Using historical data on funds to make assumptions about future performance involves correctly interpreting the trends. Over the past six years, the U.S. has experienced an extraordinarily unusual period:

- COVID bear market (01/2020 – 03/2020) with Quantitative Easing

- Federal budget deficit rising from 4.5% of GDP to 6.3% (2019 to 2025) along with Gross Federal Debt to GDP rising from 105% of GDP to 119% today

- Rising Inflation (05/2020 – 05/2022)

- The Great Normalization bear market (02/2022 – 09/2022)

- Rising rates (03/2022 – 07/2023),

- Quantitative Tightening (11/2022 – ongoing)

- The debasement trade with gold and cryptocurrencies rising (01/2023-ongoing)

- High equity valuations (12/2023 – ongoing)

- Federal Reserve cutting short-term interest rates (09/2024 – ongoing)

- Unprecedented increase in tariffs (04/2025 – ongoing) followed by the April correction

During the next six years, we will probably experience another bear market and modest to moderate inflation. Interest rates are likely to continue falling in the short-term, but not as low as the decade following the financial crisis because of less Quantitative Easing and higher deficits and national debt. High valuations are a headwind to equity returns, and high interest rates are a tailwind for bond returns. In January 2020, before the start of the COVID bar market, the price-to-earnings ratio of the S&P 500 was an elevated 26 and is currently 31. I believe that the full COVID Cycle from January 2020 to December 2021 and 2025 are more representative of market conditions for the next six years than the period from January 2022 to December 2024.

Refining My Target Portfolio

In this article, I explore how alternative investments and mixed asset funds with flexible strategies can be used to develop a conservative portfolio. To evaluate funds, I selected thirty-six funds in twenty-three different Lipper Categories that had good risk-adjusted performance during the full COVID cycle and 2025. I created an optimizer using Excel Solver to maximize the Martin Ratio for the full COVID cycle with constraints for portfolio concentration, minimum returns, drawdowns, yields, allocation to “junk bonds”, and consistency across the individual years and bear markets.

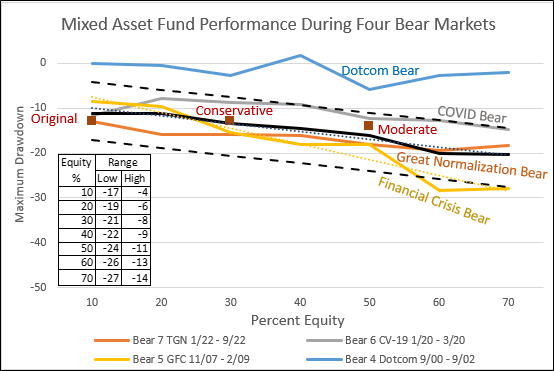

Figure #1 shows the performance during the past four bear markets by allocation to stocks for all of the 461 mixed asset funds in the Lipper global dataset with at least six years of history. Note that the severity of the bear market has a larger impact on the portfolio performance than the of the stock to bond ratio.

The two black dashed lines show a range of likely maximum downturns for the three bear markets, excluding the dotcom bear market, which was associated with a mild recession. The three maroon squares are the maximum drawdowns of the “Conservative” and “Moderate” portfolios that I created and the target portfolio that I described last month in Putting My Conservative Retirement Portfolio on Cruise Control. The two portfolios created for this article had low to average drawdowns.

Figure #1: Mixed Asset Fund Drawdowns During Four Bear Markets

Source: Author Using MFO Premium fund screener and Lipper global dataset.

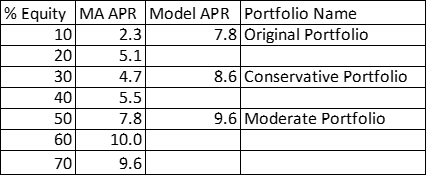

Table #1 shows the average annualized returns over the past six years for the mixed asset funds and the “Conservative”, “Moderate”, and original target portfolio. The two new portfolios outperformed both the mixed asset funds and the original target portfolio.

Table #1: Mixed Asset Fund Returns for Past Six Years

Source: Author Using MFO Premium fund screener and Lipper global dataset.

Assessing Market Risk

I am currently reading “A Crash Course on Crises: Macroeconomic Concepts for Run-Ups, Collapses, and Recoveries” by Princeton University economics professor Markus K. Brunnermeier and London School of Economics professor Ricardo Reis, which researches the interrelationship between financial markets and the economy during a crisis. They describe part of their audience to be “members of the informed public wanting to absorb some of the concepts that should be guiding both macroeconomic and financial policy.”

The book contains some wonderful insights into investing behavior, such as “Why don’t other, more sophisticated investors, lean against the bubble, preventing it from arising in the first place?” They continue, “These investors try to forecast how long the bubble will persist, which is governed by the trading behavior of the other (sophisticated) investors.” I have no illusions that I can predict the behavior of other sophisticated investors.

As described by Hyman Minsky, many crises are preceded by some type of innovation (such as artificial intelligence) followed by long periods of price increases, speculation, and leverage. These are followed by a period of instability and traders becoming risk-averse and de-leveraging. Stock market price-to-earnings ratios were around 18 before the 1929 stock market crash, peaked at 34 prior to the bursting of the dotcom bubble, hit 21 prior to the start of the financial crisis, and are now at an elevated 31.

There are usually “triggering events” that set off chain reactions between asset markets and financial markets that determine the severity of corrections and whether a macro-financial crisis results. At the National Association for Business Economics, Federal Reserve Chairman Jerome Powell said, “When COVID-19 struck in March 2020, the economy came to a near standstill and financial markets seized up, threatening to transform a public health crisis into a severe, prolonged economic downturn.” The stage is set for a correction, and there are plenty of potential “triggering events” such as a slowing economy, rising inflation, potential supply chain disruptions, and geopolitical risk.

The COVID and Great Normalization Full Cycles

Figure #2 represents the investing environment for the past six years. Fiscal and monetary stimulus contained the economic fallout from the COVID bear market lasting from January 2020 through March of that year, but Personal Consumption Price inflation rose from a half percent following the COVID bear market to nearly seven percent by January 2022. Charles Boccadoro described The Great Normalization (TGN) in which interest rates normalized to higher rates, hurting bond performance. The TGN bear market lasted from January 2022 to September of that year. By December 2023, the price-to-earnings ratio had crossed the high valuation level of $25 per dollar of earnings. The debasement trade is partly the result of investors and global central banks buying gold and the increased acceptance of cryptocurrency. I believe that the dollar will weaken but not be replaced as the global reserve currency, and the debasement trade is overbought.

Figure #2: The COVID and Great Normalization Full Cycles

Source: Author Using MFO Premium fund screener and Lipper global dataset.

The full COVID Cycle was from January 2020 to December 2021 and includes the COVID bear market and inflation. I expect cycles of bear markets and inflation to be more frequent in the coming decade than in the decade following the financial crisis. Rates are high, so “The Great Normalization” of rising rates is unlikely to occur to such extremes for many years. Finally, valuations are currently high and more likely to fall than rise either over time or in a correction with a “triggering event”.

Portfolio Results

I set up my Excel optimizer for both the Conservative and Moderate portfolios to maximize the Martin Ratio for the January 2020 to December 2021 period by changing allocations to 36 funds with constraints that I wanted to have drawdowns of less than nine percent for both the COVID and TGN bear markets. Maximum allocations were set for Alternative, Bond, Equity, and Mixed Asset fund types to ensure diversification. The Conservative portfolio has additional constraints of having yields at least 4% with less than 13% allocated to lower quality “junk bonds”.

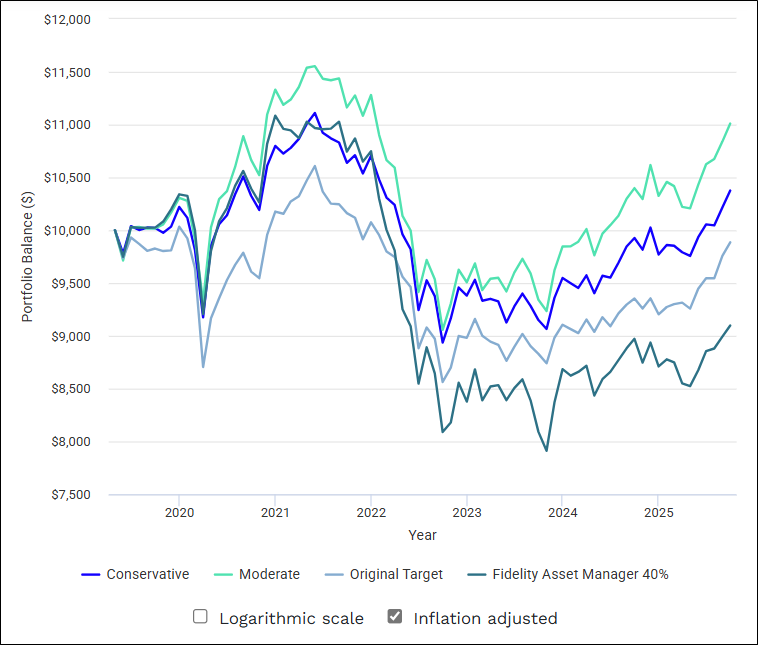

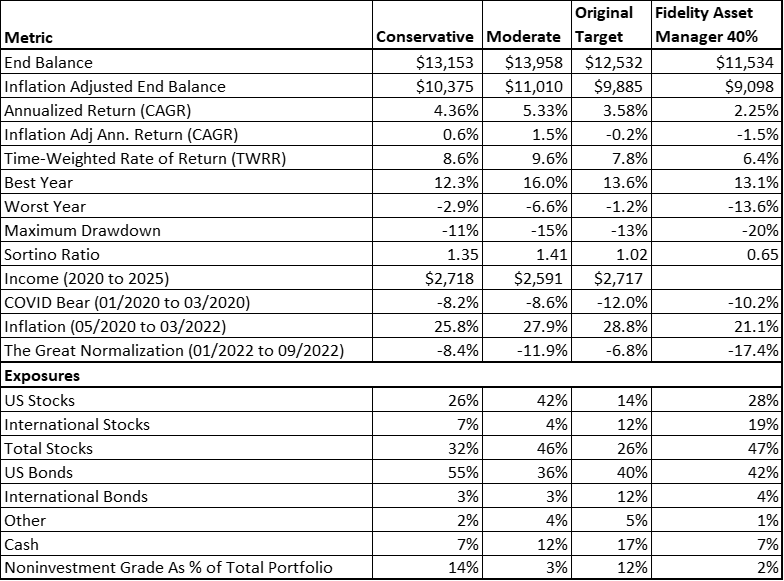

Figure #3 contains the inflation-adjusted results from Portfolio Visualizer assuming 4% annual withdrawals for the Conservative, Moderate, and Original Target Portfolio compared to the Fidelity Asset Manager 40% (FFANX), which is a good global mixed asset fund. The link is provided here. The Conservative and Moderate portfolios had similar returns through 2023, with the Moderate portfolio having higher volatility. Both beat inflation over the six years after adjusting for withdrawals. During the period of rising valuations and the debasement trade, the Moderate Portfolio has outperformed. Both outperformed the Original Target Portfolio from my last article because of a wider selection of funds under consideration, improvements in methodology, and an increase in the maximum allocation for a fund from 10% to 15%. All three outperformed the 40/60 baseline fund, which was negatively impacted during the rising rates period.

Figure #3: Conservative and Moderate Portfolio Growth – Six Years

Source: Author Using Portfolio Visualizer

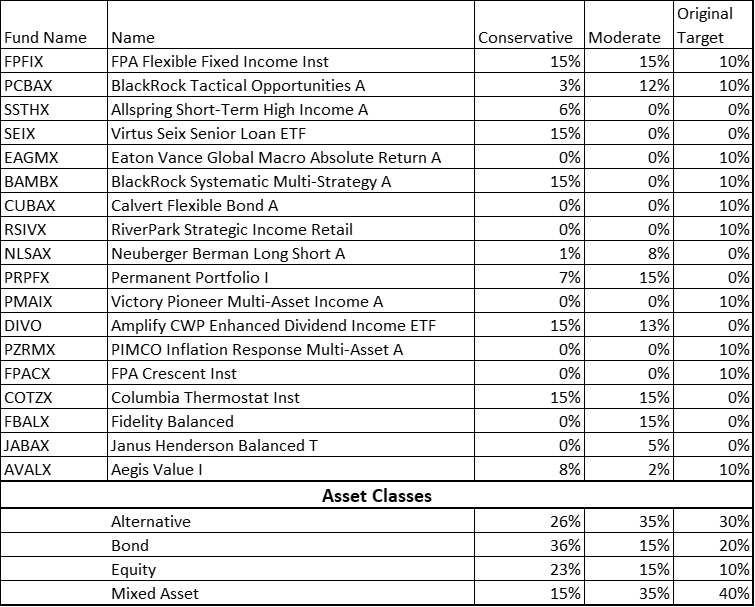

Table #2 contains the resulting allocations with the funds sorted from the lowest Ulcer Ratio over the past six years to the highest. I own shares in FPFIX/FFIRX, PCBAX, PMAIX, PZRMX, and AVALX. It will take a couple of years to fill out the rest of the portfolio, depending upon cash flows, and I will lean towards the less risky funds next.

Table #2: Portfolio Allocations

Source: Author Using MFO Premium fund screener and Lipper global dataset.

Table #3 contains the portfolio metrics for the period May 2019 to September 2025 from Portfolio Visualizer. Annualized returns are after withdrawals, while Time-Weighted Rate of Return reflects investment performance.

Table #3: Portfolio Performance

Source: Author Using Portfolio Visualizer

Fund Assessment

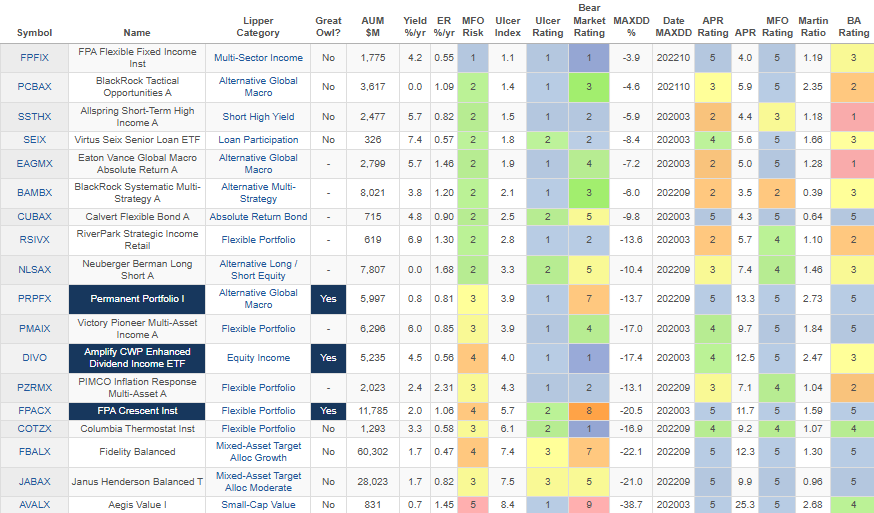

Table #4 contains the metrics and ratings from MFO for the funds for the past six years. They are sorted from the lowest Ulcer Index, which measures the depth and duration of drawdowns from the lowest to the highest. MFO Risk is based on the Ulcer Index comparing all funds, while the Ulcer Rating is for funds within the same category peers. Martin Ratio is the risk-free return divided by the Ulcer Index. The MFO Rating is based on the Martin Ratio for funds within the same Lipper Category. The Batting Average Rating (BA) is based on the percentage of the months that a fund beat its peers. One takeaway is that some of the funds outperformed during down markets but lagged peers overall.

Table #4: Fund Metrix – Six Years

Source: Author Using MFO Premium fund screener and Lipper global dataset.

Optimization depends on having funds with low correlations to each other. Notice that some funds had their maximum drawdowns during the COVID (2020) bear market, and some had them during the Great Normalization (2022) bear market.

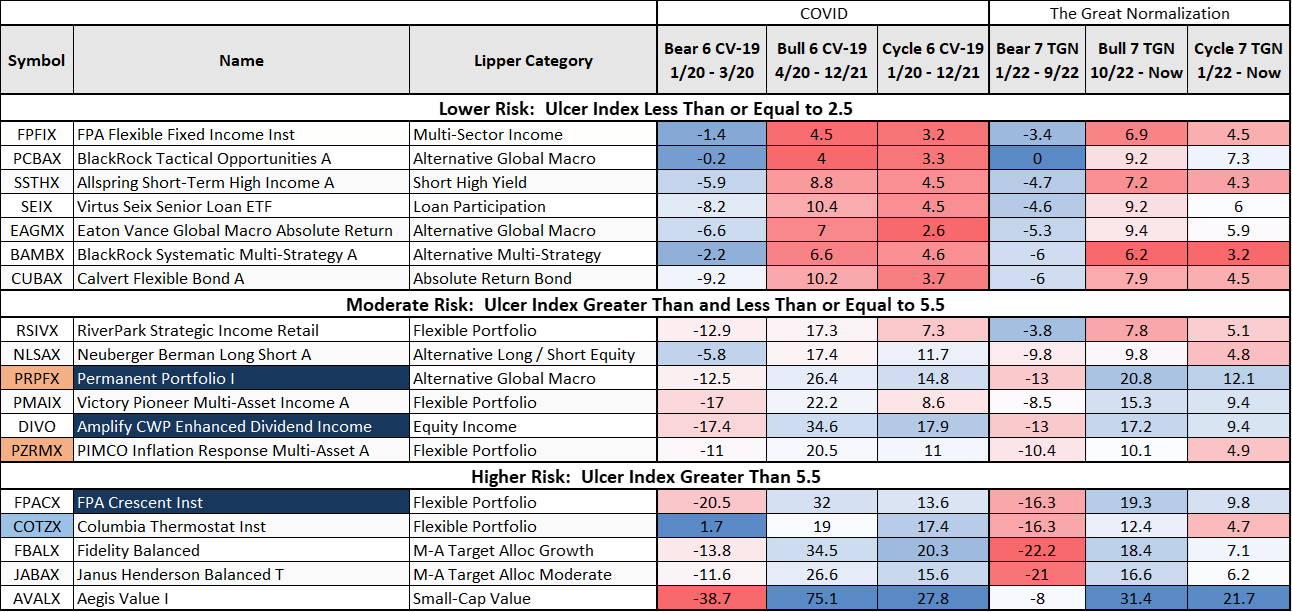

Table #5 shows how the funds performed in each of the bear markets and the bull markets. The lower-risk funds provide some safety during downturns, while the riskier funds provide growth potential. Blue shaded cells indicate the best performers, and red are the worst performers.

Table #5: Fund Performance During COVID and Great Normalization Cycles

Source: Author Using MFO Premium fund screener and Lipper global dataset.

Fund Spotlight – COTZX, PRPFX, PZRMX

Columbia Thermostat (COTZX, CTFAX)

Columbia Thermostat bases its stock to bond allocation on valuations. During the financial crisis, the strategy was to invest in all stocks or bonds, and it did not perform well. It has improved its strategy to have a range of allocations depending on price levels and performed well during the COVID bear market. The Fact Sheet indicates that the fund is currently 70% invested in fixed income and 30% invested in equity. It contains the allocation to stocks by the S&P 500 level.

BlackRock Tactical Opportunities (PBAIX, PCBAX)

BlackRock Tactical Opportunities (PBAIX, PCBAX) is an Alternative Global Macro fund that has performed well since the 2008 financial crisis, but during the financial crisis fell nearly 27% in 2008 and returned 26% in 2009. I own shares in PCBAX, but limit allocations to alternatives because they use derivatives, which can be less predictable during a crisis. Eaton Vance Global Macro Absolute Return (EAGMX) is another good Alternative Global Macro fund that had a maximum drawdown of 7% during the financial crisis. I included it in the original target portfolio from last month.

Comparison of Permanent Portfolio versus PIMCO Inflation Response Multi-Asset

The Permanent Portfolio (PRPFX) is based on the concepts developed by Harry Browne in the 1980s to provide steady, long-term growth with low volatility without trying to time the market. The fund managers describe Permanent Portfolio (PRPFX) as, “Designed as a core portfolio holding, Permanent Portfolio seeks to preserve and increase the purchasing power value of each shareholder’s account over the long-term, regardless of current or future market conditions, through strategic investments in a broad array of different asset classes.” It invests fixed percentages of its net assets in dollar assets (35%), gold (20%), aggressive growth stocks (15%), real estate and natural resource stocks (15%), Swiss Franc assets (10%), and silver (5%).

The PIMCO Inflation Response Multi-Asset (PZRMX) is described by the fund managers as “By investing in a blend of inflation-related asset classes, the fund seeks to help preserve and grow purchasing power, enhance portfolio diversification, and guard against market shocks across varying inflation environments.” It currently has a composition of Inflation Linked Bonds 68%), Commodities (22%), Currencies (15%), REITS (10%), and Precious Metals (10%). I own shares in PZRMX.

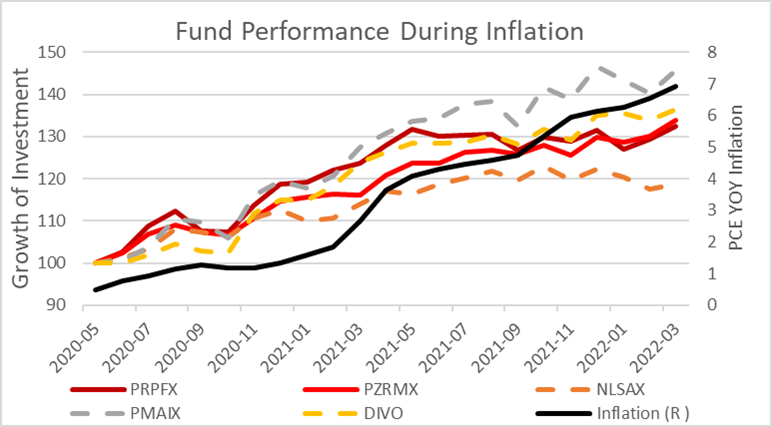

Figure #4 contains some of the funds that did well during 2020 to 2022 with high inflation. These are mostly in the Flexible Portfolio Lipper Category plus DIVO in equity income, Permanent Portfolio (PRPFX, maroon line) in the Alternative Global Macro category, and the PIMCO Inflation Response Multi-Asset (PZRMX, red line) in the Flexible Portfolio Category. During the period in between the bear markets, the S&P 500 rose 89% while core bonds rose a paltry 2.5%.

Figure #4: Fund Performance During Inflation (2020 – 2022)

Source: Author Using MFO Premium fund screener and Lipper global dataset and St. Louis Federal Reserve FRED database.

From 2012 through 2019, Permanent Portfolio (PRPFX) and PIMCO Inflation Response Multi-Asset (PZRMX) had very similar performance. From 2019 through 2021, PRPFX outperformed PZRMX and greatly outperformed starting in 2023. I prefer owning PRPFX and PZRMX to directly owning gold because it is much more volatile.

Closing

Over the past year, I decreased my allocation to stock from 65% to 50% which is a small decrease in risk. Rebalancing during high market valuations and downturns is a modest way of “buying low and selling high”. I believe that risk risk-adjusted performance of bonds to be greater than equities for the next few years. Using the bucket approach to match risk assets with spending needs and using bond ladders does more to reduce portfolio risk than lowering the allocation to stocks.

As a qualifier, I use financial advisors to manage the majority of my portfolio using a traditional, globally diversified 60/40 portfolio. I am developing this “Conservative Portfolio” strategy for a subset of the portfolio that I manage in addition to traditional bond funds and bond ladders to have liquidity available in any market condition, and with some growth potential.