It looks like you're new here. If you want to get involved, click one of these buttons!

https://www.nytimes.com/2020/10/06/business/trump-taxes-hair.htmlIn 1989, the real estate mogul Leona Helmsley was sentenced to four years in prison for tax evasion after she tried to write off improvements to her estate in Greenwich, Conn., as business expenses.

One of her lawyers was Alan Dershowitz, who defended Mr. Trump during the impeachment proceedings.

The United States attorney who brought the charges? Rudolph W. Giuliani, who appeared this week with Mr. Trump to denounce The Times’s reporting and has called Mr. Trump a “genius” for finding ways to shrink his tax bill.

I bought small positions in SQ+SHOP but sold after I made several % ;-)Just a reminder. .

Are you looking for converts?

By now I think many are aware that you are an active bond fund trader.

I hope it works out for you.

BTW, I see good signs for stocks uptrend since the last bottom about 2 weeks ago.

What are you buying?

Good read with lots of charts but I could not find predictions about the markets, especially near term.

I think the SP500+QQQ are consolidating after a huge run and the next leg is up. The price is bouncing around the 50 days moving average but the trend is still up.

Prediction based on PE + value/growth can be off by years

While no sane tax advisor would suggest swapping VOO for SPY when harvesting a loss, Betterment like many professionals does not say that this is definitely a wash sale. Rather, Betterment writes:For example, while selling VOO (Vanguard S&P 500 ETF) to buy SPY (SPDR S&P 500 ETF) would definitely generate a wash sale, selling VWO (Vanguard FTSE Emerging Markets ETF) to buy IEMG (iShares Core MSCI Emerging Markets ETF) wouldn’t.

How do I know? Because Betterment, one of the domain experts on tax loss harvesting, lists IEMG as the security alternate for VWO in their taxable accounts.

https://www.betterment.com/resources/tax-loss-harvesting-methodology/#wash-salesLess clear is the treatment of two index funds from different issuers (e.g., Vanguard and Schwab) that track the same index. While the IRS has not issued any guidance to suggest that such two funds are “substantially identical,” a more conservative approach when dealing with an index fund portfolio would be to repurchase a fund whose performance correlates closely with that of the harvested fund, but tracks a different index.

https://fairmark.com/investment-taxation/capital-gain/wash/substantially-identical-securities/Because there is no direct authority dealing with this question, reasonable minds may disagree. It’s always possible to identify differences between funds managed by different companies, such as expense ratios and tax load. Some people conclude on this basis that funds maintained by two different companies are never substantially identical.

My feeling is that those differences aren’t enough to prevent the two funds from being substantially identical. The point of the wash sale rule is to determine whether you’ve changed your position relative to the market. If you can lay the price graph for your new investment on top of the price graph for the old one and never see a significant disparity (as would be the case for two high quality S&P 500 funds), the investments should be considered substantially identical for purposes of the wash sale rule.

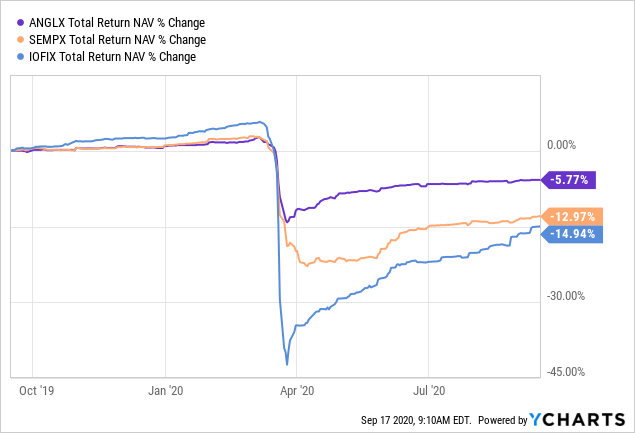

https://seekingalpha.com/article/4377703-update-on-non-agency-mbs-sectorWe noted how AlphaCentric Income Opportunities saw a "run on the fund" where shareholders all liquidated en masse causing a downward spiral in prices.

(Writing about CEFs)....most NAVs are still well below where they were in February even when including the distribution paid since. As we've noted, these securities take the elevator down and stairs back up. We still expect prices to return to around an average price of 90 cents on the dollar but that it would take at least 6 months and more like 18-24 months to do so.

tax-loss-harvestingA successful tax loss harvesting strategy should generate a tax loss in the short run without generating an actual monetary loss in the long run. What I mean by this is that you should never make it an explicit goal to lose money just for the tax benefits. Losing money is always bad for you as an investor. As Warren Buffett’s once said:

The first rule of investment is don’t lose. And the second rule of investment is don’t forget the first rule. And that’s all the rules there are.

However, a good tax loss harvesting strategy can generate losses as they appear without losing money in the long run. How does it do this?

First it sells a security at a loss, and then it takes the proceeds from that sale and buys an “alternate security” that behaves similarly, but not identically to the original security. Why does it purchase an alternate security? Because it wants to generate a tax loss without changing your exposure to the underlying asset class.

For example, let’s say you owned $10,000 of VWO (Vanguard FTSE Emerging Markets ETF) in a taxable account as of January 1, 2020. The optimal tax loss harvesting strategy would have sold your VWO on March 23, 2020 (i.e. the coronavirus bottom) to generate the largest tax loss possible, and then would have immediately taken the proceeds from that sale ($6,817) and bought shares of IEMG (iShares Core MSCI Emerging Markets ETF) to replace it.

And the moment he's gone I'll be bailing.So beware that the bonds in the fund are consisted of lower quality, i.e. junk bonds. In the longer term the risk-reward tilts in his favor. The drawdown in March 2020 was -13.7%. The fund recovered in 6 months and keeps on moving upward.

Are you looking for converts?Just a reminder. .

What are you buying?

BTW, I see good signs for stocks uptrend since the last bottom about 2 weeks ago.

David, thanks for the comments. All true, however, I do not find it common for a CIO to stay only 7 months since being brought on to presumably turn around the performance, which has really taken a nose dive in the last 3 years. Pacific Tiger and Asia Dividend, two of the largest funds, are both less than 50th percentile compared to peers 3-year trailing return. I presume the CIO was brought on to fix that performance, which seemingly never happened as the returns as of August were still poor versus competitors.As Derf notes, Matthews Emerging Markets (MEGMX) is just six months old. It has seen consistent inflows and is sort of clubbing the competition: up 32% since inception versus 20% for its peers in the same period.

Matthews Emerging Asia (MEASX), on the other hand, has had a harder time with three lean years and a couple years of outflows, though the management team has remained unchanged.

I had a chance to chat with some of the Matthews reps. They're a bit concerned that headlines ("Exodus!") will override the substance of the stories: a couple really good managers (and their seconds) moved took plum positions elsewhere, a less excellent manager might have been replaced, and cancelled business initiative in China might have displaced another, all of which is pretty normal in the industry. They admitted to not knowing much about the administrative departure, but promised to try to find out.

For what that's worth,

David

© 2015 Mutual Fund Observer. All rights reserved.

© 2015 Mutual Fund Observer. All rights reserved. Powered by Vanilla