It looks like you're new here. If you want to get involved, click one of these buttons!

Still a youngster - we can collect SS until 150 years old, like those collecting now. ;)

Oh my, all this time I thought/assumed that, originally, it was set up this way so as to avoid taxing state governments. 76 and not to old to learn. ;)

Specificity granularity? Wasn't there an old Star Trek episode about a specificity granularity in the warp drives?To look at the impact of both the Trump tariffs on North American partners and the retaliatory tariffs Trump has planned for other global trading partners, CNBC analyzed data on imports and exports of all 50 states and the District of Columbia provided by LendingTree. ImportGenius provided additional granular data on the products. Using Customs code analysis, each state’s exports and imports with China, Canada, and Mexico were aggregated to specific products. This specificity granularity can show a state’s economic risk exposure which could affect jobs and economic prosperity.

Lots of chewy numbers and details at the links. The CNBC article is behind an ad wall, you'll have to turn off your ad blockers to see it.Consider Montana, which tops the list of states importing from China, Canada and Mexico, with 94% of the state’s total imports coming from these three nations.

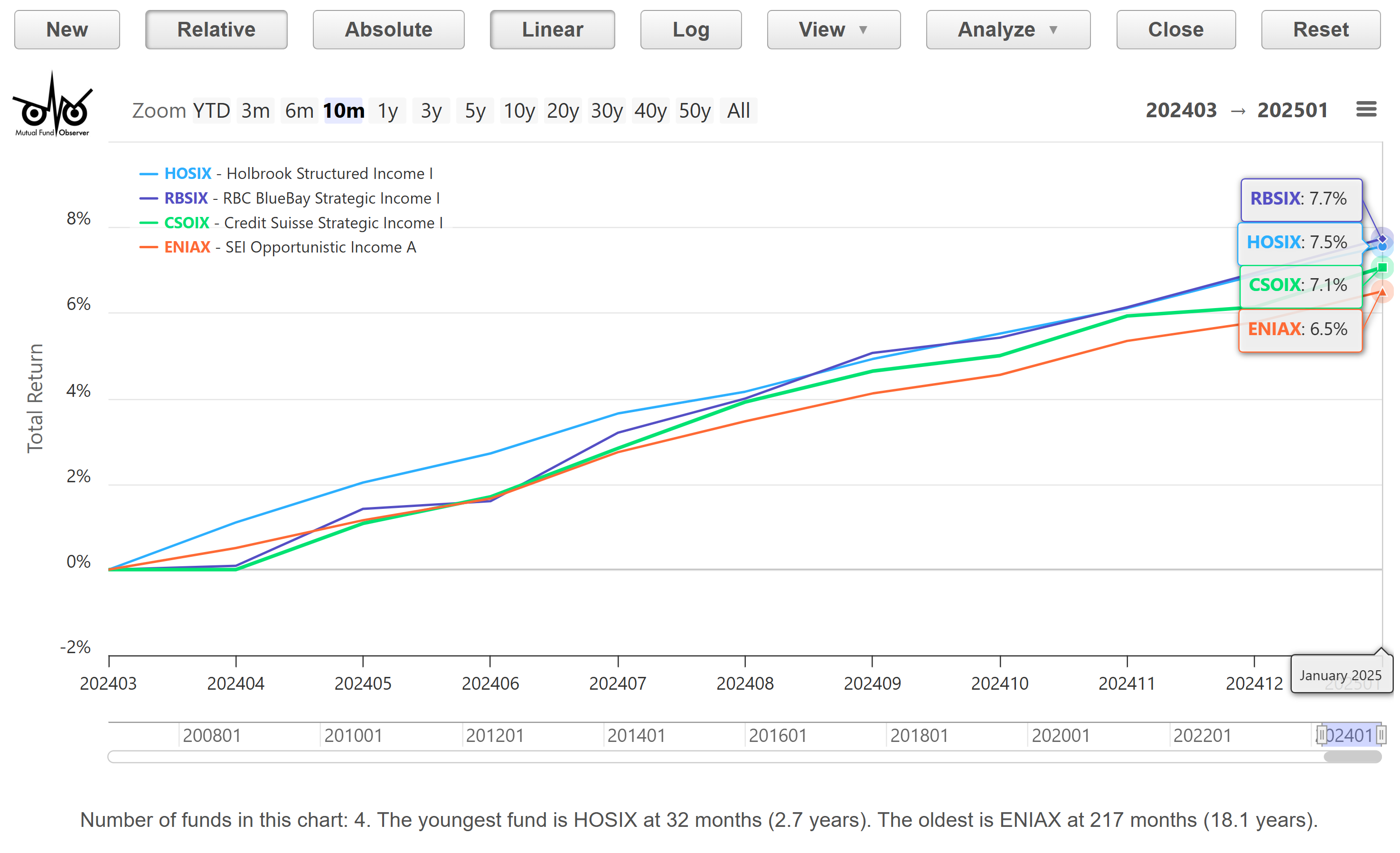

What's the difference between constructing your own "Fund of Funds" and being told by some MFOers that having too many funds is inefficient, wasteful, and self-defeating, as we've all heard here so many times over the years?

© 2015 Mutual Fund Observer. All rights reserved.

© 2015 Mutual Fund Observer. All rights reserved. Powered by Vanilla