It looks like you're new here. If you want to get involved, click one of these buttons!

https://www.usaa.com/inet/wc/about_usaa_corporate_overview_mainUse of the term "member" or "membership" refers to membership in USAA Membership Services and does not convey any legal or ownership rights in USAA.

https://themilitarywallet.com/usaa-subscriber-savings-account-insurance-policy/All USAA members benefit from the sales to Victory and Schwab. By the end of 2020, USAA will have a new focus on insurance and banking– without trying to handle an investment branch. There might even be a little extra distribution in the Subscriber Accounts.

https://chipfilson.com/2020/01/remembering-long-time-members/We receive two bonus checks annually as part of this relationship [with USAA].

The first for $412 was the annual distribution (dividend) from the Subscriber’s Account, a portion of the capital base for this mutual insurance company. USAA stated that the amount was partly from the sale of their asset management company as well as from their overall net income.

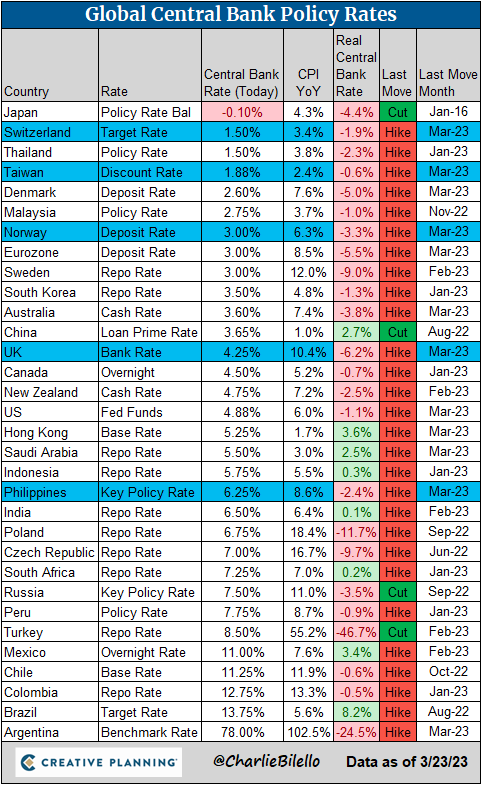

Yup, that's what happened.Multiply you guys x 10 to the umpteenth and you got Silicon Valley Bank.

© 2015 Mutual Fund Observer. All rights reserved.

© 2015 Mutual Fund Observer. All rights reserved. Powered by Vanilla