Dear friends,

Welcome to the end of the summer. And to the beginning of … the weakest month of the year for the stock market, with an average monthly loss of about 0.7%. And the threshold of the most volatile month of the year, October, which sees an intramonth movement of 8.3%; that is, since 1928, the record says that your portfolio will bounce 8.3% in October (but only 5.2% in February). My inbox overflows with apocalyptic forecasts and also of celebrations of The New Bull. Recognizing that it’s all bull of a sort, I move on.

Augustana welcomes the largest first-year class in its 163-year history, materially (and disconcertingly) fed by the Augustana Possible scholarships that debuted this fall. Alumni-supporting, Augustana Possible fills the aid gap for any high-achieving student from a lower-income family. Good news: 800 amazing newcomers, including 160 students from 33 countries beyond the US. Their courage and ambition is amazing! Bad news: that’s rather more than we have dorm space for. Hmmm … I’ll be curious to see if anyone’s slipped bunkbeds into my office by Labor Day.

And, of course, the presidential nominating circus in which people whom we might not trust to run a dog-walking business will try to howl their way into our hearts in pursuit of running a national government.

But, too, it’s the beginning of Oktoberfest (September 16th is the kick-off; the original was a five-day celebration of the marriage of Prince Ludwig beginning 12 October 1810 with the date shifting as partiers noticed that October days were short and nights were nippy) and of apple season. Which also means apple cider donut season! Which also means that Chip and I have a date with the Brightonwoods Orchard, which has over 200 heirloom apple varieties.

If you’ve got taste buds and a taste for adventure, you really should find time in the next month to get away to an heirloom / antique orchard in your region. Snacking on an apple that dates to the Roman invasion of Gaul, or one that tastes a lot like caramel, is a trip in time.

In the September MFO

A quick and tasty issue, shortened a bit by our late August appearance. Devesh talks emerging markets value with Rakesh Bordia of Pzena Emerging Markets Value. I profile Artisan International Explorer, an extension of David Samra’s international value strategy led by Bieni Zhou and Anand Vasagiri. Lynn Bolin ranks and rates notable young ETFs for you and also walks through the process of assessing tax-exempt bond funds. Finally, The Shadow offers a round-up of industry news – including several notable announcements – in Briefly Noted.

And a special shout-off to Aahan Shah, Devesh’s computer-savvy son, who has spent much of the summer upgrading the Fund Archives for you. He’s made hundreds of edits to update names, fates, managers, expenses, and so on. We’re deeply grateful to him!

But, before all that, there are …

Ten things I learned in August that only I might find interesting.

But, who knows? You’re weird. You might be intrigued, too. Let’s see.

For college professors, as for many of us, summer is a time to sneak in a bit of reading and reflection that the hubbub of the busy part of the year forbids. As we transition from summer issues of MFO and relaxed evenings huddled away from the heat, I surveyed some of the most interesting snippets that I discovered in late summer (some financial, some not) and thought I’d share.

There is a best age for making financial decisions.

It’s 53.

Our abilities are controlled by two distinct types of intelligence, a sort of mental yin and yang. Fluid intelligence is a measure of our ability to make graceful mental leaps, connecting disparate things in ways no one has done before. Researchers say it peaks in our late 20s and, more or less gradually, declines thereafter. Crystallized intelligence is a measure of the amount of stuff we’ve learned (and learn how to do) over the years and can access when we encounter a challenge. It accumulates steadily through adulthood, maxing out somewhere around 70. The difference is important: if you have a problem requiring a brilliant leap (“How do we manage the threat from AI to the trust we’ve built with investors?”), find someone young and brilliant. If you have a problem that requires knowing stuff and having a sense of perspective, hire me. Well, older people.

Our abilities are controlled by two distinct types of intelligence, a sort of mental yin and yang. Fluid intelligence is a measure of our ability to make graceful mental leaps, connecting disparate things in ways no one has done before. Researchers say it peaks in our late 20s and, more or less gradually, declines thereafter. Crystallized intelligence is a measure of the amount of stuff we’ve learned (and learn how to do) over the years and can access when we encounter a challenge. It accumulates steadily through adulthood, maxing out somewhere around 70. The difference is important: if you have a problem requiring a brilliant leap (“How do we manage the threat from AI to the trust we’ve built with investors?”), find someone young and brilliant. If you have a problem that requires knowing stuff and having a sense of perspective, hire me. Well, older people.

Making good decisions, especially of a type we haven’t made before, benefits from having both types of intelligence. Researchers have looked at how we think about finances and how we make our decisions across our lives. Some of the research looked at crystallized knowledge of finance. Some looked at financial problem-solving. And both sets come to very similar conclusions:

Rafal Chomik, an economist in Australia at the ARC Centre of Excellence in Population Ageing Research … led a 2022 study that looked at financial literacy, which is the ability to understand financial information and apply it to managing personal finances. Financial literacy typically peaks at age 54 and then declines, according to the study.

In [another] study, economists looked at financial choices made by adults in 10 financial areas, including home-equity loans, lines of credit, mortgages and credit cards, and how those decisions affected fees and interest payments. Fees and interest payments, across all 10 areas, are at their lowest levels around age 53, according to the 2009 study in the Brookings Papers on Economic Activity. That age was referred to as the “age of reason.” (Claire Ansberry, “The Exact Age When You Make Your Best Financial Decisions,” Wall Street Journal,” 8/26/2023)

Good news: Chip is 53! Bad news: She’s been letting me handle our portfolio. (I think I can hear the account passwords changing from here.) Hmmm … I wonder what my allowance will be? On the upside, given the research, she’ll pick the perfect amount.

Collapsing attention spans: a portfolio perspective.

There is a robust body of research that supports two conclusions. First, our attention spans are short. Second, they’re getting shorter. (Did you even finish that sentence?)

Indeed, research [Gloria Mark, a professor of informatics at the University of California, Irvine, and author of Attention Span: A Groundbreaking Way to Restore Balance, Happiness and Productivity] suggests we’re giving into digital temptation more and more. In the early 2000s, she and her team tracked people while they used an electronic device and noted each time their focus shifted to something new—roughly every 2.5 minutes, on average. In recent repeats of that experiment, she says, the average has gone down to about 47 seconds. Why Everyone’s Worried About Their Attention Span—and How to Improve Yours, Time Magazine, 8/10/2023)

Yikes. We have to measure attention indirectly by looking at what you’re doing and how long you stick with it before getting bored or distracted and moving on. A bunch of different measures, used by a bunch of different scholars, reach the same general conclusion: We have trained our brains to surrender to distraction (check how many tabs or apps you have open at this very second), and our brains have gotten the message: “peek and run away!”

Good news: that’s longer than a goldfish’s attention span (about 9 seconds), and we’ve never tried measuring a butterfly’s. That’s about it for good news.

The definitive MFO Portfolio Guide in 46 seconds:

- Take the year you were born. Add 70.

- Take the resulting number and round down to the next number ending “0” or “5.”

- Invest your portfolio in a T. Rowe Price fund ending with that number.

- Never touch your money again, you butterfly!

Really. Money is important. If you don’t have time to do it right, do it simply, as in the example above. Our only amendment for those with an extra five seconds:

3A. Stash $2,000 in a high-rate money market fund to cover inevitable emergencies.

Bad ideas are quietly bleeding to death.

Quite apart from the demise of the stupid Long Cramer ETF, which The Shadow chronicles in this month’s “Briefly Noted.”

Stupid ideas and converted mutual funds are the lifeblood of the ETF industry. By stupid ideas, I mean funds that were imagined in some sort of Red Bull fueled marketing scrum by desperate people who had seen something cross their news feeds (“More states legalize pot” or “Boeing unveils hypersonic aircraft model” or “you can buy used undies from vending machines in Japan” – really) and cried out “that’s it! Let’s go for it!” And, you end up with the Yield Premium Coca Cola ETF, or the Asian Middle Class ETF, or the KPOP and Korean Entertainment ETF.

The industry does that because they have no competitive advantage (no “edge,” in Devesh’s term) in investing in recognized asset classes and are appealing to an investor base with a 47-second attention span.

Good news: those funds are withering and dying in droves.

Exchange-traded funds are closing down at a rapid clip, with many niche products in the industry struggling to attract investors in a market dominated by a handful of big technology stocks. Global fund closures have climbed to 929 in 2023, rising at a record pace from 373 at the same point last year …

Many of the closed funds were launched just a year or two ago with a narrow thematic focus and never attracted a sustainable asset base. Small asset managers rushed to tap into the individual investing boom with specialized funds that gave everyday investors the tools to trade like a Wall Street pro or bet on the latest hot theme. Just a few years later, they are reckoning with the reality that there might not be enough demand to support many of the funds.

Among this year’s casualties: a metaverse equity ETF focused on the concept popularized by Mark Zuckerberg, a “Generation Z” ETF that promised to invest in companies aligned with the values of the younger generation, a pair of ETFs that bought stocks purchased by Republican or Democratic members of Congress, and a suite of funds offering leveraged exposure to various single stocks. One of the most recent closures came Friday when a cannabis-themed ETF whose shares had declined about 90% since its 2021 launch was liquidated. (Jack Pitcher, “Investors Say No Thanks to Gen-Z, Metaverse Funds,” WSJ, 8/30/2023, paywall)

Oops! I did it again!

And really, who understands the financial management business better than Brittney Spears?

And really, who understands the financial management business better than Brittney Spears?

Oops, I did it again

I played with your heart, got lost in the game

Oh baby, baby

Oops, you think I’m in love

That I’m sent from above

I’m not that innocent.

Speaking of “doing it again” and “not noticeably innocent,” the kleptomaniacal Wells Fargo has done it again. The SEC has again slammed Wells Fargo for ripping off the people who trusted it: “For years (emphasis added), Wells Fargo and its predecessor firms negotiated reduced advisory fees with thousands of clients, but failed to honor them, overcharging those clients millions of dollars as a result.” In this case, the SEC found Wells was guilty of “overcharging more than 10,900 investment advisory accounts more than $26.8 million in advisory fees.”

We’ll ask again the question we asked back in January 20223:

Why does Wells Fargo have any customers left?

Really.

These people are so consistently predatory that the director of the federal Consumer Financial Protection Bureau has denounced Wells’ “rinse-repeat cycle of violating the law” and imposed nearly $4 billion in penalties. That follows the $3 billion penalty imposed by the Department of Justice and SEC two years ago. The latest crimes involve illegal repossession of people’s homes and cars, on top of profitable and illegal overdraft fees.

These people are so consistently predatory that the director of the federal Consumer Financial Protection Bureau has denounced Wells’ “rinse-repeat cycle of violating the law” and imposed nearly $4 billion in penalties. That follows the $3 billion penalty imposed by the Department of Justice and SEC two years ago. The latest crimes involve illegal repossession of people’s homes and cars, on top of profitable and illegal overdraft fees.

Ethan Wolf-Mann chronicled the complete list of Wells Fargo scandals for 2016-2019, where the firm managed a rigorous pace with nearly one scandal per month. The Congressional Research Service covers the same time range in a less engaging style. The FinanChill blog extended the scandal roster back to 2010.

The “lather-rinse-repeat” cycle mentioned above is almost reassuring in its constancy: combine rapacious impulses and a near-total disregard for the need for internal control structures, screw the people who’ve entrusted their financial security to you, get caught, flop about, then pay another couple billion in penalties while promising that this time is really is THE NEW Wells Fargo, then repeat. While other firms have been more egregious, none of them have survived.

If you search “Wells Fargo” at MFO, you’ll find more than 500 mentions of the firm. Many are from the MFO Discussion Board … and well more than half appear to highlight the firm’s scandals.

We’re slowly catching up with Roman building technology.

There are three things you need to know about concrete.

- We use mountains of it. Concrete is the most widely used material on the planet. We use 14 billion metric tons of it each year. That includes 3-4 billion tons of cement (the stuff that holds it together, known as “clinker”) and 10 billion tons of aggregate (the rock and sand that make up the body. Since the start of the industrial revolution, we’ve poured over 900 billion tons of the stuff.

- It’s not very good. Our concrete tends to crack and crumble; it’s almost impossible to make long-lasting repairs, and so it’s got to be replaced all the time. (Do a quick check on your driveway. Notice your blood pressure on your drive to work as you dodge craters and creep through construction.) Nominally, a reinforced concrete structure might last 50-100 years, but the “economic life” of it, the tipping point on a repair-or-replace decision, is just 30 years.

- It is an unparalleled environmental disaster. We produce cement by burning rocks in kilns at 2,732 degrees; that process consumes 5% of all of the world’s energy, something like 9% of our industrial water use, and produces 8% of all of its greenhouse gas emissions. We produce aggregate by dredging sand and gravel from rivers and deltas, which plays havoc with water quality and the aquatic environment.

The curious thing is that Romans made what was, in many ways, better concrete than ours. Roman structures persist, structurally sound, after 1800 – 2000 years, and there’s no evidence that they’re near the end of their lives.

Grain of Roman concrete, with calcium and a big ol’ lime clast in red

The key is that Roman concrete, unlike ours, is self-healing. The Romans incorporated two substances into their concrete – volcanic ash and clast – that caused cracks to seal before the concrete was damaged. More importantly, the new “healed” sections of the concrete were stronger than the original. As a result, with time, Roman concrete becomes stronger and more impermeable. Ours becomes cracked, weaker, and crumbles.

Why so? In marine concrete, the volcanic ash used by the Romans would be exposed to seawater when it cracked. The seawater would dissolve part of the ash, but the resulting solution would form interlocking crystals that were stronger than concrete and impervious to water. In inland concrete, the clast – relatively big chunks of lime – functioned the same way. Traditionally, we thought the clast was inadvertent, the result of Roman carelessness. Hah, stupid us!

As soon as tiny cracks start to form within the concrete, they can preferentially travel through the high-surface-area lime clasts. This material can then react with water, creating a calcium-saturated solution, which can recrystallize as calcium carbonate and quickly fill the crack, or react with [volcanic] materials to further strengthen the composite material. These reactions take place spontaneously and therefore automatically heal the cracks before they spread … the team produced samples of hot-mixed concrete that incorporated both ancient and modern formulations, deliberately cracked them, and then ran water through the cracks. Sure enough: Within two weeks the cracks [in Roman concrete] had completely healed and the water could no longer flow. (“Riddle solved: Why was Roman concrete so durable?” MIT News, 1/6/2023)

We need to use less concrete. That occurs if (1) our concrete lasts longer, (2) our concrete is stronger, so we need less of it, and (3) we find a substitute for some applications. Good news: we’re making gains in all three.

Scientists have now discovered how to incorporate burnt coffee grounds into concrete, displacing traditional aggregate and making it 30% stronger in the process. We produce 60 million pounds of grounds each year, so that makes a substantial difference. (Chip and I alone could repave 53rd Street in Davenport.)

They have also discovered that incorporating graphene – a one-atom-thick honeycomb made of carbon – into concrete makes it “2.5 times stronger and four times less water permeable than standard concrete. It uses much less cement to deliver the desired strength. As a result, it is expected to reduce CO2 emissions by 30%” (Materials of the future: Graphene and concrete, 2023).

Other teams this year explored the potential of fungus (don’t go “yuck”!) as a building material. They call it “myocrete.” Mushrooms are just the surface manifestations of networks of ultra-strong roots, called mycelium, that can extend for miles. In a true science fiction moment, researchers have learned how to literally build fire-proof, lightweight walls (“The growing field of fungus in low carbon, sustainable building materials,” 8/3/2023). That sort of construction is central to the “Monk and Robot” science fiction duology, Prayer for the Wild-Built and A Prayer for the Crown-Shy. They are, between them, profoundly optimistic tales about our ability to work ourselves out of our current mess.

Other teams this year explored the potential of fungus (don’t go “yuck”!) as a building material. They call it “myocrete.” Mushrooms are just the surface manifestations of networks of ultra-strong roots, called mycelium, that can extend for miles. In a true science fiction moment, researchers have learned how to literally build fire-proof, lightweight walls (“The growing field of fungus in low carbon, sustainable building materials,” 8/3/2023). That sort of construction is central to the “Monk and Robot” science fiction duology, Prayer for the Wild-Built and A Prayer for the Crown-Shy. They are, between them, profoundly optimistic tales about our ability to work ourselves out of our current mess.

Still, other teams are working on creating self-healing concrete through embedding bacteria, which, when water reaches them, consumes the water and some of the surrounding concrete to protect new limestone, sealing the crack for good.

Best of all, concrete is a carbon sink. That is, concrete absorbs CO2 naturally for as long as it stands. If we can produce buildings with walls that will last centuries and don’t need to be enormously thick for strength, they will passively wick greenhouse gases out of the air for centuries.

Most wildfires are actually grass fires.

The horror of the fires in Maui – one of the five deadliest in American history – have furnished lead stories in the news worldwide. But as we mourn the losses from the hundreds of fires burning across Canada and the western US, we tend to lose sight of the fact that these aren’t primarily “forest fires.” They’re grass fires, often fueled by non-native grasses withered by drought. Estimated are that two-thirds of all wildfires, including those that spread to forests, are fundamentally burning grass.

The horror of the fires in Maui – one of the five deadliest in American history – have furnished lead stories in the news worldwide. But as we mourn the losses from the hundreds of fires burning across Canada and the western US, we tend to lose sight of the fact that these aren’t primarily “forest fires.” They’re grass fires, often fueled by non-native grasses withered by drought. Estimated are that two-thirds of all wildfires, including those that spread to forests, are fundamentally burning grass.

Grass fires are particularly pernicious because they’re so hard to take seriously. “Your lawn caught fire? Seriously? Okay, I’ll grab a hose and …” That misplaced sense of familiarity is fatal. Fortunately, understanding that grass is the risk allows us – individually and collectively – to better anticipate and control a lot of the conditions that put us at risk.

Buying buy-write funds as a magic shield or not

Anxious investors look for magical solutions: wands, shields, and wizards. One source of that magic is the option-trading or buy-write funds. The shortest version is that the fund puts 95% of its assets in a traditional asset class and uses the remaining 5% to buy an insurance policy against loss.

The folks at the Leuthold Group wanted to check whether the promised magic in these 200 or so funds and ETFs is all that. Their conclusion, which I’ll quote in full, is that very few such funds provide a reasonable amount of downside protection coupled with a reasonable amount of participation in the market’s upside. Though a few, which they named, do.

The point, here, is not to grade buy-write funds as a thumbs-up or a thumbs-down. Rather, Reditus Emptor Caveat—a twist on the old Latin proverb—is our cautionary advice to “Let the Income Buyer Beware,” and reflects our objective to dig into the subtleties of this rapidly growing corner of the fund universe. We hope this analysis better equips investors to make sound decisions as to whether a buy-write strategy deserves a spot in their portfolio mix. From our perspective, the following are the most important takeaways.

-

- Buy-write funds provide excellent current income but achieve that by selling away the upside for equities. This financial alchemy is not genius at work, just a simple conversion of capital gains into current income.

- Buy-write strategies are not a substitute for equities in a bull market and may not provide the growth component that stocks bring to a balanced portfolio. Nor are buy-write funds a proxy for fixed income as a defensive haven during bear markets.

- If these funds do not fill an equity or fixed income role, they must be evaluated as a distinctly different asset. How do investors decide if the skewed payoff is attractive? One simple test is to ask if you would be comfortable selling a naked put on the market. Because selling a naked put has the same return pattern as a covered call, if you are not at ease with the former, don’t let the eye candy of a 10% yield tempt you into the latter.

- BXM uses a straightforward at-the-money approach. Newer offerings include variations on the strategy such as: (a) only selling calls on a portion of the underlying portfolio; or (b) adjusting the “moneyness” of the calls based on volatility or a target level of desired yield, which influences the amount of the upside sold away and the premium earned. Given the importance of price appreciation in a portfolio’s equity sleeve, we are partial to both of those modifications. We encourage investors interested in the covered call strategy to look for a product incorporating such design tweaks to boost the chances of achieving the twin goals of income and growth. (Scott Opsal, “Reditus Emptor Caveat,” 8/28/2023)

The full report was produced for Leuthold’s institutional clients, but if you’d like a copy, the folks at Leuthold will give you access to the full report if you send an email to [email protected] and mention Mutual Fund Observer.

Buying the ARK Innovation bandwagon in blue-and-white

The one-star, $7.4 billion ARK Innovation ETF (ARKK) remains curiously attractive to investors and “journalists” who featured it in 102 articles in August 2023 alone (from “ARK Fund is dead money” to “Best 3 actively managed ETFs to buy now,” with lots and lots of breathless “did you see what bold and visionary thing Cathie Woods just did????” stories in between). Money continues to trickle in.

The one-star, $7.4 billion ARK Innovation ETF (ARKK) remains curiously attractive to investors and “journalists” who featured it in 102 articles in August 2023 alone (from “ARK Fund is dead money” to “Best 3 actively managed ETFs to buy now,” with lots and lots of breathless “did you see what bold and visionary thing Cathie Woods just did????” stories in between). Money continues to trickle in.

The fund trails 100% of its peers over the past month … but leads 98% so far this year … but trails 100% over the past three years. They’ve managed the feat by placing in the top 1-2% of funds in 2017, 2020, and 2023 (through August). And the bottom 1% of funds in 2021 and 2022. In its short life, it has posted single-year gains of 87% and 153% but also single-year losses of 23% and 67%.

Since inception, ARKK has outpaced the S&P 500 by 0.2% per year (11.9% versus 12.1%) …with double the volatility, hence half of the risk-adjusted returns.

If you’re an investor in ARKK today, what are the chances you’ve made money? Here’s a simple way of understanding the improbability of that. ARKK’s current NAV is the dashed line. If you bought ARKK only when it was lower than today – those little white spaces in 2018 and over the past year, you’re in the black. If you bought anywhere in the blue zone, you’ve lost. All purchases from 2019 through the middle of 2022 are losers.

Morningstar’s “investor returns” calculations suggest that ARKK investors have, on the whole, been killed by the fund. The returns seen by investors, who tended to buy high, trail the fund’s raw returns since inception by more than 30% (Why ARKK Shareholders Are Still Underwater, 6/5/2023).

Our recommendations remain the same and are embedded in all of MFO’s metrics: do not chase returns, do not invest in high-vol products, do not place more money at risk than you can afford to lose.

The Corporate Green Conundrum rolls on.

Vanguard joined BlackRock in Green Flight, in this case, from collapsing support for shareholder motions concerning ESG issues. At the same time, Biden’s landmark “Inflation Reduction Act” (IRA) has seen a huge upward revision in its impact on the federal deficit precisely because its provisions have seen unprecedented support from Corporate America.

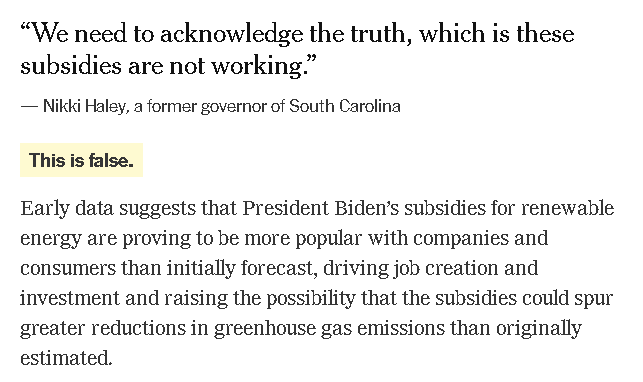

That became an issue in the first Republican “debate” when Nikki Haley claimed that the green incentives in the IRA had failed. She was quickly fact-checked.

Source: Fact-Checking the First Republican Debate, NYT.com, 8/23/2023

The IRA was initially scored as reducing long-term debt by $200 billion or so. It’s now seen as added more than a trillion to the debt, precisely because it’s corporate incentives are acting in exactly the way they were designed to.

Go green, Corporate America! Quickly. And, per our earlier note, concretely!

Morningstar named names.

Our final note is that Morningstar released a report that named which investment advisers took environmental issues seriously and which blew them off entirely. It is The Morningstar ESG Commitment Level: Our assessment of 108 asset managers (8/30/2023). Only eight advisors, in the US and overseas, stood out for the depth of their commitment:

Out of the 108 asset managers covered under the Morningstar ESG Commitment Level, we have awarded the highest honors to just eight. Robeco, Impax, Parnassus, Australian Ethical, Boston Trust Walden, Domini Asset Management, Affirmative Investment Management, and Stewart Investors all earn Morningstar ESG Commitment Levels of Leader.

The list of “not my problem” investors is far longer and includes American Century, Ariel, BNY Mellon, DFA, Dodge & Cox, Fidelity, GQG Partners, Janus Henderson, Schwab, Van Eck and Vanguard.

Bonus: Morningstar still favors EM investing

In an August analysis, they argue that Europe, banks, and emerging markets are the stock sectors with the highest forward-looking 10-year returns (3 Asset Classes That Still Hold Opportunities for Long-Term Investors, 8/16/2023). They foresee the broad US equity markets gaining 4.8% annually while banks, various European markets, and emerging markets exceed 10% per year.

Devesh checks in from vacation with a caution about TIPS

“Over the last four weeks, I have reduced my allocation to the 30-year TIPS bonds, and I am also a lot less sure about those bonds than I was at the start of the year. The reason for changing is rather simple. I thought I understood the bond market and waited long enough to buy at the right price.

But, observing price action over the past few months has made me realize that there is too much I don’t know. The biggest thing I am not sure about is how high yields can go and how low bonds can go. Is it credit risk, is it federal deficit magnitude, or is it the Fed not buying bonds like it used to? I cannot nail it down. Having realized this lack of conviction, I have switched about two-thirds of my TIPS position into short-dated T-bills.

- Rule number one: don’t lose money.

- Rule number two: never forget rule number one.”

Cheers from the beach, Devesh.

Rupal on the move

Rupal Bhansali is leaving Ariel to launch her own firm. We have no idea why, but it seems sudden. Ms. Bhansali stepped down as manager of Ariel Global and Ariel International on August 31. Between them, the funds have over $800 million in assets. Bhansali will remain as a consultant until February.

Rupal Bhansali is leaving Ariel to launch her own firm. We have no idea why, but it seems sudden. Ms. Bhansali stepped down as manager of Ariel Global and Ariel International on August 31. Between them, the funds have over $800 million in assets. Bhansali will remain as a consultant until February.

She will be succeeded by Henry Mallari-D’Auria, who joined the firm from AllianceBernstein in April, bringing along five associates. He was the head of emerging markets for Ariel until the announcement of Bhansali’s departure, at which point he became head of global and international equities for them. He was CIO for EM Equity Value to AllianceBernstein from 2002-2023.

Ariel Global is a four-star fund. Ariel International is vastly larger and has earned three stars. MFO Premium tracks Global against Lipper’s Global Multi-Cap Value peer group. Global has average returns (it trails the group by 0.2% APR) but substantially lower volatility and substantially higher risk-adjusted returns (Sharpe Ratio is 0.62 since inception versus the peer group’s 0.50). International tracks the International Large Core group, where it substantially trails its peers in returns, has substantially lower volatility, and comparable risk-adjusted performance.

Mr. Mallari-D’Auria ran a Europe-based EM hedge fund (Next 50) for AllianceBernstein. He manages two SMA strategies for Ariel (EM Value and EM ex-China Value). He also ran AB Emerging Markets Value Equity, which also appears to be a quarter-billion-dollar SMA strategy. That strategy earned three stars from Morningstar. Like the Ariel funds, it’s a value strategy that substantially trails its (non-value) peer group since inception. The gap is about 200 bps. But it’s not evident that he’s ever run a mutual fund before.

Rupal is a remarkable investor and thoughtful person. I’ve reached out to her via LinkedIn to see if she’ll chat in the month ahead about her plans.

Thanks, as ever …

To The Faithful Few, whose monthly contributions keep spirits up and the lights on, thanks and thanks and thanks again: S & F Investment Advisers, Wilson, Brian, Gregory, Doug, Stephen, David, William, and William. If you’d like to do your part to keep MFO up and running, please click on the “Support Us” link above or join the MFO Premium folks who, for just $120/year, get access to maestro Charles and some of the most advanced search tools available (or, at least, “available for less than the $16,000 that some others charge”).

Cheers!