It looks like you're new here. If you want to get involved, click one of these buttons!

What's that old saying? Oh, yeah.FWIW, all SELLs (per above posts) have been entered today.

Reduced stock exposure by ~50%.

Parking proceeds in VMRXX, FZDXX and will likely BUY a coupla new rungs on 5-yr CDs ladder that virtually guarantees a net positive TR in 2025.

Kudos to @larryB for this thread.

(Sadly) Timely and actionable.

EDIT: NOT saying this strategy is correct for anyone other than me and the missus.

BUT, our #1 goal this year, after two monster stock gain years under a REAL president, was to NOT allow the buffoon's asinine fiscal policies (read, orange brain farts) to cause us to be anything but net positive for the year on 12/31/25. And that goal has virtually been guaranteed with these moves today. Plus, we will sleep MUCH better thru year-end!

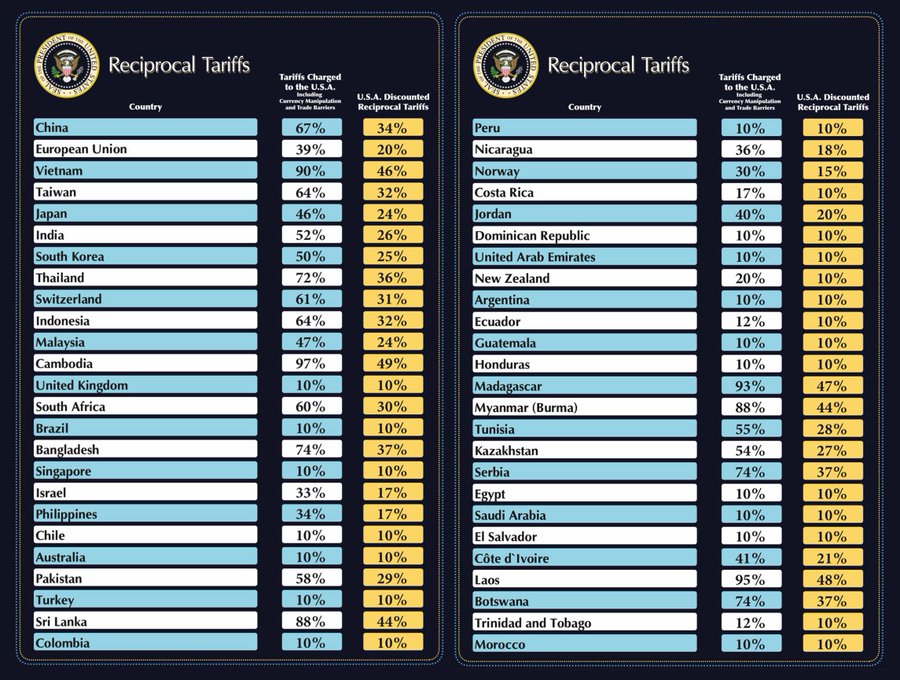

Lots of posts in social-media are pointing this out - that the figures on what tariffs the other countries charge on the US products aren't supported by the other data available. It looks like the White House just calculated each country's trade deficit with the US as % of its total exports to the US (i.e % trade imbalance).https://cnbc.com/2025/04/03/how-did-the-us-arrive-at-its-tariff-figures-.html

From the stable genius..

Perhaps you misunderstood. Perhaps I was not clear. Schwab has it right. Morningstar is in error.Could you say where on Schwab you're looking? What I see as of 9:46PM is:

https://www.schwab.com/research/mutual-funds/quotes/summary/wcpnxNAV Change Net Expense Ratio YTD Return

$9.68 +0.02 (0.21%) 0.65% 2.90%

Quote data as of close 03/31/2025 As of 02/28/2025

April Fools ."I never used momentum indexes; I only used typical funds but looked at the best risk/reward ones and kept changing according to uptrends, and several parameters."

@FD1000,

This may be surprising but the article isn't about you or your "system."

It's about momentum investing in general.

You posted messages very similar to the one from 9:40 PM many times.

There is no need to post the same messages ad nauseum.

Thank you for your consideration!

I can post whatever I want, just as you post daily about tariffs ad nauseum. You may learn something if you pay attention because I have done it.

BTW, why do you post the same thread on 2 different sites?

© 2015 Mutual Fund Observer. All rights reserved.

© 2015 Mutual Fund Observer. All rights reserved. Powered by Vanilla