It looks like you're new here. If you want to get involved, click one of these buttons!

Maybe go back a little further to the way uncle Ronny Ray-guns killed the unions. I recall that Joe was actually SUPPORTING unions. But the Orange Kool-Aid winos have been brainwashed to think that anything to help workers is a pinko commie plot. Meanwhile, back at the ranch, Vladimir The Righteous is calling the shots. And the NATO summit today happened without any US presence. Hmmmmmm.

https://www.thestreet.com/automotive/uaw-president-offers-straight-talk-to-workers-on-tariffs

the labor leader said that the country's labor force has been in crisis mode since the North American Free Trade Agreement (NAFTA) was signed and that there is "no other issue "that has affected our economy and working-class people.

"We’re in a triage situation," Fain said on the program. "Tariffs are an attempt to stop the bleeding from the hemorrhaging of jobs in America for the last 33 years.

I haven't watched network news since Network came out. And after 25 years around marine radio traffic I stopped listening to anything but music on the radio.@WABAC,

The cat is out of the bag.

Peter Navarro is on TV right now. He said "Tariffs equal to Tax cuts." If any one was waiting for it to be spelled out, now they have it.

SNL’s ”Weekend Update” on Saturday reminded everyone to set their clocks ahead - “preferably by 4 years.”Will add new unique Display period to MFOP and coin it: Trump 2.0. Will start November 2024. End current month or until there is a new president.

Above are edited excerpts from a current report in The Washington Post.HONDO, Tex. — Jaylee Williams needed to find somewhere to deliver her son. The 19-year-old knew little about the complicated metrics of who takes what health insurance. But relief for Williams came when they realized Medina Regional Hospital — just 15 minutes from their home — accepted Medicaid, the federal-state program that covers medical costs for lower-income Americans. Provider groups an hour away in San Antonio had refused to take the insurance.

But the lifeline that the 25-bed critical-access hospital offered to Williams could disappear in Hondo and other communities like it. Rural hospitals across the United States fear that massive Medicaid cuts Republicans would have to consider under the current House budget proposal could decimate maternity services or shutter already struggling medical facilities in communities that overwhelmingly voted for Donald Trump.

Nearly half of all rural hospitals nationwide operate at a deficit, with Medicaid barely keeping them afloat. Already, almost 200 rural hospitals have closed in the past two decades, according to the Cecil G. Sheps Center for Health Services Research, part of the University of North Carolina at Chapel Hill.

Rural hospital leaders in Arkansas, Colorado, Kansas, Mississippi, Missouri and Texas who spoke to The Washington Post warned that the enormous cuts congressional Republicans are weighing could further destroy limited health-care access in rural America. Proposals to slash up to $880 billion over 10 years — which is expected to be accomplished largely by scaling back on Medicaid — would also affect those who do not rely on the program but do rely on the medical facilities that are financially dependent on the program’s reimbursements.

NOAA's specialized workforce provides products and services that support more than a third of the nation's GDP. But in MAGA narrative, our country will be "saved" by cutting 50% of the 12,000 NOAA workers. Approx. $600M per year in Comp savings....in the scheme of things, a veritable drop in the bucket.

JD wrote: "$600M per year in Comp savings......in the scheme of things, a veritable drop in the bucket."

To paraphrase an old Senator of many years ago, $600M here -- $600M there and before long you are talking about real money.

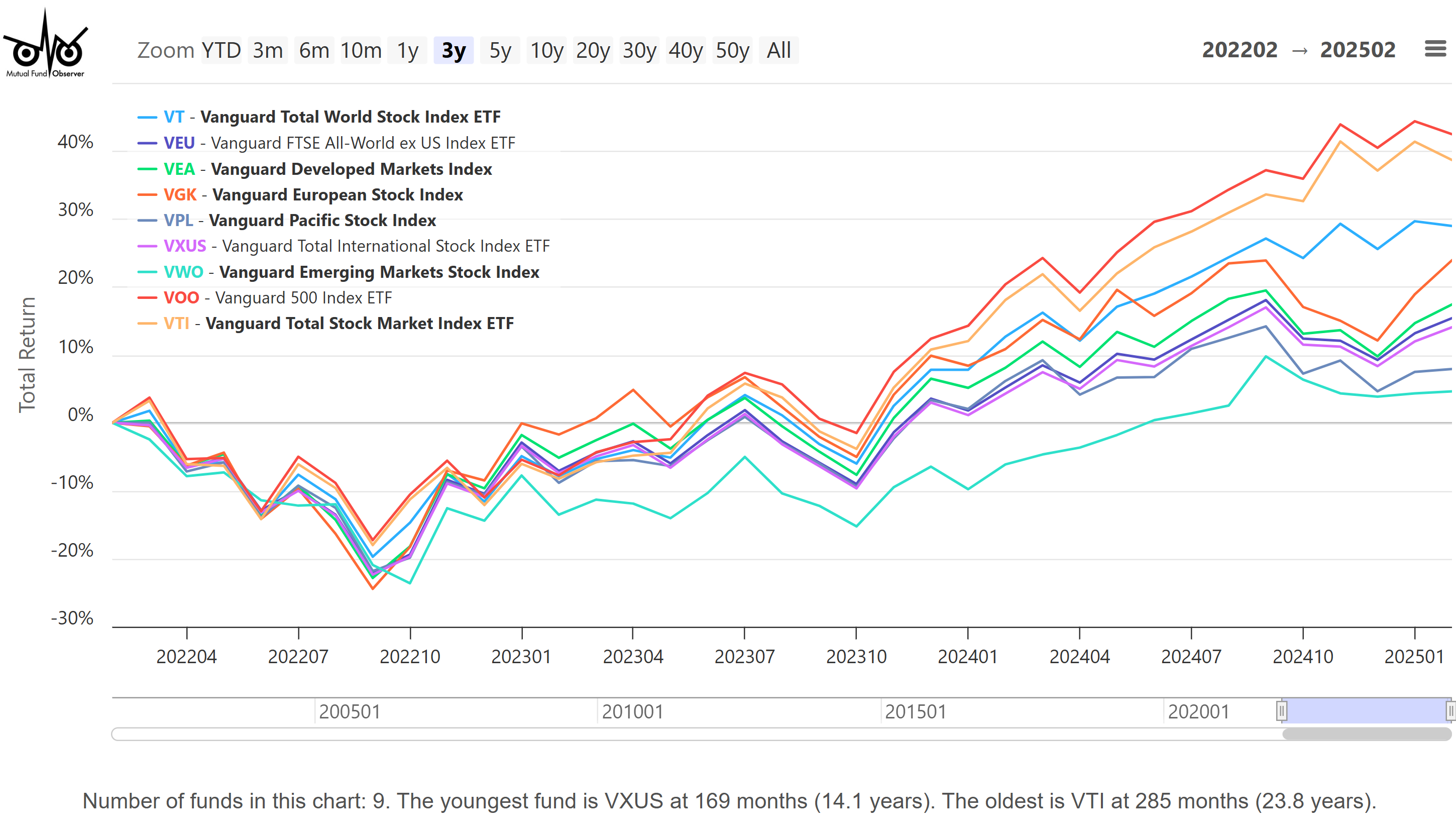

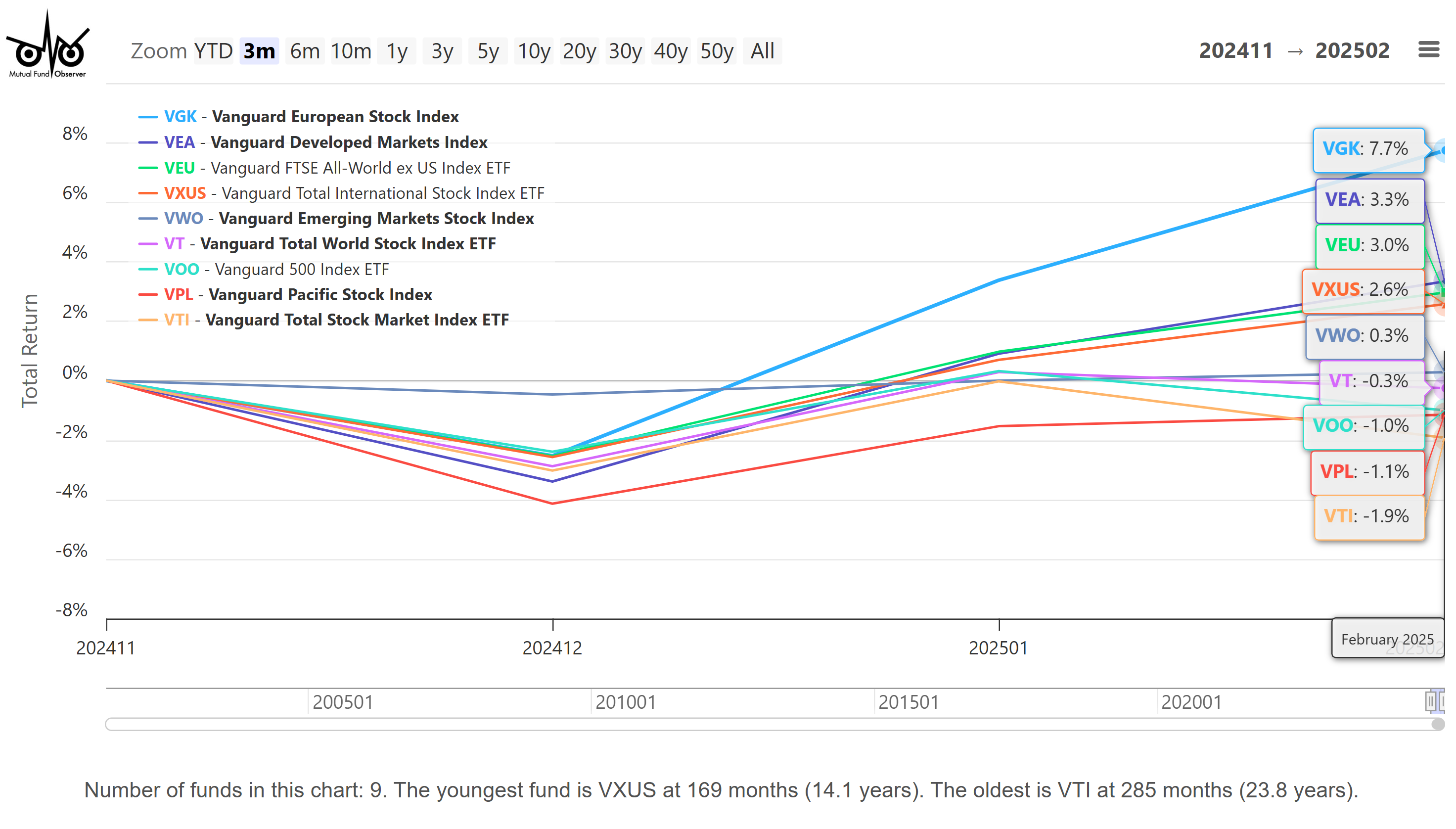

In a sense that tactic of buying when others are fearful has worked for me as well. Dumpster fires and bathwater floods are great places to look for hidden gems rather than racing up the roads to the current sparkles in the eyes of the masses.

I am no where near the abilities of Buffett, Marks or a host of others but my best returns have come from selections made during those times.

© 2015 Mutual Fund Observer. All rights reserved.

© 2015 Mutual Fund Observer. All rights reserved. Powered by Vanilla