Rakesh Bordia co-manages Pzena Emerging Markets Value Fund (“the fund”) with tenured co-managers Caroline Cai, Allison Fisch, and (recently added) Akhil Subramanian. The strategy has approximately $1.35 billion under management and has been around just since 2014. Investing in emerging markets has been no cakewalk for this window. The passive Vanguard FTSE Emerging Markets ETF (VWO), over the past 15 years, has earned just south of 3% annualized.

Rakesh Bordia co-manages Pzena Emerging Markets Value Fund (“the fund”) with tenured co-managers Caroline Cai, Allison Fisch, and (recently added) Akhil Subramanian. The strategy has approximately $1.35 billion under management and has been around just since 2014. Investing in emerging markets has been no cakewalk for this window. The passive Vanguard FTSE Emerging Markets ETF (VWO), over the past 15 years, has earned just south of 3% annualized.

Pzena EM Value Fund has earned just north of 4% a year since its inception. The interesting part of capitalism is that there is always something going on. Since the pandemic lows, this fund has earned 23% annualized, almost double the VWO.

Lifetime Performance (April 2014 – July 2023)

| Annual return | Max drawdown | Standard deviation | Downside deviation | Ulcer Index |

Sharpe Ratio |

|

| Pzena Emerging Markets Value | 4.8% | -38.0 | 18.9 | 12.6 | 16.1 | 0.19 |

| Lipper EM Equity Peers | 2.0 | -41.4 | 18.8 | 13.2 | 18.0 | 0.08 |

Source: MFO Premium fund screener and Lipper Global Data Feed

A year ago, we had a series of long, detailed conversations with six of the industry’s best emerging markets managers, representing a variety of investment strategies and advisors from Causeway to Pzena. Those conversations led to two articles: Emerging Markets (EM) Investing in the Next Decade: The Game and Emerging Markets Investing in the Next Decade: The Players. At that time, he had made the case for the fund:

- People panic in EM far more than in DM. These panic moments create value opportunities in those countries where a great asset might be hit along with everything else.

- We like to swoop in then, accompanied by deep research, value analysis, and long-term holding periods.

- Many high-quality value businesses are trading at 10-15% FCF yield with good ongoing business models. But…

- EM returns are very lumpy. This compelling valuation starting point means that stock returns are obvious, but the timing is always unclear in our business.

On a sleepy day in early August 2023, we got on a Zoom call, where I had a chance to pick Rakesh’s brain on what was working and why his fund’s performance was a solid 20% year-to-date in 2023.

“We were lucky,” he said humbly. “In a different comparison window, we wouldn’t look as good. End point bias matters when comparing funds and performance.”

It’s true that we are prejudiced and more likely to be interested in funds and managers where something is working than where it’s not. Winners see the ball differently, and the rest of us can always benefit by improving our game. Since we also know that the market has NOT generally been rewarding strategies in EM or Value, this fund’s performance matters even more. The combination of different and winner is too good to not investigate. This is the stuff real diversification is made of.

I share some themes of what Rakesh Bordia (RB) shared with me on the Zoom call.

RB: The story consists of 3 important ingredients: We are active investors in EM, Pzena’s research process is very deep, and we should talk about how our fund traversed the last many years and why that has continued to work for us.

[Let’s use a stock that Rakesh brought up – a Chinese company called Weichai Power, a 1.4% holding in the fund – to get a glimpse into their process.]

RB: Weichai is the largest heavy-duty truck engine manufacturer in China (among other industrial business in equipment, logistics, and supply chain services). In China, trucks have a lower shelf life. In the USA, a truck might be driven about 10 hours a day. In China, the same truck would be driven 15 hours a day in two shifts. Because it’s driven more, a truck in China needs to be replaced every seven years (compared to 10 years in the US).

The fund managers are aware that the Chinese GDP is slowing and the economy is maturing. However, looking at the replacement demand for trucks over the next ten years already makes the stock cheap. If the GDP grows anything more than the 3% of mature economies, the business is very attractive. Plus, there is a European business that has upside potential.

Pzena’s sweet spot is bad macro + company-specific issues, leading to a sharp sell-off in the stock. We want to find cheap businesses where there are NO CATALYSTS immediately in sight. We want opportunities where 3-5 years might be required to turn things around. In EM, management and governance changes take a lot of time.

The Seth Klarman interlude: new edition of Security Analysis, classic investing insights

Graham and Dodd’s Value Investing Bible – Security Analysis – just released a 7th edition. Seth Klarman, the founder and portfolio manager of hedge fund Baupost, plays the role of Editor. This is a must-read for any serious investor because of the cover chapters written by excellent investors like Klarman himself, Todd Combs of Berkshire Hathaway, Howard Marks, and others. Seth Klarman rarely talks in public, but in conjunction with the book release, he did a long podcast with Ted Seides. The Capital Allocators Podcasts are phenomenal listening material, and this one with Klarman did not disappoint.

If we listen closely to what he said and what he wrote in the cover chapter for Security Analysis, Klarman talks about his value investing hedge fund process. This was an important learning moment as it highlighted the difference between what Pzena and Baupost are trying to do.

Both are successful value investors, but Baupost needs a catalyst along with value.

Pzena being long-only money may look for value opportunities with no immediate catalysts in sight. In fact, to them, that’s the sweet spot because those stocks would be untouchable for hedge funds.

RB: Weichai took several months of research. They have the highest market share in China. We looked into the risks of hydrogen and EV batteries. Hydrogen is at least ten years away. Weichai has a great Balance sheet. Their construction and forklift divisions are gaining tremendous market share. Europe + macro + engine demand can all improve, and you are not paying for any of it. Once we determined that there was value, we did lots of research and scenario analysis before initiating the position. One cannot just look at trucking in the US and assume that’s how it will be replicated globally. Fundamental research shows the nuances and thus the opportunities.

RB: It’s not enough for the stock to just be cheap. Enormous research goes into avoiding value traps. We look for a $1.5 Billion minimum market cap. All investment decisions require unanimous agreement among the managers.

Discipline: To us, it is always “what you are paying vs. what you are getting.” We are never, ever, going to be out-researched. The firm’s process has been disciplined since 1995 as deep value investors. The EM team has been together for about seven years now, with very long-tenured members serving as portfolio managers. In EM, more than anywhere else, a long-term waiting period for your holdings is important.

Skirting China: From 2017 to 2019, Chinese equities were most loved in EM, and mega tech Chinese names could do no wrong. Our goal is to find great businesses at cheap valuations, and we could not find many businesses to buy in China. Despite their huge weights in the EM Indices, we avoided stocks like Tencent and Alibaba. When China was 42% of EM Equities, our allocation was only 17%. When clients questioned this, our explanation was that those businesses were priced for perfection. We were also worried about political and regulatory risks. We got a lot of scrutiny for our Chinese underweight (but no money was pulled).

The Yin became Yang: In 2021-2022, Chinese stocks were down 30%, while the Rest of EM was up 15%. We benefitted from being out. After the washout, Chinese businesses started screening attractive again. While the EM Index Chinese weights have gone down (ed note – from 42 to 32%), Pzena’s EM fund weight has gone up to 27%.

[The conversation was much longer with lots of insight into EM indices, US stocks, and cap-weighted indices. One particular point stands out about passive investing.]

RB: Think of a large growth stock in US indices in 2018 vs. 2022. In 2018, let’s say the stock had an EPS of 10 and a market cap of 100. In 2022, the stock still has an EPS of 10 but a market cap of 400. The passive index has a 4X investment in that stock in 2022 compared to 2018. Overall, passive is pro-cyclical. For many investors, the true way to make money is by betting on countercyclical investments. That is, buying something truly out of favor for much cheaper than you can buy it in an efficient world. The curse of the investment management industry is that it forces us to be index huggers.

Pzena’s managers are pure stock pickers and remarkably successful ones

Pzena shared an attribution report with MFO, a report they would usually share with potential investors. The simple takeaway from that report was that Pzena’s returns come not from choosing countries and sectors within EM but pure stock selection. They are stock people. Process people. And that’s all they do — day in and day out. It’s important to understand this as we think about why it makes sense to trust some active managers with our investments.

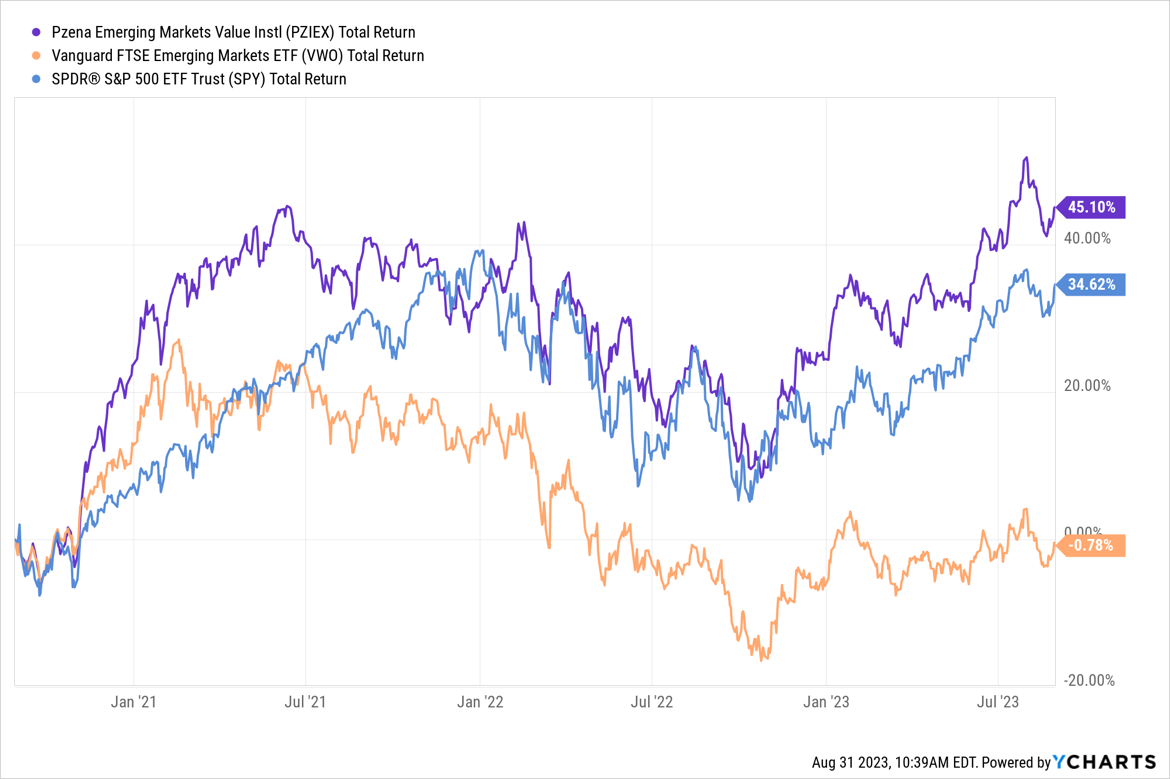

So, what do the results for being EM + active + deep value Pzena style look like? To compare (yes, yes, I know), we have here three assets: the SPDR S&P 500 ETF (SPY), the Vanguard FTSE Emerging Market ETF (VWO), and Pzena’s EM Value Fund (PZIEX) over the last three years. As you can see with the purple line, PZIEX outperformed both the S&P 500 and VWO. It beat the passive EM by close to 46% total return and even beat the mighty S&P 500 by more than 10% points over that period.

RB: Investors recognize and trust Pzena’s process, which is why we have been receiving more than our fair share of inflows as other managers in the EM world are going through hiccups.

[I asked him how he would manage his own money in the future, advice for our readers.]

RB: I would find two good Value investors and two good Growth investors. I would want them to be consistent and disciplined with their process across time.

In Conclusion

In the last few months, we have sat down with a series of value-oriented managers. Moerus, Aegis, Seafarer, and now Pzena. Process and stock selection are incredibly important to these managers. Pzena does what it does – deep value investing. Many investors no longer want to be in EM. That’s fine because of the performance of passive EM indices. But funds like Pzena’s should at least make one pause and think about one’s conviction to not be invested in EM equities. I am an investor in Pzena’s EM fund.