and a several separately managed accounts. It was founded by Mr. Royce in 1972 and now employs more than 100 people, including 30 investment professionals. As of 12/31/2015, Royce had $18.5 billion in assets under management. $111 million of that amount was personal investments by their staff. When we published our 2008 profile, Royce had 27 funds and $30 billion and slightly-higher internal investment.

Managers

Charles Royce and Chris Flynn. Mr. Royce is the adviser’s founder, CEO and senior portfolio manager. He often wears a bowtie, and manages or co-manages six other Royce funds. Mr. Flynn serves as assistant portfolio manager and analyst here and on three other funds. They’ve overseen the fund since inception.

Strategy capacity and closure

Royce estimates the strategy could handle $2 billion or so, and notes that they haven’t been hesitant to close funds when asset flows become disruptive.

Management’s stake in the fund

Mr. Royce has over $1,000,000 directly invested in the fund. Mr. Flynn has invested between $50,000 – 100,000. All told, insiders owned 5.70% of the fund’s shares as of November 30, 2015.

Opening date

December 31, 2003

Minimum investment

$2,000 for regular accounts, $1000 for IRAs.

Expense ratio

1.53% on an asset base of $26 million, as of July 2023, with a 1% redemption fee on shares held less than 30 days.

Comments

Royce Global Financial Services Fund is a financial sector fund unlike any other. First, it invests in smaller firms. The fund’s average market cap is about $2 billion while its average peer’s is $27 billion. Over 20% of the portfolio is invested in microcap stocks, against a norm of 2%. Second, it invests internationally. About 32% of the portfolio is invested internationally, which that rising steadily toward the 40% threshold required by the “global” name. For the average financial services fund, it’s 5%. Third, it pursues value investing. That’s part of the Royce DNA. Financial services firmly are famously tricky to value but, measured by things like price/cash flow, price/sales or dividend yield, the portfolio trades at about half the price of its average peer. And fourth, it doesn’t focus on banks and REITs. Just 11% of the fund is invested in banks, mostly smaller and regional, and real estate is nearly invisible. By contrast, bank stocks constitute 34% of the S&P Financial Sector Index and REITs add 18% more.

In short: it’s way different. The question is, should you make room for it in your portfolio? The answer to that question is driven by your answer to two others: (1) should you overweight the financial sector? And (2) if so, are there better options available?

On investing in the financial services sector.

Two wise men make the case. Illegal withdrawals specialist Willie Sutton is supposed to have answered the question “why do you rob banks?” with “because that’s where the money is.” And remember all that advice from Baron Rothschild that you swore you were going to take next time? The stuff about buying “when there’s blood in the streets” and the advice to “buy on the sound of cannons and to sell on the sound of trumpets”? Well, here’s your chance, little bubba!

Over the 100 months of the latest market cycle, the financial services sector has returned less than zero. From November 2007 to January 2016, funds in this category have lost 0.3% annually while the Total Stock Market gained 5.0%. If you had to guess what sector had suffered the worst losses in the six months from last July to January, you’d probably guess energy. And you’d be wrong: financials lost more, though by just a bit. In the first two months of 2016, the sector dropped another 10%.

That stock stagnation has occurred at the same time that the underlying corporations have been getting fundamentally stronger. The analysts at Charles Schwab (2016) highlight a bunch of positive developments:

Growing financial strength: Most financial institutions have paid back government loans and some are increasing share buybacks and dividend payments, illustrating their growing health and stability.

Improving consumer finances: Recent delinquent loan estimates have decreased among credit card companies, indicating improving balance sheets.

… the pace at which new rules and restrictions have been imposed is leveling off. With balance sheets solidified, financial companies are now being freed from some regulatory restrictions. This should allow them to make better business decisions, as well as raise dividend payments and increase share-buyback programs, which could help bolster share prices.

The combination of falling prices and strengthening fundamentals means that the sector as a whole is selling at huge discount. In mid-February, the sector was priced at 72% of fair value by Morningstar’s calculation. That’s comparable to discounts at the end of the 2000-02 bear and during the summer 2011 panic; the only deeper discounts this century occurred for a few weeks in the depths of the 2007-09 meltdown. PwC, formerly Price Waterhouse Coopers, looks at different metrics and reaches the same general conclusion. Valuations are even lower in Europe. The cheapest quintile in the Euro Stoxx 50 are almost all financial firms. Luca Paolini, chief strategist for Pictet Asset Management in London, worried that “There is some exaggerated concern about the systemic risk in the banking sector. The valuations seem extreme. The gap must close at some point this year.”

Are valuations really low, here and abroad? Yes, definitely. Has the industry suffered carnage? Yes, definitely. Could things in the financial sector get worse? Yes, definitely. Does all of that raise the prospect of abnormal returns? Again yes, definitely.

On investing with Royce

There are two things to note here.

First, the Royce portfolio is structurally distinctive. Royce is a financial services firm and they believe they have an intimate understanding of their part of the industry. Rather than focusing on huge multinationals, they target the leaders in a whole series of niche markets, such as asset management, that they understand really well. They invest in WisdomTree (WETF), the only publicly-traded pure-play ETF firm. They own Morningstar (MORN), the folks who rate funds and ETFs, a half dozen stock exchanges and Charles Schwab (SCHW) where they’re traded, and MSCI (MSCI), the ones who provide investable indexes to them. When they do own banks, they’re more likely to own Umpqua Holdings (UMPQ) than Wells Fargo. Steve Lipper, a principal at Royce whose career also covers long stints with Lipper Analytics and Lord, Abbett, says, “Basically what we do is give capital to really bright people in good businesses that are undergoing temporary difficulties, and we do it in an area where we practice every day.”

These firms are far more attractive than most. They’re less capital-intense. They’re less reliant on leverage. They less closely regulated. And they’re more likely to have a distinct and defensible niche, which means they operate with higher returns on equity. Mr. Lipper describes them as “companies that could have 20% ROE perpetually but often overlooked.”

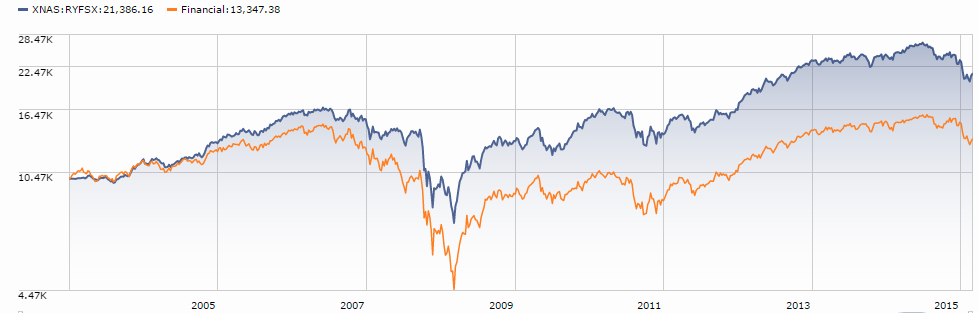

Second, Royce has done well. The data on the fund’s homepage makes a pretty compelling case for it. It’s beaten the Russell 2500 Financials index over the past decade and since inception. It’s earned more than 5% annually in 100% of the past rolling 10-year periods. It’s got below average volatility and has outperformed its benchmark in all 11 major (i.e., greater than 7.5%) drawdowns in its history. It’s got a lower standard deviation, smaller downside capture and higher Sharpe ratio than its peers.

Here are two ways of looking at Royce’s returns. First, the returns on $10,000 invested at the inception of RYFSX compared to its peers.

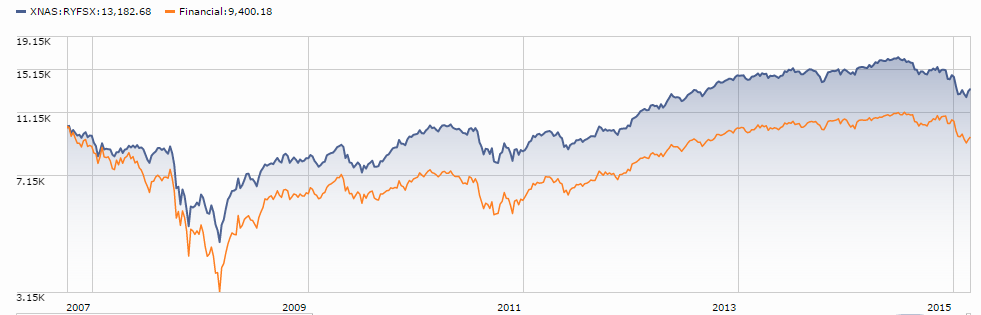

Second, those same returns during the current market cycle which began in October 2007, just before the crash.

The wildcard here is Mr. Royce’s personal future. He’s the lead manager and he’s 74 years old. Mr. Lipper explains that the firm is well aware of the challenge and is midway through a still-evolving succession plan. He’s the CEO but he’s no longer than CIO, a role now split among several colleagues. In the foreseeable future, he’s step away from the CEO role to focus on investment management. And Royce has reduced, and will continue to reduce, the number of funds for which Mr. Royce is responsible. And, firm wide, there’s been “a major rationalization” of the fund lineup to eliminate funds that lacked distinct identities or missions.

Bottom Line

There’s little question that Royce Global Financial will be a profitable investment in time. The two questions that you’ll need to answer are (1) whether you want a dedicated financial specialist and (2) whether you want to begin accumulating shares during a weak-to-wretched market. If you do, Royce is one of a very small handful of financial services funds with the distinct profile, experienced management and long record which warrant your attention.

Fund website

Royce Global Financial Services Fund. The fund’s factsheet is exceptionally solid, in a wonky sort of way, and the fund’s homepage is one of the best out there for providing useful performance analytics.

© Mutual Fund Observer, 2016. All rights reserved. The information here reflects publicly available information current at the time of publication. For reprint/e-rights contact us.