Investing is always an uncertain project, generally undertaken in uncertain times, building with uncertain tools. It’s great if you own shares in Xanax’s parent, Pfizer, but frequently miserable otherwise.

Three factors make the current market a source of epic uncertainty: valuations are historically high, concentration is historically high, and safeguards are historically weak. Let’s agree that by “historically” we mean something like “since modern civilization nearly ended withthe Great Depression,” so about 100 years.

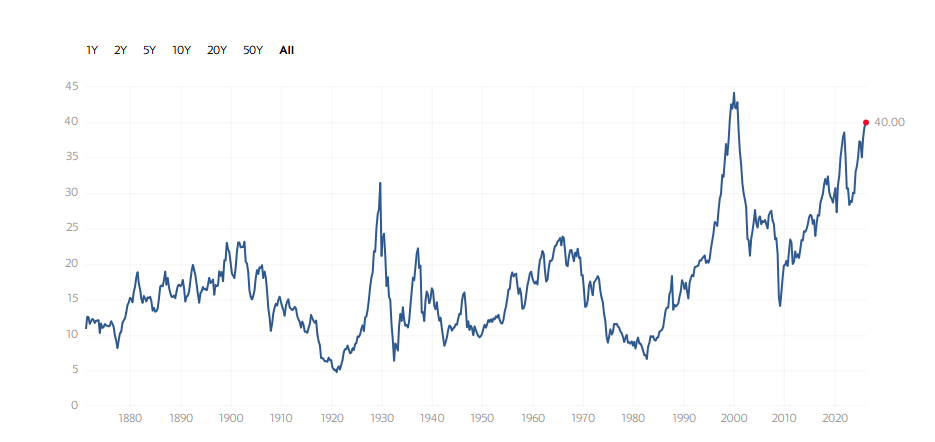

Valuations are historically high.

The Shiller CAPE P/E attempts to reduce noise in the earnings data, which can easily create transient false valuation signals, by looking at average inflation-adjusted earnings from the previous 10 years rather than, say, the previous three months. So the current Shiller CAPE translates to “assuming the earnings over the past 10 years are pretty representative of the economy today, how much are you paying for each dollar of earnings?”

Short version: a lot. Currently, broad market investors are paying $40 to buy $1 in earnings, the second-highest price for stocks in 150 years.

Source: Shiller PE Ratio, February 2026, per multipl.com.

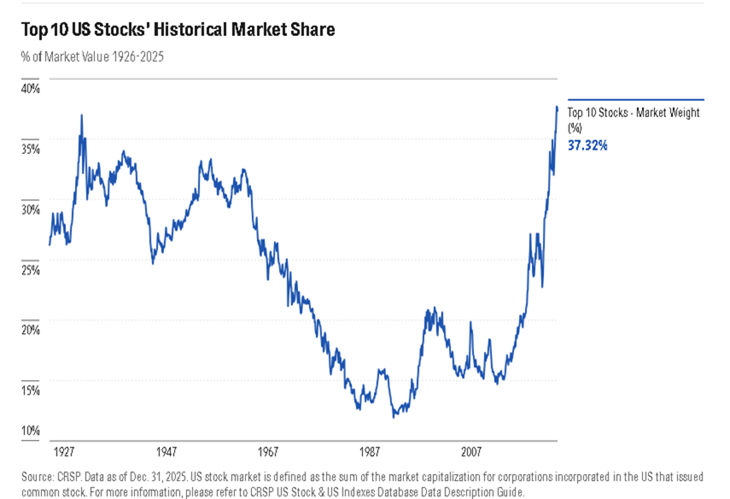

Stock market concentration is historically high.

Morningstar’s Dan Lefkovitz notes that “Stock Market Concentration Has Surpassed Its 1930s” (2/27/2026). That’s true by at least two measures.

First, the 10 largest US stocks comprise 37% of the total value of the market, the highest weight in history.

Source: Morningstar.com

Second, sector concentration has also spiked. The tech sector is 34% of the S&P 500, higher than it was during the bubble years of the 1990s. The second largest sector, financials (12%), carries barely one-third of the heft.

Mr. Lefkovitz reports on both sides of Morningstar’s research on the question. One side: “Concentration can be great for returns when market leaders are rallying” (Bold Portfolios: Are They Worth Their Risks?, a 2026 Morningstar UK report on concentrated funds, not concentrated markets). But, he notes, “there’s a flip side. ‘Even if concentration doesn’t guarantee a downturn, it erodes diversification benefits and makes markets more vulnerable to sentiment reversals,’ according to the Morningstar Outlook” (“Stock Market Concentration Has Surpassed Its 1930s,” 2/27/2026).

Investor safeguards are historically weak

U.S. investors today face not just historic valuations and concentration, but historically weak protection: the instruments are fuzzier, the guardrails lower, and the payoff to bad behavior higher. The federal statistical system has been hollowed out by budget and staffing cuts, yielding larger revisions and patchier coverage in core data like jobs and inflation, so both the Fed and markets are “driving through fog.” At the same time, federal financial enforcement, especially at the SEC, has retreated from post‑crisis norms in both case counts and penalties, while fraud surveys and complaint data show rising incidence and sharply higher realized losses. In practice, more of the burden falls on individual investors to detect risk that used to be constrained by stronger data and enforcement. That doesn’t dictate where markets go next, but it does make a clear‑eyed, portfolio‑by‑portfolio review less a luxury and more a basic act of self‑defense.

Converting awareness into motivation for an insulated portfolio

An insulated portfolio isn’t risk-free, but it’s conscious of exceptional risks. In the normal course of events, an investor knows how many high-beta funds or ETFs they hold. In the abnormal course of events, an additional layer of analysis might help.

We used the tools at MFO Premium to look carefully for hidden risks in my portfolio. That took place in three steps.

First, we looked at our funds’ intercorrelations. This is a six-year analysis, since that’s the age of the youngest fund in the portfolio. A correlation of 1.0 means two funds move in perfect lockstep; 0.0 means they move in perfect independence. For my purposes, correlations of about .80 warrant attention as potentially too high, and correlations below 0.5 signal reassuring independence. Negative correlations signal that one fund tends to rise when the other one falls.

Six-year fund correlations, through January 2026

| BAFWX | SIGIX | FPACX | GPMCX | PVCMX | RPHIX | SWVXX | RSIIX | LCORX | SIVLX | |

| Brown Adv Sust Gr | 1.0 | .38 | .73 | .61 | .27 | .68 | .24 | .60 | .66 | .25 |

| Seafarer G&I | 1.0 | .67 | .71 | .63 | .11 | -.32 | .29 | .58 | .91 | |

| FPA Crescent | 1.0 | .75 | .61 | .31 | -.02 | .66 | .85 | .61 | ||

| Grandeur Global Micro | 1.0 | .66 | .45 | .06 | .51 | .72 | .61 | |||

| Palm Valley | 1.0 | .27 | .06 | .54 | .62 | .50 | ||||

| RiverPark Short Term | 1.0 | .44 | .45 | .27 | .01 | |||||

| Schwab MM | 1.0 | .22 | .04 | -.40 | ||||||

| RiverPark Strategic | 1.0 | .55 | .31 | |||||||

| Leuthold Core | 1.0 | .48 | ||||||||

| Seafarer Value | 1.0 |

Good news: there is only one high correlation in the entire matrix. FPA Crescent and Leuthold Core, both flexible portfolio funds, have an 85% correlation. No one else is above 80. Twenty-one of the correlations are at or below 50%. What that means is that all of the funds in the portfolio are making distinct contributions; no two funds are bringing the same set of strengths and weaknesses to the table.

Second, we looked at our funds’ correlation with both the S&P 500, a surrogate for an overpriced stock market, and an ETF that tracks “the Magnificent 7” stocks, a surrogate for an overconcentrated market.

| Correlation with MAG 7 stocks | Correlation with S&P 500 | Correlation with cash | |

| Brown Advisory Sustain Growth | 0.85 | 0.89 | 0.24 |

| S&P 500 | 0.79 | 1.00 | 0.09 |

| FPA Crescent | 0.61 | 0.56 | -0.02 |

| Leuthold Core Investment | 0.50 | 0.84 | 0.04 |

| RiverPark Strategic Income | 0.47 | 0.66 | 0.22 |

| RiverPark Short Term High Yield | 0.45 | 0.37 | 0.44 |

| Grandeur Peak Global Microcap | 0.42 | 0.67 | 0.06 |

| Seafarer Overseas G&I | 0.29 | 0.55 | -0.32 |

| Palm Valley Capital | 0.23 | 0.46 | 0.06 |

| Seafarer Overseas Value | 0.19 | 0.43 | -0.40 |

| Schwab Prime Adv Money | 0.11 | 0.09 | 1.00 |

More good news: only one fund shows strong correlations with both the Magnificent 7 and the broader market. That’s Brown Advisory Sustainable Growth, which, given its focus on US growth companies, doesn’t come as a surprise. Leuthold Core has an abnormal correlation to the stock market, higher than its typical 60% stock exposure would imply, but a low correlation with the Mag 7. That suggests that Leuthold has other sorts of securities – high yield bonds, as an example – which respond to the same pressures that drive the stock market.

Takeaway: I wanted to avoid being hostage to the tippiest part of the US market, and have pretty much succeeded.

Third, we looked at whether the funds provided consistent protection against the market’s downside. We looked at their returns, returns in comparison to peers, then their worst decline, what percentage of the S&P’s downside they captured, and how closely they follow their peer groups.

Six-year fund performance comparison, through January 2026

|

|

APR |

APR vs peers |

Maximum drawdown |

Downside capture |

Correlation to peers |

|

Schwab Prime Adv Money |

2.7 |

0.1 |

0.0 |

-4.7 |

1.0 |

|

RiverPark Short Term High Yield |

3.8 |

-0.9 |

-1.1 |

-3.7 |

.57 |

|

Palm Valley Capital |

7.7 |

-1.0 |

-2.8 |

6 |

.26 |

|

RiverPark Strategic income |

5.9 |

-1.6 |

-13.6 |

11 |

.41 |

|

Leuthold Core Investment |

8.8 |

1.4 |

-12.9 |

57 |

79 |

|

Seafarer Overseas Value |

12.1 |

3.3 |

-23.0 |

61 |

.79 |

|

FPA Crescent |

11.8 |

4.3 |

-20.1 |

69 |

.89 |

|

Seafarer Overseas G&I |

9.7 |

0.9 |

-27.8 |

81 |

.88 |

|

Grandeur Peak Global Microcap |

8.2 |

-1.9 |

-42.5 |

104 |

.85 |

|

Brown Advisory Sustain Growth |

12.5 |

-0.4 |

-32.9 |

113 |

.90 |

The third table tells the story of what happens when markets turn ugly. The money market and short-term high yield funds did exactly what they’re supposed to: they posted modest positive returns while capturing none of the market’s downside. RiverPark Short Term High Yield actually rose when stocks fell. Palm Valley Capital and RiverPark Strategic Income offered meaningful returns (7.7% and 5.9%, respectively) while capturing only 6% and 11% of market downturns. These four funds, representing 35% of my portfolio, provide genuine ballast. At the other extreme, Brown Advisory and Grandeur Peak amplified market losses, capturing 113% and 104% of downside, respectively, without delivering compensating returns. Brown trailed its peers despite higher risk, while Grandeur trailed by nearly 2% annually with a maximum drawdown exceeding 40%. The middle tier, FPA Crescent, Leuthold Core, and both Seafarer funds, captured between 57% and 81% of market downside while posting solid absolute returns that handily beat their peers. These are equity-focused funds behaving as equity funds should: participating in markets while exercising some defensive discipline.

Bottom line

Three exceptional risks define today’s market: historically high valuations, historically high concentration, and historically weak investor safeguards. An insulated portfolio doesn’t eliminate those risks, but it avoids amplifying them through hidden correlations and false diversification.

The analysis reveals both success and work ahead. I’ve avoided being hostage to either the Magnificent 7 specifically or the broader overpriced market generally. Only one fund shows high correlation to both. My funds don’t duplicate each other’s strengths and weaknesses. And more than a third of the portfolio provides genuine downside protection rather than just different flavors of equity risk.

But two funds, Brown Advisory Sustainable Growth and Grandeur Peak Global Microcap, are failing their assigned roles. Brown amplifies market downside (113% capture) despite being positioned as a quality growth manager. Grandeur captures 104% of downside while trailing peers by 2% annually, with no evidence yet that the founder’s return has catalyzed improvement. Both are on the chopping block, with Aegis Value and Grandeur Peak Global Contrarian on the short-list of likely successors.

An insulated portfolio isn’t static. It requires periodic examination not just of what you own, but of whether those holdings still justify their place at your table. In times of exceptional risk, that examination shifts from an annual ritual to an urgent necessity.