It looks like you're new here. If you want to get involved, click one of these buttons!

From CNBC:It also creates a new type of savings account for children – Money Account for Growth and Advancement, or "MAGA" accounts – which the Federal government would automatically open and fund with $1,000 for every US citizen born from 2025 through 2028!

https://www.cnbc.com/2025/05/22/tax-bill-maga-baby-bonus-now-called-trump-accounts-who-is-eligible.htmlUnder the proposal, “Trump Accounts” — previously known as “Money Accounts for Growth and Advancement” or “MAGA Accounts” — can later be used for education expenses or credentials, the down payment on a first home or as capital to start a small business.

Free (hopefully) link to NY Times report.The sprawling domestic policy bill Republicans pushed through the House on Thursday would limit the power of federal judges to hold people in contempt, potentially shielding President Trump and members of his administration from the consequences of violating court orders.

Republicans tucked the provision into the tax and spending cut bill at a time when they have moved aggressively to curb the power of federal courts to issue injunctions blocking Mr. Trump’s executive actions. It comes as federal judges have opened inquiries about whether to hold the Trump administration in contempt for violating their orders in cases related to its aggressive deportation efforts.

It is not clear whether the provision can survive under special procedures Republicans are using to push the legislation through Congress on a simple majority vote. Such bills must comply with strict rules that require that all of their components have a direct effect on federal revenues.

But by including it, Republicans were seeking to use their major policy bill to weaken federal judges. Under the rules that govern civil lawsuits in the federal courts, federal judges are supposed to order a bond from a person seeking a temporary restraining order or a preliminary injunction.

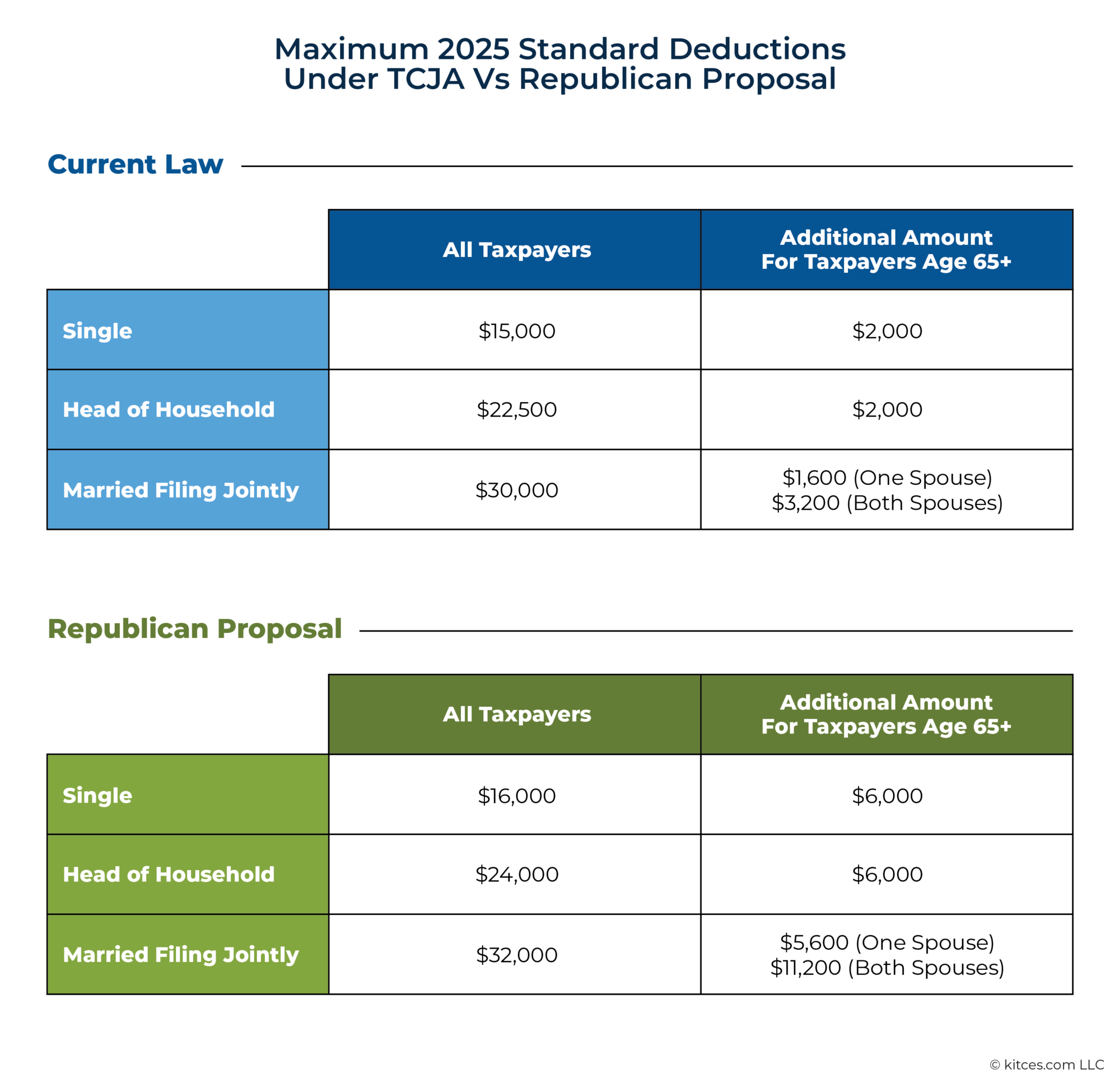

Investor unease over President Donald Trump’s economic program drove the government’s borrowing costs to their highest level in nearly two decades, following House approval of tax legislation that is expected to add trillions of dollars to the ballooning U.S. national debt.

The yield or interest rate on the 30-year Treasury bond briefly topped 5.1 percent Thursday morning, reflecting investors’ demands for greater compensation in return for lending money to the U.S. government.

If yields remain elevated, they will eventually mean higher borrowing costs on mortgages, credit cards and auto loans. Already, the average rate on 30-year mortgages has risen to 6.81 percent from 6.62 percent in mid-April, according to Freddie Mac.

Higher bond yields also are likely to act as a headwind on stocks. The S&P 500 index dropped more than 1.5 percent in early trading after the House passed the president’s tax plan by a vote of 215 to 214 with all but two Republicans in the majority and every Democrat voting no.

Yeah. That’s one word for it.too subtle i guess.

© 2015 Mutual Fund Observer. All rights reserved.

© 2015 Mutual Fund Observer. All rights reserved. Powered by Vanilla