A friend of mine asked me to write “Perpetual Income for Dummies,” covering a simple portfolio for a conservative investor that generates steady income to cover withdrawals. The objectives of the “Perpetual Income for Dummies” Portfolio are: 1) income of $40,000 for a $1M portfolio in 2016 that rises with inflation, 2) average ten-year annual return of 7%, and 3) minimize the drawdowns during the COVID and TGN bear markets. The unique part of this study is to estimate the income by year as a constraint in a self-constructed optimizer using Excel Solver.

I compare this portfolio with the Vanguard Wellesley Income Fund (VWIAX) and a Morningstar Conservative Tax-Advantaged Bucket #2 Portfolio. Each of these has advantages as part of an overall portfolio, but are not intended to be standalone portfolios.

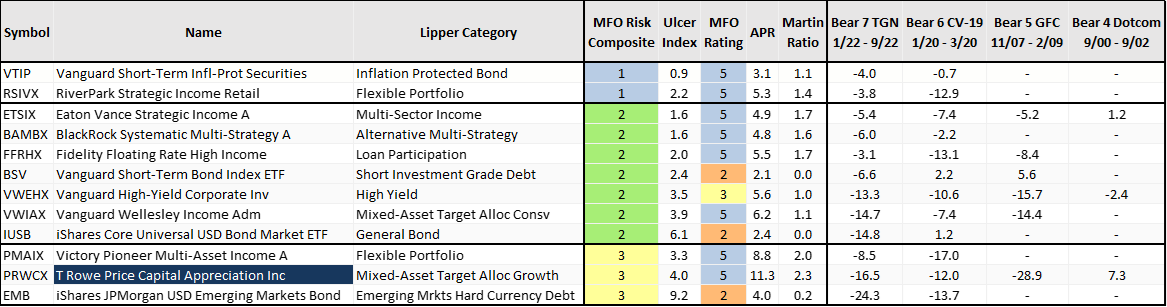

I have been researching alternative and income funds for the past several months, looking for funds that produce steady income across many environments. For this article, I evaluated eight conservative alternative funds that had average yields of 4.2% over the past ten years. I evaluated bond funds in eight different Lipper Categories that have returned at least 4% annualized over the past ten years. These alternative and income funds have produced annualized returns of 4% to 5% over the past ten years. Income-producing mixed-asset funds are used to boost returns and contribute to income.

Risk Income

I look for funds that have the flexibility to do reasonably well in both the low-interest rate environment of the 2010s and a more volatile inflation environment since the COVID pandemic. The funds have more consistent and/or higher yields than traditional bond funds with less risk than equities. Most of the funds in the following table are too risky for a conservative investor such as myself. My preferred category is “Multi-Sector Income” because it has the flexibility to invest in multiple sectors and tends to have lower drawdowns. Eaton Vance Strategic Income (ETSIX) is included in the “Perpetual Income for Dummies” Portfolio for its low MFO Risk (Conservative), Ulcer Index, risk-adjusted returns, and high yield, among other reasons.

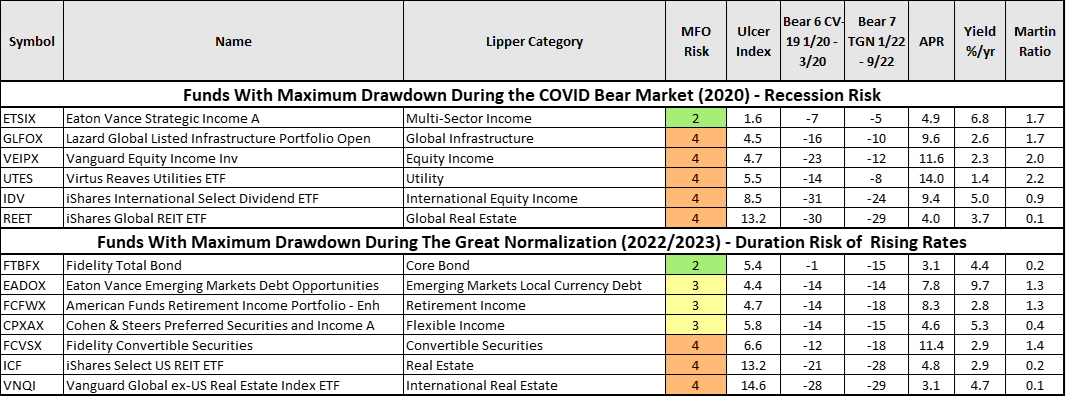

Table #1 contains examples of income-producing funds, including REITs, utilities, and equity income. Fidelity Total Bond (FTBFX) is a core bond fund shown as a baseline. The funds are divided based on whether their maximum drawdown occurred during the COVID Bear Market (2020), suggesting quality risk during a recession, or the Great Normalization (2022-2023), suggesting sensitivity to rising interest rates. They are sorted from lowest to highest risk. Most funds had moderate to high drawdowns in both periods. FTBFX performed well during the COVID bear market, but not the Great Normalization. For a long-term buy-and-hold portfolio, I want funds that have the flexibility to do reasonably well in both recessionary and inflationary environments.

Table #1: Risk Income – Ten Years

Source: Author Using MFO Premium fund screener and Lipper global dataset

Perpetual Withdrawal Rate

Here is a hat tip to YogiBearBull from the MFO Discussion Board. In the following table, I included the “Perpetual Withdrawal Rate” from Portfolio Visualizer. It is defined as, “… the percentage of portfolio balance that can be withdrawn at the end of each year while retaining the inflation-adjusted portfolio balance (percentage withdrawal). Perpetual withdrawal rate is specific to the time period and return path, so it is mostly useful as a relative comparison metric, not as an absolute value.”

In the companion article this month, “Hope Is Not a Good Strategy”, I cover why “there is high risk in planning retirement based on the average performance of the stock market over the past one hundred years.” In that article, I evaluate the inflation-adjusted stock performance for ten periods covering the past one hundred years. For more information on safe withdrawal rates, I refer you to the “PV – SWR, PWR (& SWRM)” thread posted by YogiBearBull on the MFO Discussion Board.

Overview

I used Portfolio Visualizer to analyze the three sub-portfolios. The link to Portfolio Visualizer is provided here. The results are very similar comparing the “Perpetual Income for Dummies” Portfolio to the Vanguard Wellesley Income (VWIAX) from 2016 through 2022. It outperforms VWIAX by quite a bit during the past three years, in large part because higher-yielding debt has performed better now that interest rates are higher. The “Morningstar Conservative Tax Advantage Bucket #2” Portfolio is all bonds for safe withdrawals covering the next three to ten years and has a lower income.

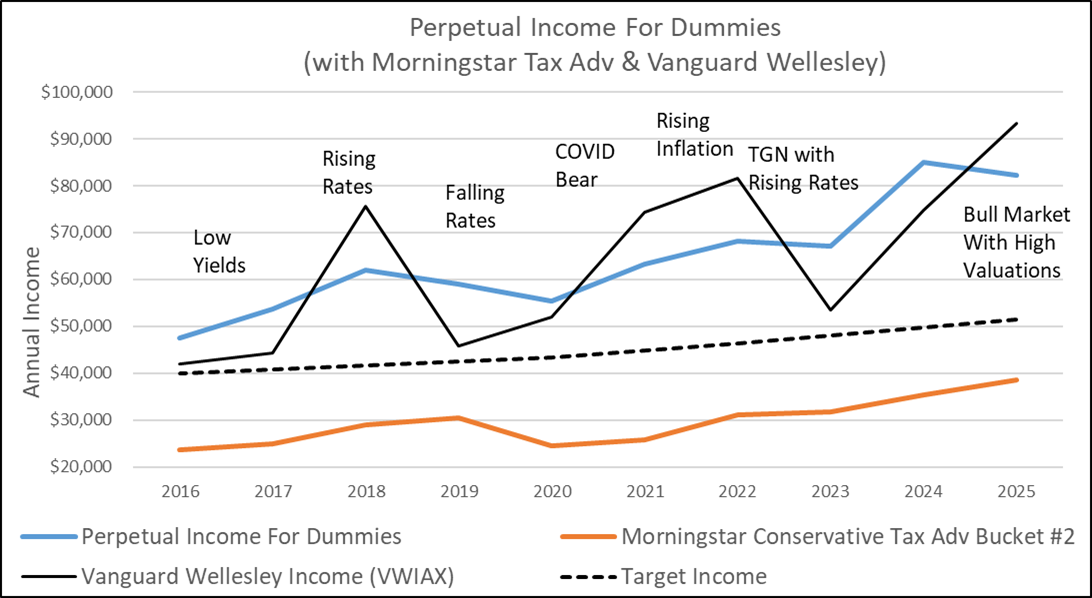

Let’s start with Figure #1, which shows the annual income of “Perpetual Income for Dummies” Portfolio (blue line) compared to the Vanguard Wellesley Income (VWIAX, solid black line), and the “Morningstar Conservative Tax Advantage Bucket #2” Portfolio (burnt orange line). The dashed black line is the annual income constraint that increases with inflation. The “Perpetual Income for Dummies” Portfolio achieved the objective of having a steady income. The variability in annual income for VWIAX is mostly the result of capital gains distributions.

Figure #1: Portfolio Income – Ten Years

Source: Author Using Portfolio Visualizer

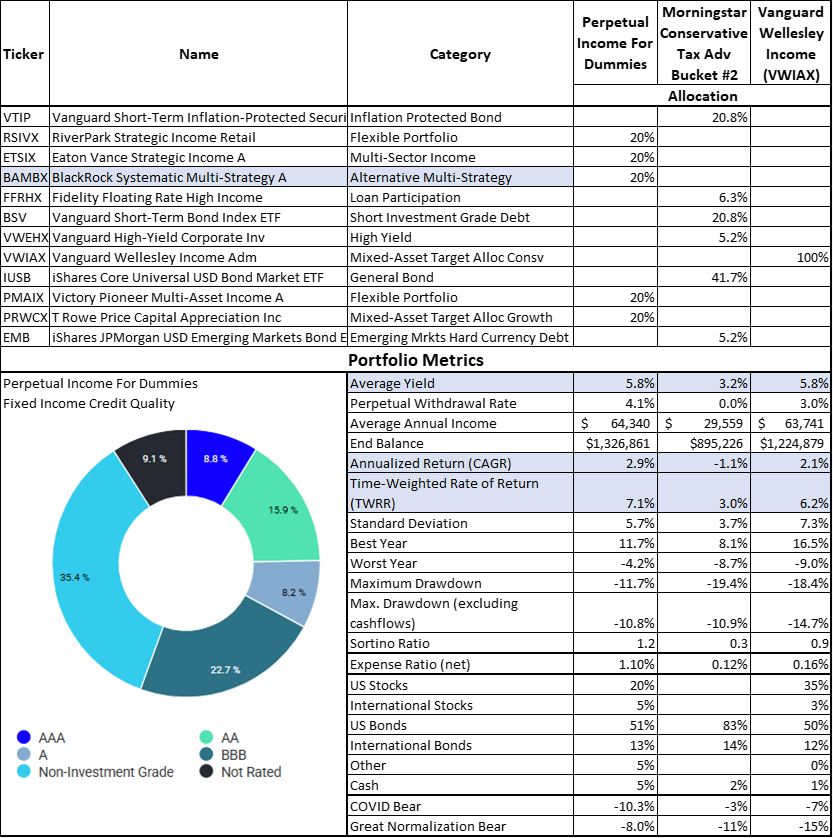

Table #2 compares the three portfolios for the past ten years. The assumptions include withdrawing 4% annually. The “Perpetual Income for Dummies” Portfolio has a higher return with lower drawdown than Vanguard Wellesley Income (VWIAX). It accomplishes this in part by having a lower allocation to stocks and a higher allocation to non-investment-grade debt. The funds are sorted by MFO Risk and Ulcer Index from the least risky to the highest. BlackRock Systematic Multi-Strategy (BAMBX) is an alternative fund.

The “Morningstar Conservative Tax Advantage Bucket #2” Portfolio is intended to be used for withdrawals when the stock market is low, and withdrawals taken from the Bucket #3 equity portfolio when the stock market is doing well. The intermediate Bucket is replenished from Bucket #3 when the stock market is high. The table assumes that all withdrawals come from the “Morningstar Conservative Tax Advantage Bucket #2” Portfolio. The overall portfolio strategy needs to be considered.

Table #2: Portfolio Performance with 4% Withdrawals – 10 Years

Source: Author Using Portfolio Visualizer

My optimizer selected the T Rowe Price Capital Appreciation Income Fund (PRWCX), which is currently closed to new investors. For this article, I evaluated eighteen mixed-asset funds out of the sixty-one that I track that had the potential to have high risk-adjusted returns with an emphasis on income. FPA Crescent (FPACX) and Vanguard Wellington (VWELX) had similar performance to PRWCX. I like and own Vanguard Global Wellington (VGWAX), but did not include it in this evaluation because its inception date is less than ten years.

Figure #2: Portfolio Performance with 4% Annual Withdrawals – 10 Years

Source: Author Using Portfolio Visualizer

I selected the funds in “Perpetual Income For Dummies” Portfolio primarily on their performance for the past ten years, but also considered their lifetime performance as shown in Table #3.

Table #3: Fund Performance – 10 Years

Source: Author Using MFO Premium fund screener and Lipper global dataset

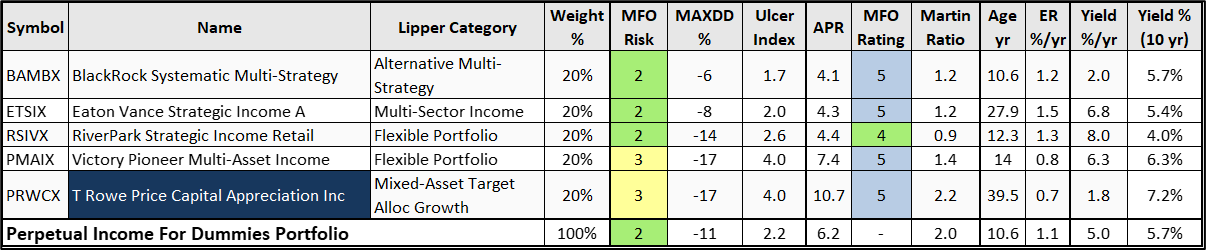

Perpetual Income for Dummies Portfolio

The objectives of the “Perpetual Income for Dummies” Portfolio are: 1) have income of $40,000 for a $1M portfolio in 2016 and increase for inflation, 2) have an average ten-year annual return of 7%, and 3) minimize the drawdowns during the COVID and TGN bear markets. It includes one multi-sector bond fund and one alternative multi-strategy fund, along with three mixed asset funds. I own shares in Victory Pioneer Multi-Asset Income (PMAIX) and two multi-sector income funds not included in the portfolio. The Lipper definitions are shown below for ETSIX and BAMBX.

Morgan Stanley Investment Management acquired Eaton Vance in 2021. ETSIX is available at Fidelity with no load or transaction fees. It is available at Vanguard with a load. I own two multi-sector income funds: PIMCO Income (PIMIX, PONAX) and FPA Flexible Fixed Income (FPFIX, FFIRX).

Eaton Vance Strategic Income (ETSIX): Multi-Sector Income Funds: Funds that seek current income by allocating assets among several different fixed income securities sectors (with no more than 65% in any one sector except for defensive purposes), including U.S. government and foreign governments, with a significant portion of assets in securities rated below investment-grade.

I own one alternative global macro fund, BlackRock Tactical Opportunities (PCBAX), in self-managed portfolios, but BlackRock Systematic Multi-Strategy (BAMBX) is probably a better selection for someone seeking income. I wrote BlackRock Systematic Multi-Strategy (BAMBX) vs BlackRock Tactical Opportunities (PCBAX) for the MFO September 2025 issue. The article compares them to Victory Pioneer Multi-Asset Income (PMAIX).

BlackRock Systematic Multi-Strategy (BAMBX), Alternative Multi-Strategy: Funds that, by prospectus language, seek total returns through the management of several different hedge-like strategies. These funds are typically quantitatively driven to measure the existing relationship between instruments and in some cases to identify positions in which the risk-adjusted spread between these instruments represents an opportunity for the investment manager.

Table #4 contains the funds in the “Perpetual Income for Dummies” Portfolio from the MFO Premium Portfolio Tool, with the average yield over the past ten years from this study. Notice that the 10-year yield often differs significantly from the 1-year yield. Some funds have yields that fluctuate with the interest rate cycle, and some with the stock market cycle. The largest differences are usually the result of capital gains distributions.

Table #4: “Perpetual Income for Dummies” Portfolio – 10.6 Years

Source: Author Using MFO Premium fund screener and Lipper global dataset

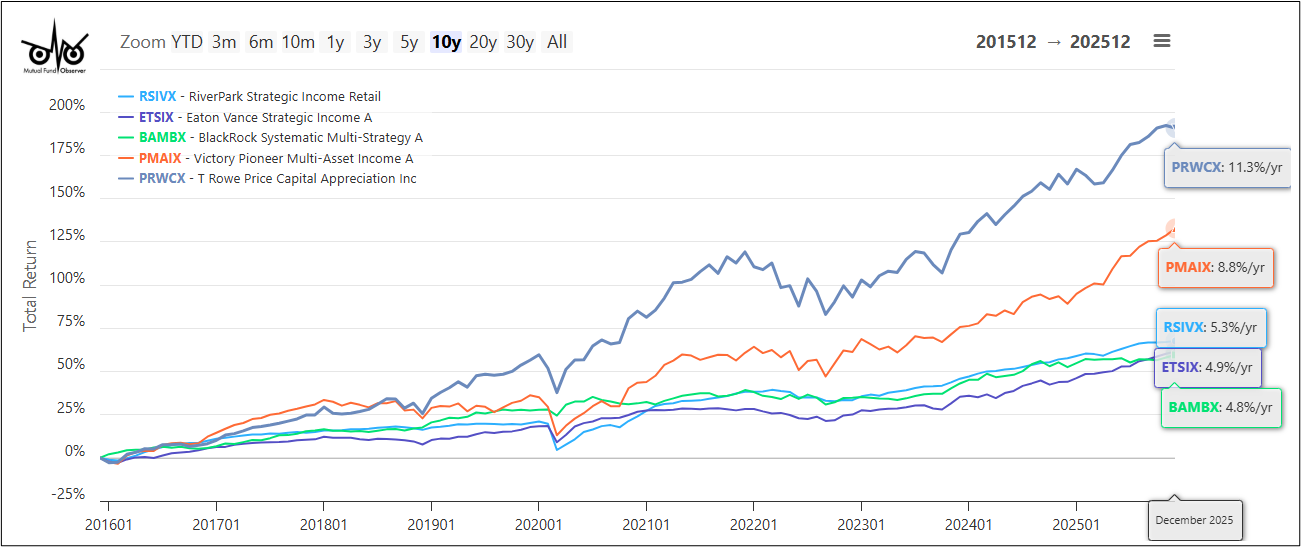

My intention is that the funds are buy-and-hold with occasional rebalancing. The funds have low correlations to each other, so that at least one fund should be doing relatively well in most market environments.

Figure #3: “Perpetual Income for Dummies” Fund Performance – 10 Years

Source: Author Using MFO Premium fund screener and Lipper global dataset

The “Perpetual Income for Dummies” Portfolio may be suitable for investors who are comfortable with alternative funds and investing in higher-risk debt. For those wanting to follow a more traditional approach, the other two portfolio options may be more suitable.

Vanguard Wellesley Income Fund (VWIAX)

I like the Vanguard Wellesley Income Fund (VWIAX), and it has been a core holding for years, but I switched to Vanguard Global Wellesley Income (VWYAX) because of its global exposure. VWIAX produces high income with a respectable total return. It sticks to debt-rated investment grade or higher.

Having one fund as part of a conservative TIRA is simple, and no rebalancing is required. The disadvantages are that yields can fluctuate, and you may have to sell in a down market if you require additional cash. Possible methods to overcome this are to use one or more bond funds and/or bond ladders that cover required minimum distributions if investment income falls short.

Morningstar Conservative Tax-Advantaged Bucket #2

Christine Benz wrote Tax-Sheltered Retirement-Bucket Portfolios for ETF Investors for Morningstar. I am a follower of her bucket approach and dividing an intermediate bucket into conservative and aggressive sub-portfolios. Her Bucket #2 that covers withdrawals for the next three to ten years is all bonds with equities located in Bucket #3. The objective of this bucket is safety with some income.

The Bucket approach to retirement portfolio planning isn’t designed to generate the best possible investment returns. It won’t—almost by definition. Instead, the Bucket strategy is geared toward real retirees, to help them source their needed cash flows regardless of what’s going on with their long-term holdings.

By maintaining an ongoing allocation to cash alongside a balanced portfolio, the Bucket approach enables retirees to withdraw funds from those liquid reserves when stock and/or bond values are in a trough. That allocation provides a psychological benefit, too, in that having cash on hand can help retirees cope with the volatility that will inevitably accompany their long-term holdings. In better market environments, retirees can source their cash flow needs from appreciated equity or bond holdings and not touch the cash.

– Christine Benz

Note that the Morningstar Conservative Tax-Advantaged Bucket #2 Portfolio has a combined allocation of 15% in Loan Participation, High Yield, and Emerging Markets Hard Currency Debt. For Readers interested in more from Ms. Benz, I recommend How to Retire – 20 Lessons for a Happy, Successful, and Wealthy Retirement (2024).

Closing

It’s tough to make predictions, especially about the future.

– Yogi Berra

Which of the 3 choices is best? So, the answer is: It depends. It depends on your own comfort level with the risk/reward trade-off. Know thyself. Not just what you intellectually realize, but your actual behavior when it all hits the fan and markets are crashing, and you are down 15% or 20% or 25%, and the pit of your stomach yells, “Run!” Here are my own current calculations and adjustments to align with my risk tolerance. Yours might be different.

Bear markets typically last nine months to a year and a half, while bull markets usually last three to five years. The risk to people depending upon their investments for income is when stock and/or bond market returns are low for extended periods of time. Most of the time, the aggressive sub-portfolio will be up, and withdrawals will come from it. I consider my Traditional IRAs to be in my intermediate Bucket (#2) because I have to take withdrawals from them, but have divided them into conservative and aggressive sub-portfolios with a combined allocation to stocks of less than 40%. Since the stock market is high, I have taken withdrawals from the aggressive TIRA sub-portfolio this year.

In essence, I use parts of all three portfolios discussed in this article. To protect against the downside risk of a secular bear market, I estimated conservative returns and withdrawals from the conservative TIRA sub-portfolio to ensure that it would last ten years. Longer-term, I would like to allocate a small amount to an income-producing mixed-asset growth fund in my conservative TIRA sub-portfolio. I believe the current risk-to-reward favors cash equivalents, and I am starting to build a small cash reserve for when opportunities arise. As bonds mature, I am investing the proceeds into a new rung on my ten-year ladder or conservative income-producing funds already in my Core TIRA. I am considering adding BAMBX as a diversifier.