Here's a statement of the obvious: The opinions expressed here are those of the participants, not those of the Mutual Fund Observer. We cannot vouch for the accuracy or appropriateness of any of it, though we do encourage civility and good humor.

Please don't enlighten the bond haters. They are needed to keep propelling yields lower, prices higher. What we don't need is a major shift in consensus that bond yields can only continue to go lower from here and for the bears to go into hibernation. Remember how entering January bond bearishness was rampant and near record levels. Every Tom, Dick, and Harry was calling for an inevitable and immediate rise in yields to 3.50% and then later in the year to 4.0%. We've seen how that has played out YTD so far. Conversely, entering January stock market optimism was by many measures at historic highs. And the result is that market hasn't exactly set the world on fire YTD.

12.84% of portf. in US Treasuries: DLFNX. Up +4.33 ytd. 5.97% of portf. in UST: DLTNX. Up +3.87 ytd.

I own DLFNX. I just thought to compare them.

MAINX is SHORTING USA 10-year notes. (labeled "CBT." What's that? Dated June, 2014. Callable Boot Trash? CBT?) But it's near the bottom of its holdings list. I asked about this earlier, and David got an answer from Fund Manager Teresa Kong which seemed to make sense.

I'll second that on Investor. He was a good guy. As for me, hopefully kinder and gentler. Then again, there's MJB to deal with so can't make any promises. Hope he is recovering nicely from his eye surgery.

@Crash ya looks like they are shorting the June 2014 10yr Treasury Bond Future. CBT just means that it's traded on the Chicago Board of Trade. Although the way they list it on their website is a little misleading because 30 futures really represent shorting 3mil worth (each contract represents $100,000). Morningstar translates it better (although their data is old).

@Charles, thanks I try, always love reading the monthly letters from the site and try to keep up on the board time permiting (as you can see my blog isn't updated as frequently as I would like either).

@heezsafe another aspect possibly being overlooked when people wonder where demand is going to come from for treasuries (besides the relative attractive valuation aspect) is increased demand by way of derivatives regulation...with trillions of over-the-counter derivatives being traded with little to no collateral, making more and more of that traded through a clearing house could cause HUGE demand for high quality assets, even with very minimal collateral requirements. This as well as the implementation of Basel III can represent a huge source of "regulated demand" that quite honestly I don't think enough people are taking into account.

The demand for Treasuries from outside primarily comes from central banks or sovereign funds holding dollar reserves. Much of this is in treasuries than actual dollar currency as people often assume. Assets at this level aren't looking for yield, just safety or preserving value over inflation in the best case. Holding them with (small) negative returns for this purpose is not uncommon. Since these bonds are often held to maturity, price fluctuations or marking to market is not a big issue for these buyers.

One can use the change in flows from this type of yield-insensitive demand to increase total returns as bond managers try to do. They are not buying Treasuries for the yield (unless we are talking about real returns in the 4%+ range).

This is important to know because the demand from funds exist only as long as there is a movement in prices and expectation of further price gains. Once, this flow induced movement stops, demand drops and people head for the exit.

It is a cyclic phenomena.

This discussion reminds me of the opposite euphoria at the beginning of the year when @Ted was making the case for the other side and I expect he will be doing so again sometime in the future.

Rather than take positions on bonds and equities like baseball fans choosing their teams and dissing the others, being diversified and staying so through these cycles is the best bet regardless of sentiment. Or one can be an active momentum trader to exploit these cycles without being jingoistic on either.

@WallStreetRanter re. derivatives. Oh, thanks alot; so much for last week's effort to re-normalize my sleep cycle! But, yeah, you're right. OTC + unseen rehypothecation .... still unresolved, the huge Known Unknown. It could significantly alter the equation, in ways unforeseeable. A very good reason to keep bond love measured, very measured.

But since you've raised the possibility, you probably are aware that Genstler resigned, after an exasperating 5-yr interagency squabble about who had authority to make rules to improve derivative transparency. As he left, the CFTC did so; and within days the shadow banking network called their Rep friends and the House voted a bill to rescind everything the CFTC had done. Do you know if that bill advanced? I'm clueless.

Rather than take positions on bonds and equities like baseball fans choosing their teams and dissing the others, being diversified and staying so through these cycles is the best bet regardless of sentiment.

So, like Bridgewaters' Pure Alpha and All Weather funds?

Rather than take positions on bonds and equities like baseball fans choosing their teams and dissing the others, being diversified and staying so through these cycles is the best bet regardless of sentiment.

So, like Bridgewaters' Pure Alpha and All Weather funds?

Doesn't that sound like a great name for high priced bottled water?

Just a simple diversified allocation into both bond and equity asset classes rather than try to guess or predict macro economic conditions or some other indicators. Don't need anything fancy.

Look at @old_skeet's portfolio (no, not the 50+ funds he owns). He always has an allocation up his "sleeve" to be happy about regardless of what is happening in the market. Put one good index or well managed fund in each such sleeve and you can be equally happy.

Cool. OK, so more simply like "The Ivy Portfolio" that Mebane Faber describes in his book by same title. The so-called generic absolute return portfolio of VTI, VEU, BND, VNQ, and DBC allocated evenly at 20% each. Something like that.

Rather than take positions on bonds and equities like baseball fans choosing their teams and dissing the others, being diversified and staying so through these cycles is the best bet regardless of sentiment.

Don't get me wrong, I'm not sitting here pounding the table to buy treasuries, I'm simply trying to tell what seems to be the completely ignored other side of the story. If anything, it simply speaks to what you are talking about, which is remaining diversified. I worry that with all bond flows going to these "unconstrained" funds, people are not getting properly diversified (yet believe they are). Instead they are doubling up on credit and exposing themselves to avoidable bad outcomes. Duration risk is just a time horizon issue, meanwhile improperly compensated credit risk is a real "money gone" issue (although sometimes made up for by being excessively compensated for the risk later on).

@Heezsafe I'm not sure of the specifics your discussing (other then Gensler resigning) but I do know derivatives regulation continues to move forward, in a morphing fashion, but forward nonetheless and increased collateral is a certainty. As far as how it is progressing? The most I know comes from the calendar

Cool. OK, so more simply like "The Ivy Portfolio" that Mebane Faber describes in his book by same title. The so-called generic absolute return portfolio of VTI, VEU, BND, VNQ, and DBC allocated evenly at 20% each. Something like that.

Yes, something like that though I prefer something more fine-grained than that in asset classes if using index funds (rather than actively managed allocation funds). The reason is that the broad index funds use a market cap based allocation for their sub classes that is usually not the oprimal allocation for best risk-adjusted returns. Or you can hand a category to a good active manager to do allocation as they see fit within that category.

You can also use the portfolio allocations from some of the online allocation tools. As long as they diversify broadly, they are all about the same for a given risk level in performance.

Don't get me wrong, I'm not sitting here pounding the table to buy treasuries, I'm simply trying to tell what seems to be the completely ignored other side of the story. If anything, it simply speaks to what you are talking about, which is remaining diversified. I worry that with all bond flows going to these "unconstrained" funds, people are not getting properly diversified (yet believe they are).

Makes sense. The last statement is a very good point. People lump all bonds into a single asset class to allocate to. But bond classes do differ widely in volatility and correlation with equities. @junkster's allocation seem, more often than not, correlated more with equities than bonds but he actively manages his allocation moving from one class to another so that works for him.

We do have to distinguish between portfolios designed for income and portfolios designed for growth. The current yield is very important to the former but total return is more relevant for the latter who can afford to sit diversified without worrying about yield.

The real problem with low yields in Treasuries for the people that need the income is the income stream shortfall even if they get the diversification benefits. Fed policies are hurting these people in the process of helping people that will benefit from economic growth. They have no choice but to chase yield at times even if at higher risk.

The real problem with low yields in Treasuries for the people that need the income is the income stream shortfall even if they get the diversification benefits.

Isn't an issue here also that if rates rise, US will owe that much more money on its government bonds? So, Fed will likely try to wait until sufficient growth offsets higher rates...while they hope (we hope) it happens.

If it doesn't, we are likely up the creek without a paddle .

>> [cman] Just a simple diversified allocation into both bond and equity asset classes rather than try to guess or predict macro economic conditions or some other indicators. Don't need anything fancy.

A month or three ago I believe I proposed going heavily into AOM / AOR / AOK, contrarily, since bonds were in such disfavor, and you poohpoohed it. I forget your reasoning, though I could look it up. Thoughts?

Isn't an issue here also that if rates rise, US will owe that much more money on its government bonds? So, Fed will likely try to wait until sufficient growth offsets higher rates...while they hope (we hope) it happens.

Whether it is an issue or not, fiscal policy is not the responsibility of the Fed. Separating the monetary policy from fiscal policy and keeping it away from commercial bankers and politicians is, after all, the main raison d'etre for central banks.

A month or three ago I believe I proposed going heavily into AOM / AOR / AOK, contrarily, since bonds were in such disfavor, and you poohpoohed it. I forget your reasoning, though I could look it up. Thoughts?

Please look it up.

I don't remember what you are referring to understand the context.

Staying fully diversified across all conditions in equities and bonds is opposed to a contrarian strategy for allocation. Contrarian investing is just the flip side of predicting the future in the opposite direction.

I find contrarian investing ill-defined as a strategy and considered as successful only in retrospect and forgotten when it doesn't work. I vaguely remember writing against contrarian reasoning per se. This has nothing to do with whether the strategy suggested investing in bonds or not. I don't know if this is what you are referring to.

It would be common courtesy if you set the context fully when you ask something of others and paraphrase something from the past.

You know, huffiness, smily or no, need not always be part of your cold-logic / contrary persona. Discourtesy indeed, to someone who simply has a memory for your interesting work. Sure, I will see if I can find the exact exchange and quote. I assumed your having such intellectual consistency as you attempt would permit you to know what you were going on about only a month or so ago. But let me check, yes.

You concluded by wondering if my query was not like that of someone who bet on all red in Vegas in order to be contrary, and that such was not worth discussing (of course it's not).

Perhaps 'poohpoohing' is unfair/inaccurate.

Fwiw, AOK is up 3% or something since this exchange approximately (not sure when it was). Some other agg bond holdings better, of course.

Early in your second answer to my query you repeated that 'A small bet in a big idea or a big bet in a small idea ... neither makes money,' the first part of which is complete nonsense and goes directly against the common notions of making layups and not jacking threes / going for singles and not homers.

This was in response to my suggestion that 'Contrarian would (for me in this situation) mean assuming most bad news is already baked into current pricing (bond indexes).' I had asked whether perhaps considering going into AOK would not be a good idea in Dec '13 with all the gloom spreading about bonds in general.

"Look at @old_skeet's portfolio (no, not the 50+ funds he owns). He always has an allocation up his "sleeve" to be happy about regardless of what is happening in the market. Put one good index or well managed fund in each such sleeve and you can be equally happy."

By my thinking ... perhaps so ... perhaps not as you will not have become as diverisfied as I have as you will not spread out your manager risk in the sleeves where there is no index fit. And, many of the funds that I own have a history of bettering their benchmarks. Read rule number nine in the below link.

Okay, it was the bottom of this, and from December, not only a few months ago; apologies for chron error: ... Perhaps 'poohpoohing' is unfair/inaccurate.

This is why it is important to discuss in context. Why would you expect me to remember one post from the past to and comment on some paraphrasing of it? That is being very rude in my books but your concept of rudeness in social conversation may vary.

That thread has already said what needs to be said in the context.

You seem to be looking for some kind of validation that your call to buy bonds on a contrarian bet was right. Sorry, it isn't. A well diversified portfolio has returned around 3-4% since then and would likely have done it even if bonds hadn't taken off. Would we be having this conversation in the latter case? For every contrarian bet, there is at least one that failed. You can't predict the future any more by being contrary than you can by not being so.

Early in your second answer to my query you repeated that 'A small bet in a big idea or a big bet in a small idea ... neither makes money,' the first part of which is complete nonsense and goes directly against the common notions of making layups and not jacking threes / going for singles and not homers.

This is an example of why taking things out of context is bad. That thread was in the context of a suggestion by Paul Merriman of going all in into stocks as a big idea.

Besides, the analogy is wrong. A small idea by itself doesn't get you much. A single base hit with no runner in scoring position won't get you anything over a home run by itself. You need to put together a sequence of small balls (or a combination with long) that leverage each other (not independent events) and that is often a bigger idea and more riskier to execute than going for homers and so can pay off big.

For example, if you had followed your own conviction and invested 10% on AOK, you would have made 0.3% or so from it based on your own reporting of returns. Small bet on a small idea. If that was all the idea.... A big bet on a big idea is what @junkster did, put his entire net worth into munis. That makes money. That saying is an alternative to the common sense observation that taking big risks makes money not small risks. The risk taken is a multiplier of the risk in the idea and the amount of bet you place on it.

Problem is diversification follows law of diminishing returns. So, there is such a thing as over-diversification. Where that line lies is open to debate, of course. But simplistic truisms like those rules don't contribute to that and will support any level of diversification.

The point, however, was to show the benefits of your diversification in multiple sleeves in different asset classes consistent with that rule as well.

Comments

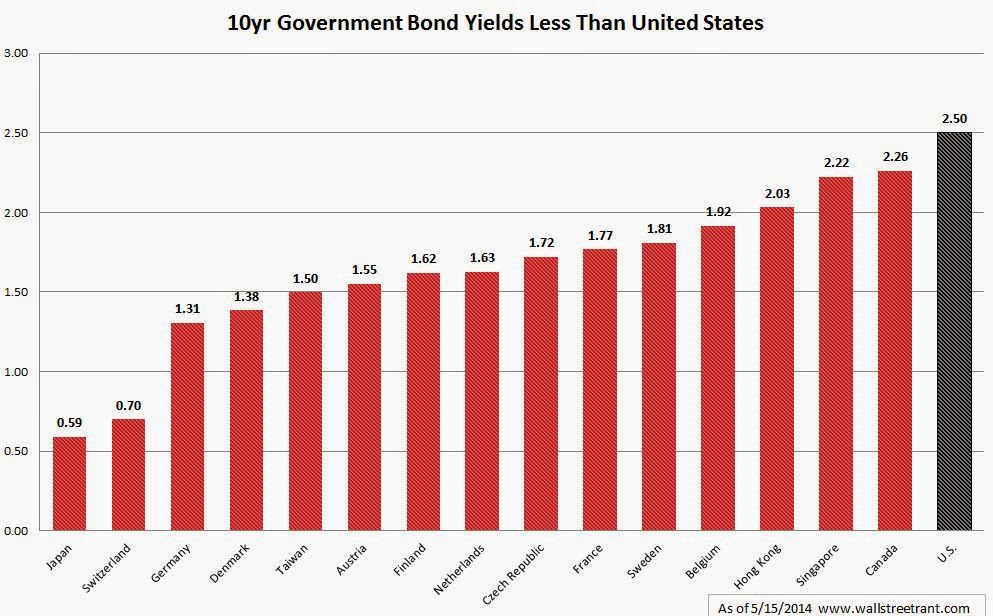

Below is a link to a hater of bonds.

http://blogs.barrons.com/incomeinvesting/2014/05/15/deutsche-bank-sees-swift-and-violent-treasury-yield-rise/?mod=BOL_hp_blog_ii

5.97% of portf. in UST: DLTNX. Up +3.87 ytd.

I own DLFNX. I just thought to compare them.

MAINX is SHORTING USA 10-year notes. (labeled "CBT." What's that? Dated June, 2014. Callable Boot Trash? CBT?) But it's near the bottom of its holdings list. I asked about this earlier, and David got an answer from Fund Manager Teresa Kong which seemed to make sense.

MAINX ytd: up +3.52%.

Cute.

Continue to suppress, central banksters, continue your race to the bottom.

Getting sweeter-er for bond love.

@Charles, thanks I try, always love reading the monthly letters from the site and try to keep up on the board time permiting (as you can see my blog isn't updated as frequently as I would like either).

@heezsafe another aspect possibly being overlooked when people wonder where demand is going to come from for treasuries (besides the relative attractive valuation aspect) is increased demand by way of derivatives regulation...with trillions of over-the-counter derivatives being traded with little to no collateral, making more and more of that traded through a clearing house could cause HUGE demand for high quality assets, even with very minimal collateral requirements. This as well as the implementation of Basel III can represent a huge source of "regulated demand" that quite honestly I don't think enough people are taking into account.

One can use the change in flows from this type of yield-insensitive demand to increase total returns as bond managers try to do. They are not buying Treasuries for the yield (unless we are talking about real returns in the 4%+ range).

This is important to know because the demand from funds exist only as long as there is a movement in prices and expectation of further price gains. Once, this flow induced movement stops, demand drops and people head for the exit.

It is a cyclic phenomena.

This discussion reminds me of the opposite euphoria at the beginning of the year when @Ted was making the case for the other side and I expect he will be doing so again sometime in the future.

Rather than take positions on bonds and equities like baseball fans choosing their teams and dissing the others, being diversified and staying so through these cycles is the best bet regardless of sentiment. Or one can be an active momentum trader to exploit these cycles without being jingoistic on either.

Oh, thanks alot; so much for last week's effort to re-normalize my sleep cycle!

But since you've raised the possibility, you probably are aware that Genstler resigned, after an exasperating 5-yr interagency squabble about who had authority to make rules to improve derivative transparency. As he left, the CFTC did so; and within days the shadow banking network called their Rep friends and the House voted a bill to rescind everything the CFTC had done. Do you know if that bill advanced? I'm clueless.

Just a simple diversified allocation into both bond and equity asset classes rather than try to guess or predict macro economic conditions or some other indicators. Don't need anything fancy.

Look at @old_skeet's portfolio (no, not the 50+ funds he owns). He always has an allocation up his "sleeve" to be happy about regardless of what is happening in the market. Put one good index or well managed fund in each such sleeve and you can be equally happy.

@Heezsafe I'm not sure of the specifics your discussing (other then Gensler resigning) but I do know derivatives regulation continues to move forward, in a morphing fashion, but forward nonetheless and increased collateral is a certainty. As far as how it is progressing? The most I know comes from the calendar

http://www2.isda.org/functional-areas/public-policy/otc-derivatives-compliance-calendar/

You can also use the portfolio allocations from some of the online allocation tools. As long as they diversify broadly, they are all about the same for a given risk level in performance.

We do have to distinguish between portfolios designed for income and portfolios designed for growth. The current yield is very important to the former but total return is more relevant for the latter who can afford to sit diversified without worrying about yield.

The real problem with low yields in Treasuries for the people that need the income is the income stream shortfall even if they get the diversification benefits. Fed policies are hurting these people in the process of helping people that will benefit from economic growth. They have no choice but to chase yield at times even if at higher risk.

If it doesn't, we are likely up the creek without a paddle

A month or three ago I believe I proposed going heavily into AOM / AOR / AOK, contrarily, since bonds were in such disfavor, and you poohpoohed it. I forget your reasoning, though I could look it up. Thoughts?

I don't remember what you are referring to understand the context.

Staying fully diversified across all conditions in equities and bonds is opposed to a contrarian strategy for allocation. Contrarian investing is just the flip side of predicting the future in the opposite direction.

I find contrarian investing ill-defined as a strategy and considered as successful only in retrospect and forgotten when it doesn't work. I vaguely remember writing against contrarian reasoning per se. This has nothing to do with whether the strategy suggested investing in bonds or not. I don't know if this is what you are referring to.

It would be common courtesy if you set the context fully when you ask something of others and paraphrase something from the past.

http://www.mutualfundobserver.com/discuss/discussion/comment/33099/#Comment_33099

You concluded by wondering if my query was not like that of someone who bet on all red in Vegas in order to be contrary, and that such was not worth discussing (of course it's not).

Perhaps 'poohpoohing' is unfair/inaccurate.

Fwiw, AOK is up 3% or something since this exchange approximately (not sure when it was). Some other agg bond holdings better, of course.

Early in your second answer to my query you repeated that 'A small bet in a big idea or a big bet in a small idea ... neither makes money,' the first part of which is complete nonsense and goes directly against the common notions of making layups and not jacking threes / going for singles and not homers.

This was in response to my suggestion that 'Contrarian would (for me in this situation) mean assuming most bad news is already baked into current pricing (bond indexes).' I had asked whether perhaps considering going into AOK would not be a good idea in Dec '13 with all the gloom spreading about bonds in general.

"Look at @old_skeet's portfolio (no, not the 50+ funds he owns). He always has an allocation up his "sleeve" to be happy about regardless of what is happening in the market. Put one good index or well managed fund in each such sleeve and you can be equally happy."

By my thinking ... perhaps so ... perhaps not as you will not have become as diverisfied as I have as you will not spread out your manager risk in the sleeves where there is no index fit. And, many of the funds that I own have a history of bettering their benchmarks. Read rule number nine in the below link.

http://www.dryassociates.com/16_rules.htm

I wish all ... "Good Investing."

Old_Skeet

That thread has already said what needs to be said in the context.

You seem to be looking for some kind of validation that your call to buy bonds on a contrarian bet was right. Sorry, it isn't. A well diversified portfolio has returned around 3-4% since then and would likely have done it even if bonds hadn't taken off. Would we be having this conversation in the latter case? For every contrarian bet, there is at least one that failed. You can't predict the future any more by being contrary than you can by not being so. This is an example of why taking things out of context is bad. That thread was in the context of a suggestion by Paul Merriman of going all in into stocks as a big idea.

Besides, the analogy is wrong. A small idea by itself doesn't get you much. A single base hit with no runner in scoring position won't get you anything over a home run by itself. You need to put together a sequence of small balls (or a combination with long) that leverage each other (not independent events) and that is often a bigger idea and more riskier to execute than going for homers and so can pay off big.

For example, if you had followed your own conviction and invested 10% on AOK, you would have made 0.3% or so from it based on your own reporting of returns. Small bet on a small idea. If that was all the idea.... A big bet on a big idea is what @junkster did, put his entire net worth into munis. That makes money. That saying is an alternative to the common sense observation that taking big risks makes money not small risks. The risk taken is a multiplier of the risk in the idea and the amount of bet you place on it.

The point, however, was to show the benefits of your diversification in multiple sleeves in different asset classes consistent with that rule as well.