Originally published in October 1, 2014 Commentary

The pre-autumnal weather was perfect. Blue skies. Warm days. Cool nights. Vibrant city scene. New construction. Breath-taking architecture. Diverse eateries, like Lou Malnati’s deep dish pizza. Stylist bars and coffee shops. Colorful flower boxes on The River Walk. Shopping galore. An enlightened public metro system that enables you to arrival at O’Hare and 45 minutes later be at Clark/Lake in the heart of downtown. If you have not visited The Windy City since say when the Sears Tower was renamed the Willis Tower, you owe yourself a walk down The Magnificent Mile.

At the opening keynote, Ben Johnson, Morningstar’s director responsible for coverage of exchange traded funds (ETFs) and conference host, noted that ETFs today hold $1.9T in assets versus just $700M only five years ago, during the first such conference. He explained that 72% is new money, not just appreciation.

The conference had a total of 671 attendees, including 470 registered attendees (mostly financial advisors, but this number also includes PR people and individual attendees), 123 sponsor attendees, 43 speakers, and 35 journalists, but not counting a very helpful M* staff and walk-ins. Five years ago? Just shy of 300 attendees.

The Dirty Words of Finance

AQR’s Ronen Israel spoke of Style Premia, which refers to source of compelling returns generated by certain investment vehicle styles, specifically Value, Momentum, Carry (the tendency for higher-yielding assets to provide higher returns than lower-yielding assets), and Defensive (the tendency for lower-risk and higher-quality assets to generate higher risk-adjusted returns). He argues that these excess returns are backed by both theory, be it efficient market or behavioral science, and “decades of data across geographies and asset groups.”

He presented further data that indicate these four styles have historically had low correlation. He believes that by constructing a portfolio using these styles across multiple asset classes investors will yield more consistent returns versus say the tradition 60/40 stocks/bond balanced portfolio. Add in LSD, which stands for leverage, shorting and derivatives, or what Mr. Israel jokingly calls “the dirty word of finance,” and you have the basic recipe for one of AQR’s newest fund offerings: Style Premia Alternative (QSPNX). The fund seeks long-term absolute (positive) returns.

Shorting is used to neutralize market risk, while exposing the Style Premia. Leverage is used to amplify absolute returns at defined portfolio volatility. Derivatives provide most efficient vehicles for exposure to alternative classes, like interest rates, currencies, and commodities.

When asked if using LSD flirted with disaster, Mr. Israel answered it could be managed, alluding to drawdown controls, liquidity, and transparency.

(My own experience with a somewhat similar strategy at AQR, known as Risk Parity, proved to be highly correlated and anything but transparent. When bonds, commodities, and EM equities sank rapidly from May through June 2013, AQR’s strategy sank with them. Its risk parity flagship AQRNX drew down 18.1% in 31 trading days…and the fund house stopped publishing its monthly commentary.)

When asked about the size style, he explained that their research showed size not to be that robust, unless you factored in liquidity and quality, alluding to a future paper called “Size Matters If You Control Your Junk.”

When asked if his presentation was available on-line or in-print, he answered no. His good paper “Understanding Style Premia” was available in the media room and is available at Institutional Investor Journals, registration required.

Launched in October 2013, the young fund has generated nearly $300M in AUM while slightly underperforming Vanguard’s Balanced Index Fund VBINX, but outperforming the rather diverse multi-alternative category.

QSPNX er is 2.36% after waivers and 1.75% after cap (through April 2015). Like all AQR funds, it carries high minimums and caters to the exclusivity of institutional investors and advisors, which strikes me as being shareholder unfriendly. Today, AQR offers 27 funds, 17 launched in the past three years. They offer no ETFs.

In The Shadow of Giants

PIMCO’s Jerome Schneider took over the short-term and funding desk from legendary Paul McCulley in 2010. Two years before, he was at Bear Stearns. Today, think popular active ETF MINT. Think PAIUX.

During his briefing, he touched on 2% being real expected growth rate. Of new liquidly requirements for money market funds, which could bring potential for redemption gates and fees, providing more motivation to look at low duration bonds as an alternative to cash. He spoke of 14 year old cars that needed to be replaced and expected US housing recovery.

He anticipates capital expenditure will continue to improve, people will get wealthier, and for US to provide a better investment outlook than rest of world, which was a somewhat contrarian view at the conference. He mentioned global debt overhang, mostly in the public sector. Of working age population declining. And, of geopolitical instability. He believes bonds still play a role in one’s portfolio, because historically they have drawn down much less than equities.

It was all rather disjointed.

Mostly, he talked about the extraordinary culture of active management at PIMCO. With time tested investment practices. Liquidity sensitivity. Risk management. Credit research capability, including 45 analysts across the globe that he begins calling at 03:45…the start of his work day. He touted PIMCO’s understanding of tools of the trade and trading acumen. “Even Bill Gross still trades.” He displayed a picture of himself that folks often mistook for a young Paul McCulley.

Cannot help but think what an awkward time it must be for the good folks at PIMCO. And be reminded of another giant’s quote: “Only when the tide goes out do you discover who’s been swimming naked.”

Youthful Hosts

Youthful Hosts

Surely, it is my own graying hair, wrinkled bags, muddled thought processes, and inarticulate mannerisms that makes me notice something extraordinary about the people hosting and leading the conference’s many panels, workshops, luncheons, keynotes, receptions, and sidebars. They all look very young! In addition to being clear thinkers, articulate public speakers, helpful and gracious hosts.

It would not be too much of a stretch to say that the combined ages of M*’s Ben Johnson, Ling-Wei Hew, and Samuel Lee together add up to one Eugene Fama. Indeed, when Mr. Johnson sat across from Nobel laureate Professor Fama, during a charming lunch time keynote/interview, he could have easily been an undergraduate from University of Chicago.

Is it because the ETF industry itself is young? Or, is it as a colleague explains: “Morningstar has hard time holding on to good talent because it is a stepping stone to higher paying jobs at places like BlackRock.”

Whatever the reason, if we were all as knowledgeable about investing as Mr. Lee and the rest of the youthful staff, the world of investing would be a much better place.

Damp & Disappointing

That’s how JP Morgan’s Dr. David Kelly, Chief Global Strategist, describes our current recovery. While I did not agree with everything, it was hands-down the best talk of the conference. At one point he said that he wished he could speak for another hour. I wished he could have too.

“Damp and disappointing, like an Irish summer,” he explained.

Short term US prospects are good, but long term not good. “In the short run, it’s all about demand. But in the long run, it’s all about supply, which will be adversely impacted by labor and productivity.” The labor force is not growing. Baby boomers are retiring en masse. He also showed data that productivity was likely not growing, blaming lack of capital expenditure. (Hard to believe since we seem to work 24/7 these days thanks to amazing improvements communications, computing, information access, manufacturing technology, etc. All the while, living longer.)

Dr. Kelly offered up fixes: 1) corporate tax reform, including 10% flat rate, and 2) immigration reform, that allows the world’s best, brightest, and hardest working continued entry to the US. But since congress only acts in crisis, he concedes his forecast prepares for slowing US growth longer term.

Greater opportunity for long term growth is overseas. Manufacturing momentum is gaining around world. Cyclical growth will be higher than US while valuations remain lower and work force is younger. Simply put, they have more room to grow. Unfortunately, US media bias “always gives impression that the rest of the world is in flames…it shows only bad news.”

JP Morgan remains underweight fixed income, since monetary policy remains abnormal, and cautiously over weight US equities. The thing about Irish summers is…everything is green. Low interest rates. Higher corporate margins. Normal valuation. Although he takes issue with the phrase “All the easy money has been made in equities.” He asks “When was it ever easy?”

Alpha Architect

Dr. Wesley Gray is a former US Marine Captain, a former assistant and now adjunct professor at Drexel University, co-author of Quantitative Value: A Practitioner’s Guide to Automating Intelligent Investment and Eliminating Behavioral Errors, and founder of AlphaArchitect, LLC.

He earned his MBA and Finance PhD from University of Chicago, where Professor Fama was on his doctoral committee. He offers a fresh perspective in the investment community. Straight talking and no holds barred. My first impression – a kind of amped-up, in-your-face Mebane Faber. (They are friends.)

In fact, he starts his presentation with an overview of Mr. Faber’s book “The Ivy Portfolio,” which at its simplest form represents an equal allocation strategy across multiple and somewhat uncorrelated investment vehicles, like US stocks, world stocks, bonds, REITS, and commodities.

Dr. Gray argues that simple, equal allocation remains tough to beat. No model works all the time; in fact, the simple equal allocation strategy has under-performed the past four years, but precisely because forces driving markets are unstable, the strategy will reward investors with satisfactory returns over the long run. “Complexity does not add value.”

He seems equally comfortable talking efficient market theory and how to maximize a portfolio’s Sharpe ratio as he does explaining why the phycology of dynamic loss aversion creates opportunities in the market.

When Professor Fama earlier in the day dismissed a question about trend-following, answering “No evidence that this works,” Dr. Gray wished he would have asked about the so-called “Prime anomaly…momentum. Momentum is pervasive.”

When Dr. Gray was asked, “Will your presentation would be made available on-line?” He answered “Absolutely.” Here is link to Beware of Geeks Bearing Formulas.

His firm’s web site is interesting, including a new tools page, free with an easy registration. They launch their first ETF aptly called Alpha Architect’s Quantitative Value (QVAL) on 20 October, which will follow the strategy outlined in the book. Basically, buy cheap high-quality stocks that Wall Street hates using systematic decision making in a transparent fashion. Definitively a candidate MFO fund profile.

Trends Shaping The ETF Market

Ben Johnson hosted an excellent overview ETF trends. The overall briefings included Strategic Beta, Active ETFs (like BOND and MINT), and ETF Managed Portfolios.

Points made by Mr. Johnson:

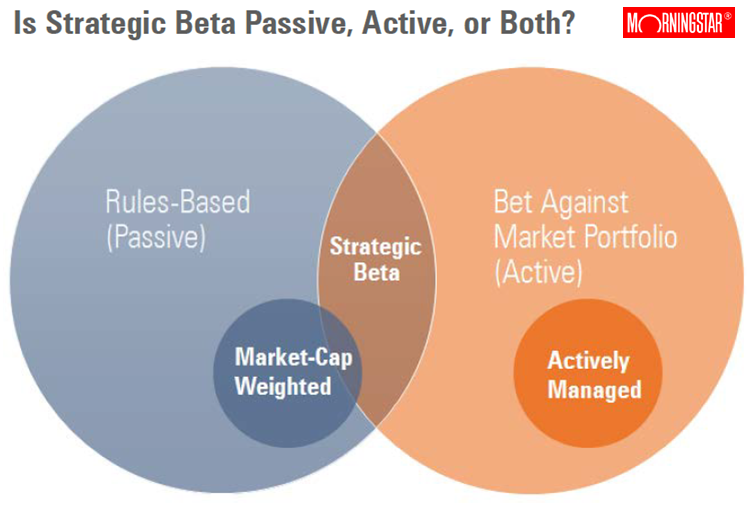

1. Active vs passive is a false premise. Today’s ETFs represent a cross-section of both approaches.

2. “More assets are flowing into passive investment vehicles that are increasingly active in their nature and implementation.”

3. Smart beta is a loaded term. “They will not look smart all the time” and investors need to set expectations accordingly.

4. M* assigns the term “Strategic Beta” to a growing category of indexes and exchange traded products (ETPs) that track them. “These indexes seek to enhance returns or minimize risk relative to traditional market cap weighted benchmarks.” They often have tilts, like low volatility value, and are consistently rules-based, transparent, and relatively low-cost.

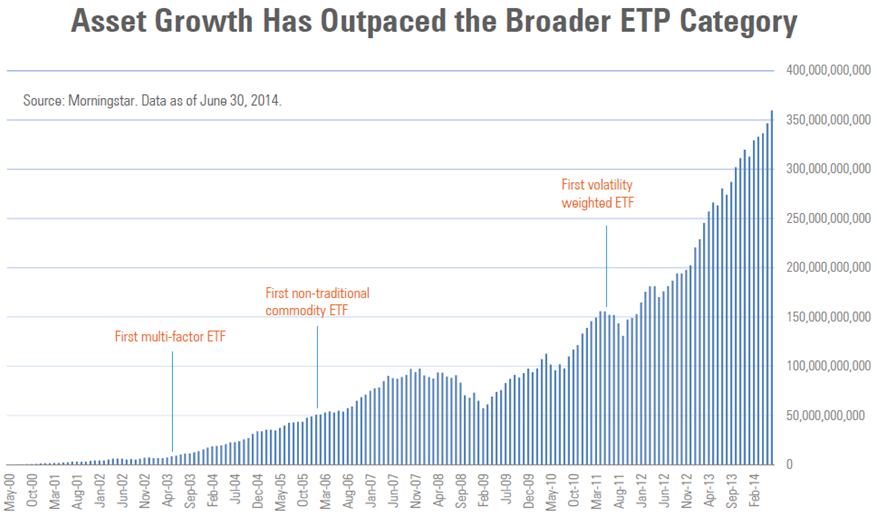

5. Strategic Beta subset of ETPs has been explosive in recent years with 374 listed in US as of 2Q14 or 1/4 of all ETPs, while amassing $360M, or 1/5th of ETP AUM. Perhaps more telling is that 31% of new cash flows for ETPs in 2013 went into Strategic Beta products.

6. Reduction or fees and a general disillusionment with active managers are two of several reasons behind the growth in these ETFs. These quasi active funds charge a fraction of traditional fees. A disillusionment with active managers is evidenced in recent surveys made by Northern Trust and PowerShares.

M* is attempting to bring more neutral attention to these ETFs, which up to now has been driven by product providers. In doing so, M* hopes to help set expectation management, or ground rules if you will, to better compare these investment alternatives. With ground rules set, they seek to highlight winners and call out losers. And, at the end of the day, help investors “navigate this increasingly complex landscape.”

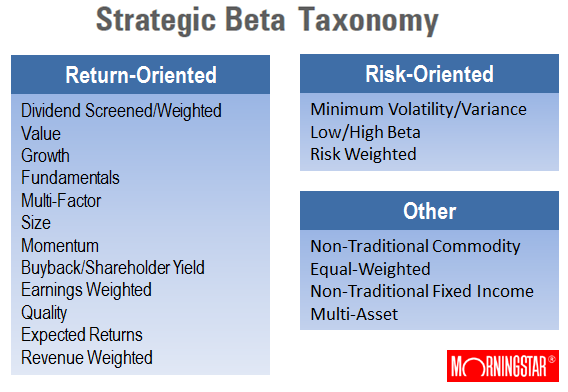

They’ve started to develop the following taxonomy that is complementary to (but not in place of) existing M* categories.

Honestly, I think their coverage of this area is M* at its best.

Welcomed Moderation

Mr. Koesterich gave the conference opening keynote. He is chief investment strategist for BlackRock. The briefing room was packed. Several hundred people. Many standing along wall. The reception afterward was just madness. His briefing was entitled “2014 Mid-Year Update – What to Know / What to Do.”

He threaded a somewhat cautiously reassuring middle ground. Things aren’t great. But, they aren’t terrible either. They are just different. Different, perhaps, because the fed experiment is untested. No one really knows how QE will turn out. But in mean time, it’s keeping things together.

Different, perhaps, because this is first time in 30-some years where investors are facing a rising interest rate environment. Not expected to be rapid. But rather certain. So bonds no longer seem as safe and certainly not as high yield as in recent decades.

To get to the punch-line, his advice is: 1) rethink bonds – seek adaptive strategies, look to EM, switch to terms less interest rate sensitive, like HY, avoiding 2-5 year maturities, look into muni’s on taxable accounts, 2) generate income, but don’t overreach – look for flexible approaches, proxies to HY, like dividend equities, and 3) seek growth, but manage volatility – diversify to unconstrained strategies

More generally, he thinks we are in a cyclical upswing, but slower than normal. Does not expect US to achieve 3.5% annual GDP growth (post WWII normal) for next decade. Reasons: high debt, aging demographics, and wage stagnation (similar to Rob Arnott’s 3D cautions).

He cited stats that non-financial debt has actually increased 20-30%, not decreased, since financial crisis. US population growth last year was zero. Overall wages, adjusted for inflation, same as late ’90s. But for men, same as mid ‘70s. (The latter wage impact has been masked by more credit availability, more women working, and lower savings.) All indicative of slower growth in US for foreseeable future, despite increases in productivity.

Lack of volatility is due to fed, keeping interest rates low, and high liquidity. Expects volatility to increase next year as rates start to rise. He believes that lower interest rates so far is one of year’s biggest surprises. Explains it due to pension funds shifting out of equities and into bonds and that US 10 year is pretty good relative to Japan and Europe.

On inflation, he believes tech and aging demographics tend to keep inflation in check.

BlackRock continues to like large cap over small cap. Latter will be more sensitive to interest rate increases.

Anything cheap? Stocks remain cheaper than bonds, because of extensive fed purchases during QE. Nothing cheap on absolute basis, only on relative basis. “All asset classes above long term averages, except a couple niche areas.”

“Should we all move to cash?” Mr. Koesterich answers no. Just moderate our expectations going forward. Equities are perhaps 10-15% above long term averages. But not expensive compared to prices before previous drops.

One reason is company margins remain high. For couple of same reasons: low credit interest and low wages. Plus higher productivity, which later appeared contrary to JP Morgan’s perspective.

He advises investors be selective in equities. Look for value. Like large over small. More cyclical companies. He likes tech, energy, manufacturing, financials going forward. This past year, folks have driven up valuations of “safe” equities like utilities, staples, REITS. But those investments tend to work well in recessions…not so much in rising interest rate environment. EM relatively inexpensive, but fears they are cheap for reason. Lots of divided arguments here at BlackRock. Japan likely good trade for next couple years due to Japanese pension funds shifting to organic assets.

He closed by stating that only New Zealand is offering a 10 year sovereign return above 4%. Which means, bond holders must take on higher risk. He suggests three places to look: HY, EM, muni’s.

Again, a moderate presentation and perhaps not much new here. While I personally remain more cautiously optimistic about US economy, compared to mounting predictions of another big pull-back, it was a welcomed perspective.

Beta Central

I’m hard-pressed to think of someone who has done more to enlighten investors about the benefits of ETF vehicles and opportunities beyond buy-and-hold US market cap than Mebane Faber. At this conference especially, he represents a central figure helping shape investment opportunities and strategies today.

He was kind enough to spend a few minutes before his panel on dividend investing and ETFs, which he held with Morningstar’s Josh Peters and Samuel Lee.

He shared that Cambria recently completed a funding campaign to expand its internal operations using the increasingly popular “Crowd Funding” approach. They did not use one of the established shops, like EquityNet, simply because of cost. A couple hundred “accredited investors” quickly responded to Cambria’s request to raise $1-2M. The investors now have a private stake in the company. Mebane says they plan to use the funds to increase staff, both research and marketing. Indeed, he’s hiring: “If you are an A+ candidate, incredibly sharp, gritty, and super hungry, come join us!”

The new ETF Global Momentum (GMOM), which we mentioned in the July commentary, is due out soon, he thinks this month. Several others are in pipeline: Global Income and Currency Strategies ETF (FXFX), Emerging Shareholder Yield ETF (EYLD), Sovereign High Yield Bond ETF (SOVB), and Value and Momentum ETF (VAMO), which will make for a total of eight Cambria ETFs. The initial three ETFs (SYLD, FYLD, and GVAL) have attracted $365M in their young lives.

He admitted being surprised that Mark Yusko of Morgan Creek Funds agreed to take over AdvisorShares Global Tactical ETF GTAA, which now has just $20M AUM.

He was also surprised and disappointed to read about the SEC’s probe in F2 Investments, which alleges overstated performance results. F2 specializes in strategies “designed to protect investors from severe losses in down markets while providing quality participation in rising markets” and they sub-advise several Virtus ETFs. When WSJ reported that F2 received a so-called Wells notice, which portends a civil case against the company, Mebane posted “first requirement for anyone allocating to separate account investment advisor – GIPS audit. None? Move on.” I asked, “What’s GIPS?” He explains it stands for Global Investment Performance Standards and was created by the CFA Institute.

Mebane continues to write, has three books in work, including one on top hedge funds. Speaking of insight into hedge funds, subscribers joining his The Idea Farm after 31 December will pay a much elevated $499 annually.