It looks like you're new here. If you want to get involved, click one of these buttons!

CME FedWatch indicates there is an 87% probability of a 25 bps rate cut at the Dec. 10 Fed meeting.

7-Day Yields as of 12/03/2025

VANGUARD FEDERAL MONEY MARKET (VMFXX) 3.90%

SCHWAB PRIME ADVANTAGE MONEY INVESTOR (SWVXX) 3.84%

FIDELITY GOVERNMENT CASH RESERVES (FDRXX) 3.69%

FIDELITY GOVERNMENT MONEY MARKET (SPAXX) 3.63%

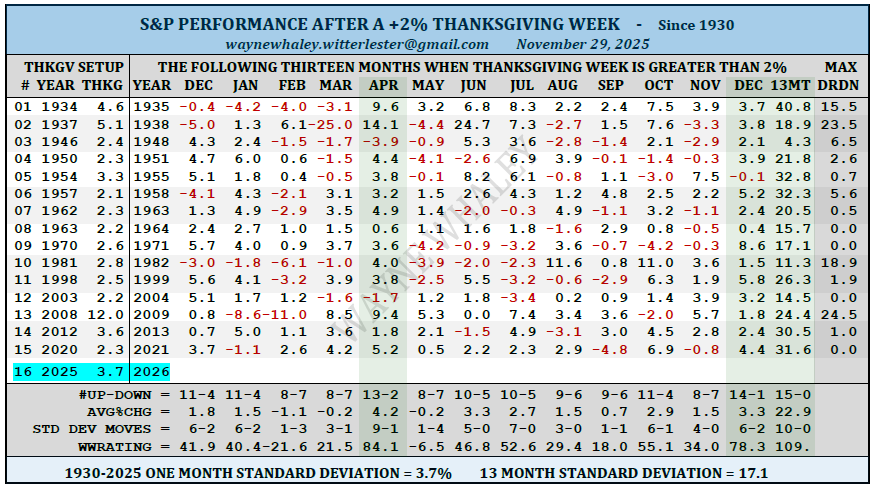

This is my thinking. Call it "mean reversion" or "bubble bursting" or anything at all, it still makes me wary.On the theme of torturing the data...

Typically, when the S&P 500 has effectively doubled (or nearly doubled) in a 3-year window, the subsequent 12 months are often a "hangover" period.

In 6 out of the 7 historical cases, the market either crashed, corrected, or went flat in the year immediately following the peak. The only major exception was the late 1990s Dot-Com bubble, where the market continued to rally for two more years before eventually busting.

...

Summary: History suggests the odds of a negative or flat year in 2026 are elevated, simply because the market rarely sustains a >20% annualized pace for four years straight.

The threat of wild fires was one of the reasons we re-roofed with metal shingles when we were living just down the road from the forests of the Coast Range in NorCal. Another advantage is that they supposedly don't store heat the way traditional shingles do. So we are considering another re-roof in Arizona.Interesting Article on a unique approach by North Carolina's State Insurer "of last resort" regarding the use of CAT Bonds for disaster preparedness for individual NC property owners.the-game-changing-cat-bond-incentivizing-adaptation?srnd=homepage-americasAs the Trump administration stalls federal funding for projects intended to make states more resilient to climate change and private insurers decline to cover properties in high-risk zones, North Carolina just proved there’s another way to fund disaster preparedness: a $600 million catastrophe bond that rewards homeowners and their insurer for installing “super roofs.”

Related Articles:

How 'Super Roofs' Reward Insurers, Cat Bond Investors and Homeowners

NC Expands FORTIFIED Roof Grant Program With Another $20 Million

Thurs, Dec 11 6:30-8:00MoMath is pleased to announce the 2025 edition of Simplified, a lecture honoring the memory of Peter Carr, a Founding Trustee of the National Museum of Mathematics.

The Black-Scholes-Merton model transformed finance by showing how to value an option using expected payoff and stochastic calculus. But just five years later, Stephen Ross proved that no probability was required at all — just a careful accounting of prices and cash flows over time. In this talk, Keith Lewis revisits and extends Ross’s breakthrough, offering a clean, intuitive framework for understanding derivative valuation. By treating cash flows and prices as equal components of any trading strategy, Lewis shows how we can model and manage risk without heavy technical machinery. Whether you're steeped in quantitative finance or just curious how modern markets really work, this talk offers a simplified (and powerful) lens for understanding the mathematics behind the money.

© 2015 Mutual Fund Observer. All rights reserved.

© 2015 Mutual Fund Observer. All rights reserved. Powered by Vanilla