I propose that those of us over sixty have been blessed with the experience of living through multiple drastic and dramatic pullbacks, which have been real-life stress tests on what we actually feel and do in a financial crisis. We have personal experience to draw on to pre-plan for the next inevitable drop.

I grew up listening to the stories of the Great Depression and the Dust Bowl from those who lived through them. I graduated from high school during the stagflation of the 1970’s when unemployment was high, and inflation shrank the purchasing power of the dollar. The bursting of the Dotcom Bubble taught us that stocks had not reached a permanent plateau of higher valuations. People shifted focus from the technology bubble in stocks to an emerging bubble in housing, and the Great Financial Crisis resulted from an incorrect assessment of the risk of the financial innovation of collateralized debt obligations for subprime loans.

Today, the S&P 500 is up eighty percent during the past three years, and many analysts expect it to gain another 10% this year. The price-to-earnings ratio is higher than at the start of ninety-four of the years since 1929. Margin debt is again at historically high levels. High deficits and national debt pose new risks not seen since World War II.

Hope is not a good strategy. In today’s environment, I hope for the best and prepare for the worst. I have determined that my Core TIRA sub-portfolio would benefit in the long-term from a good mixed-asset growth fund. I believe that the current risk-to-reward ratio favors cash. I have started building a small cash reserve for better entry points.

Investing in U.S. Financial History

I am currently reading Investing in U.S. Financial History – Understanding the Past to Forecast the Future (2024) by Mark J. Higgins:

The formation of asset bubbles requires a large percentage of people to believe that a bubble cannot exist. Usually, widespread acceptance of such narratives depends on heavy promotion by market experts and members of the media. Once the narrative is accepted by a large swath of investors, a bubble is likely to follow…

Asset bubbles often repeat because investors’ collective memory does not extend far enough back in time to see the repetition.

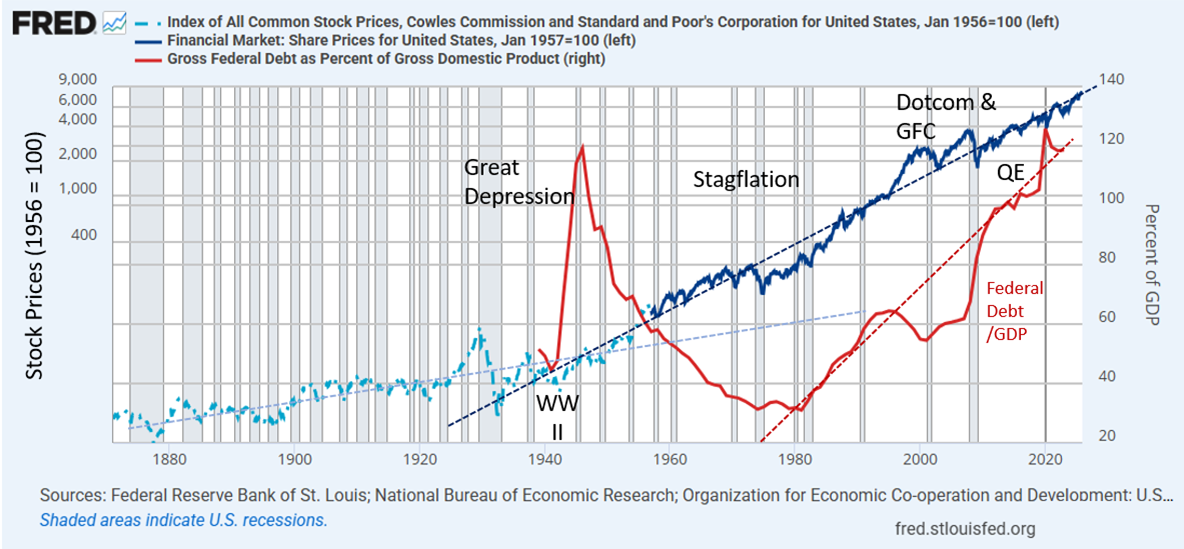

The book is enlightening about the financial instability during the preliminary evolution to the current financial system. Recessions, depressions, and bank failures were more common. Figure #1 is my attempt to capture the impact of financial evolution since the Civil War on the stock markets (log scale). The changes made during the Great Depression (1930s) created a stronger financial foundation, and recessions became less frequent. The end of World War II marked a major inflection point for stocks to rise at a faster rate. The taming of inflation in 1982, followed by the end of the Cold War, has extended this period of prosperity. I have concerns that policy changes being implemented now will result in unanticipated problems for decades to come.

The fact that the National Banking Acts [1864-1865] were both a present solution and source of future problems is not a unique phenomenon in financial history. Many financial innovations follow the same pattern. Sometimes unanticipated problems emerge within a few years, but usually they remain hidden for decades…

– Mark J. Higgins

Figure #1: Recessions and Stock Prices Since 1871

Source: Author using National Bureau of Economic Research, Cowles Commission, and Standard and Poor’s Corporation for the United States, retrieved from the Federal Reserve Bank of St. Louis (FRED)

The stock prices are shown in nominal values, but inflation and the devaluation of the dollar have played a role. The Gold Reserve Act of 1934 devalued the dollar, and President Richard Nixon ended international convertibility of the dollar to gold in 1971. Some of the growth in stock market prices was financed by rising debt, which now poses challenges to future growth.

The Power of Perspective

The Federal Reserve and Treasury may succeed in lowering short- and intermediate-term interest rates to stimulate economic growth and finance the growing national debt. The coming decade is likely to see inflation running a little hotter. Kenneth Rogoff stated in Our Dollar, Your Problem (2025) that he expects “a sustained period of global financial volatility marked by higher average real interest rates and inflation and more frequent bouts of debt and financial crises.” Ray Dalio wrote in Principles for Dealing with the Changing World Order – Why Nations Succeed and Fail (2021) that “The goal of printing money is to reduce debt burdens, so the most important thing for currencies to devalue against is debt (i.e., increase the amount of money relative to the amount of debt, to make it easier for debtors to repay).” I agree with these narratives.

There is a high risk in planning retirement based on the average performance of the stock market over the past one hundred years. Retirement planning involves settling on a realistic expectation for likely drawdowns during severe bear markets.

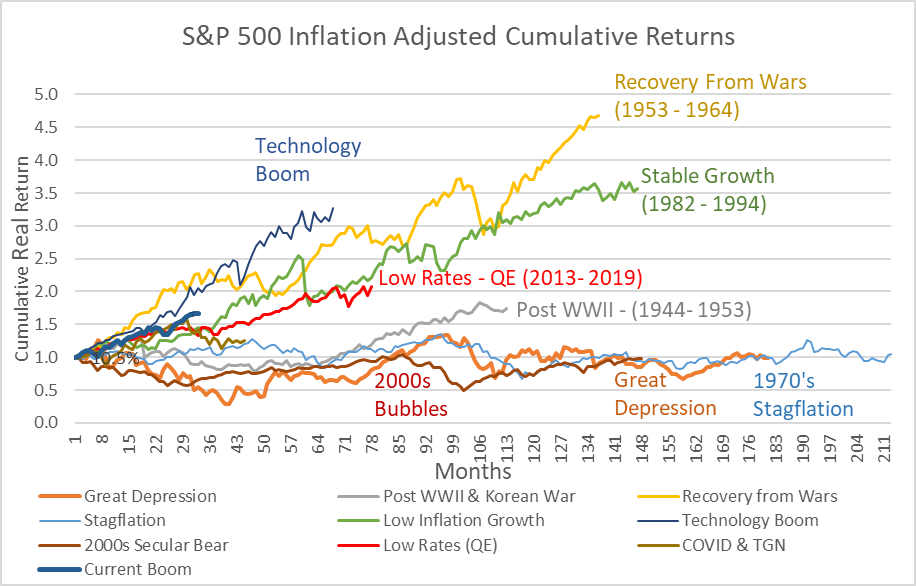

For this article, I estimated the inflation-adjusted returns of the S&P 500 for ten periods since 1929. Three periods covering 45 years saw no positive returns. Five periods covering 38 years produced the majority of the real returns since 1929. Sixty percent of these years (24 years) with high gains came during two time periods: 1) Peace time recovery period following the end of World War II and the Korean War, and 2) Stable Economic Growth following the stagflation of the 1970s and the end of the Cold War. The remaining periods (15 years) of high real stock market returns are during the periods of: 1) run-up to the Dotcom Bubble with high valuations, 2) low interest rates following the Great Financial Crisis when interest rates were suppressed, and 3) the past three years of rising equity valuations.

Figure #2 shows the inflation-adjusted cumulative returns. I don’t believe that the current three-year bull market (heavy blue line) has the foundation to extend more than a few years at most. Secular bull markets are rare, and cyclical bull markets last only three to five years.

Figure #2: S&P 500 Inflation-Adjusted Cumulative Returns

Source: Author Using MFO Premium fund screener and Lipper global dataset; St. Louis Federal Reserve (FRED) database

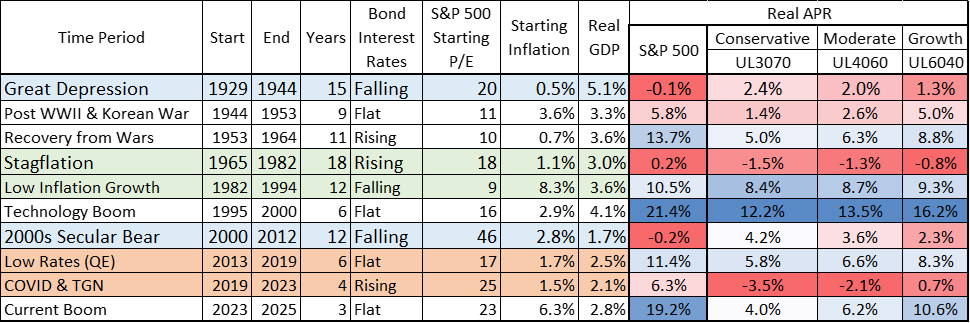

The information is shown in Table #1 along with some factors that influence stock market returns. Boom periods create excesses, which are followed by busts. High stock market returns are influenced by many factors besides economic growth, including population growth, valuations, wars, stability, uncertainty, geopolitical risk, globalization, technology, inflation, interest rates, and pandemics, among others. The blue-shaded periods covering 27 years (Great Depression & Bursting of Dotcom followed by the Great Financial Crisis) are when mixed-asset portfolios outperformed an all-equity portfolio. The two periods shaded green, covering 30 years (1970s Stagflation followed by low inflation with falling rates), are when mixed-asset portfolios performed about as well as an all-equity portfolio.

The two periods shaded burnt orange, covering 10 years (Low interest rates and rising interest rates), are when moderate mixed-asset funds underperformed the all-equity portfolio by five to eight percentage points. There were 27 years when a 40/60 portfolio outperformed the S&P 500 and 60/40 portfolio.

Table #1: S&P 500 Inflation-Adjusted Cumulative Returns

Source: Author Using MFO Premium fund screener and Lipper global dataset; St. Louis Federal Reserve (FRED) database

Some of the drivers of historical economic growth will have less of an impact in the future. The population of the U.S. has more than tripled since 1920, and growth has slowed. Gross federal debt as a percentage of gross domestic product has increased from 49% in 1940 to 119% today and is still rising. Starting equity valuations today (30) are higher than any of the ten periods and a headwind to stocks, while high starting yields are a tailwind to bonds performing well. Uncertainty does not favor stable economic or stock market growth.

The Advantages and Disadvantages of Cash

Those who have been fortunate to save and accumulate now have a very powerful buffer against panic – a cushion even with serious losses to ride it out. With conservative funds yielding 3.5% to 4%, cash is not trash. It provides liquidity for withdrawals and emergencies. Bear markets are typically less than one year, but the time to recover may take several more years. Keeping enough cash and safe investments to cover these two-to-five-year periods allows you ride out most bear markets.

The Tax Man Cometh!

I began studying financial planning two decades before retiring, while there was uncertainty about job security. It was a valuable lesson, especially about taxes. I switched contributions to Roth IRAs to reduce taxes during retirement. I was still overweight in Traditional IRAs, and performed Roth Conversions after retirement when my income was lower. It did raise my Medicare income-related monthly adjustment amount (IRMAA), which I am lowering by taking steady withdrawals from Traditional IRAs.

For diligent savers wishing to reduce their tax liabilities in retirement, they may want to plan ROTH conversions from TIRAs during market drops. In hindsight, I should probably have made smaller ROTH conversions more frequently while still working. I would have paid higher taxes while working, but avoided higher IRMAA premiums now.

Fools Rush In Where Angels Fear To Tread

Fear of missing out (FOMO) when the market is unexpectedly soaring often leads to investors being overcommitted to stocks. Humans are hardwired with the tendency to fear losses more than host positive feelings over the same gains, and it pushes them to sell at the bottom. In retirement, we need to be cognizant of the sequence of return risk that poor market conditions can have on our savings.

To resist their psychological urges, informed investors can raise cash while markets are high with a plan to deploy into stocks during drawdowns, so market losses are investment opportunities. Let yourself make a 5% urgency readjustment in stock/bond balance as a pressure valve when you are overwhelmed by fear (analogous to an occasional rich dessert on a diet). Over the past year, I permanently lowered my overall stock-to-bond target from 65% to less than 50%, but it has been creeping back up. Meanwhile, core bond funds have made close to 7% for the past year.

Closing

I don’t believe that the current bull market has a strong foundation to extend into a secular bull market. Periods with stable economic growth and high equity valuations tend to result in lower long-term equity returns as uncertainty increases. When investors perceive higher economic uncertainty, they tend to seek safety, leading to lower valuations as demand for stocks fall. Long-term rates are influenced by expectations for inflation and economic growth.

After researching income and alternative funds for the past several months, I decided to err on the side of safety. As bonds mature, I am investing the proceeds into a new rung on my ten-year ladder or conservative income-producing funds already in my Core TIRA. I have started building a small cash reserve. I find the risk-to-reward favors cash, but I look forward to opportunities to invest in an income-producing mixed-asset growth fund during market downturns.

Hope is not a good strategy.

A special thanks goes to my long-time friend Dave in Spokane, Washington. We began discussing investment books two decades ago on our two-hour trips to the nearest Costco. I continue to bounce investing ideas off him, and he provides wonderful insights.