All the developments that are worth knowing but aren’t worth separate stories, including 50 funds that just earned headstones rather than headlines. An absolute disaster? 10% of vanishing funds promising “absolute returns.” Wells Fargo promises that you can trust them, just before announcing millions of additional fines. Tadas moves up, a favorite fund closes quick and hard, Monrad celebrates his 58th and the Mathers Fund leaves this veil of tears after 53 eventful years.

Briefly Noted . . .

iShares has announced 2-for-1 share splits for three of its ETFs. The affected funds are

- iShares 1-3 Year Credit Bond ETF (CSJ)

- iShares Intermediate Credit Bond ETF (CIU)

- iShares U.S. Credit Bond ETF (CRED)

The record date for the stock splits will be August 3, 2018, and the stock splits will be effectuated after the close of trading on August 7, 2018.

The Ritholtz Empire grows. On June 26, 2018, Josh Brown (a/k/a The Reformed Broker) announced the hiring of Tadas Viskanta as the new director of investor education at Ritholtz Wealth Management. Tadas is the indefatigable proprietor of Abnormal Returns who, since 2005, has daily curated dozens of links on finance and on life. His proclaimed focus is being a “forecast-free investment blog,” which is to say AR is blessedly free of the endless din of self-serving, click-whoring speculation about whether a new Golden Age or a new Dark Age has been spawn by some act of corporate cupidity, fintech folly, robotic ascendance or druncle tweet. His curation strikes me as discerning but not dogmatic; he finds thoughtful content in unconventional places, and is as willing to offer an audience to a thoughtful blogger as to a Morningstar vice president. Tadas will continue to publish Abnormal Returns and profess finance at Butler University in Indianapolis.

The Ritholtz Empire grows. On June 26, 2018, Josh Brown (a/k/a The Reformed Broker) announced the hiring of Tadas Viskanta as the new director of investor education at Ritholtz Wealth Management. Tadas is the indefatigable proprietor of Abnormal Returns who, since 2005, has daily curated dozens of links on finance and on life. His proclaimed focus is being a “forecast-free investment blog,” which is to say AR is blessedly free of the endless din of self-serving, click-whoring speculation about whether a new Golden Age or a new Dark Age has been spawn by some act of corporate cupidity, fintech folly, robotic ascendance or druncle tweet. His curation strikes me as discerning but not dogmatic; he finds thoughtful content in unconventional places, and is as willing to offer an audience to a thoughtful blogger as to a Morningstar vice president. Tadas will continue to publish Abnormal Returns and profess finance at Butler University in Indianapolis.

Butler was, for a bit, the academic home of my predecessor as Director of Debate at Augustana. My teams and I spent a fair amount of time on Butler’s campus, primarily in Jordan Hall which seemed to be eternally under renovation.

The longest tenured fund manager. On June 1, 2018, Bruce Monrad of Northeast Investors Trust (NTHEX) celebrated his 58th year at the fund’s helm. His next-closest peer is Rupert H. Johnson of Franklin DynaTech (FKDNX) who is his 50th year with his fund. Their funds have one and five stars, respectively.

“Any publicity is good publicity”? Wells Fargo begins to wonder. In April 2018, federal regulators proposed $1 billion in fines against Wells Fargo for mortgage-lending and auto-insurance abuses.

In May 2018, scandal-ridden Wells Fargo trotted out a new ad campaign to reassure the public that “It’s a new day at Wells Fargo.”

In June 2018, the SEC fined Wells another $5.1 million because it “improperly pushed retail customers to actively trade complex investments in order to generate higher fees” (Reuters, 6/25/2018). It’s poor optics at the very least when the best you can say is, “well, the fines are getting much smaller!”

CBS News offered a nice summary of Wells’ travails.

SMALL WINS FOR INVESTORS

Brown Advisory Strategic Bond Fund (BATBX/BIABX) is trying an interesting game. The fund has three share classes, the most expensive of which is the Advisor class. Rather than reducing expenses on all three share classes, on July 1, 2018, Brown is going to (a) close the Advisor class and (b) move Advisor shareholders to the less expensive Investor share class and Investor shareholders to the still-less expensive Institutional share class. For reasons less clear, the Investor share class will adopt the ticker symbol from the closed Advisor shares (BATBX) and the Institutional share class will adopt the old Investor class ticker (BIABX).

CLOSINGS (and related inconveniences)

Columbia Diversified Real Return Fund (CDRAX) will close to new investors on July 27, 2018. No word about why or the fund’s future. That said, it has $1.7 million in assets, across all share classes, after four years of operation. (Cue funeral dirge.)

A typo notwithstanding, Oberweis International Opportunity Fund (OBIOX) and its Institutional clone were hard closed on June 7, 2018 (the typo in the filing stipulates 2017 for the closure date). There are only two small exceptions to the closure.

“Effective as of the date hereof” (a laughably inelegant phrase in place of which they might have said “as of June 27, 2018”), the Institutional Class shares of Royce Low-Priced Stock Fund (RYLPX) and Royce Small-Cap Value Fund (RYVFX) are closed to all purchases and exchanges.

OLD WINE, NEW BOTTLES

Effective August 6, 2018, The Arbitrage Credit Opportunities Fund (AGCAX) will change its name to the Water Island Credit Opportunities Fund. The Fund’s portfolio managers, investment objective and investment strategies will not change. Our guess is that the adviser felt that the fund’s current name as a bit too generic to attract investor attention; despite top-quartile returns over the past five years, the fund has drawn only $45 million in assets and has seen money trickling out the door.

Effective June 25, 2018, AT All Cap Growth Fund became CIBC Atlas All Cap Growth Fund (AWGIX) and AT Equity Income Fund was rechristened as CIBC Atlas Equity Income Fund (AWYIX). No changes in structure, fees or management were announced.

This all follows from the fact that AT Investment Advisers, Inc., the funds’ investment adviser, has changed its name to CIBC Private Wealth Advisors. For fans of initialisms, AT started as Atlantic Trust, adviser to the Atlantic Whitehall funds. CIBC signals Canadian Imperial Bank of Commerce, one of Canada’s Big Five banks.

CBOE Vest Defined Distribution Strategy Fund (VDDIX) is on its way to being the CBOE Vest Alternative Income Fund, at which point it will become an index fund tracking the CBOE S&P 500 Market-Neutral Volatility Risk Premia Optimized Index.

Effective June 4, 2018, the City National Rochdale Emerging Markets Fund (RIMIX) reorganized into the Fiera Capital Emerging Markets Fund.

Effective December 1, 2018, Fidelity MSCI Telecommunication Services Index ETF (FCOM) will be renamed Fidelity MSCI Communication Services Index ETF and its new benchmark will be the MSCI USA IMI Communication Services 25/50 Index.

A little less Laudus: The Board of Trustees of Laudus Trust has determined that it is in the best interests of each of the Laudus Mondrian International Equity Fund (LIEIX), Laudus Mondrian Emerging Markets Fund (LEMNX) and Laudus Mondrian International Government Fixed Income Fund (LIFNX) and their shareholders to ditch the “Laudus” moniker. The funds will become Mondrian International Equity Fund, Mondrian Emerging Markets Equity Fund, and Mondrian International Government Fixed Income Fund.

Effective September 30, 2018, Lord Abbett International Dividend Income Fund (LIDAX) becomes Lord Abbett International Value Fund and its benchmark changes from the MSCI All Country World Ex-U.S. High Dividend Yield Index to the MSCI EAFE Value Index.

Salient International Real Estate Fund (KIRYX) becomes Salient Global Real Estate Fund, with the predictable and necessary changes to its investment mandate, on August 14, 2018.

Many ETFs have recently chosen to highlight the identity of their sub-advisers in the fund’s name, so The Reasonable ETF might be renamed The Reasonable OMG It’s Peter Lynch! ETF. Effective as of June 29, 2018, Wisdom moved in the opposite direction by stripping out the names of their index providers from some ETFs.

| Prior to June 29, 2018 | Effective on June 29, 2018 |

| WisdomTree Barclays Yield Enhanced U.S. Aggregate Bond Fund | WisdomTree Yield Enhanced U.S. Aggregate Bond Fund |

| WisdomTree Barclays Yield Enhanced U.S. Short-Term Aggregate Bond Fund | WisdomTree Yield Enhanced U.S. Short-Term Aggregate Bond Fund |

| WisdomTree Barclays Interest Rate Hedged U.S. Aggregate Bond Fund | WisdomTree Interest Rate Hedged U.S. Aggregate Bond Fund |

| WisdomTree Barclays Negative Duration U.S. Aggregate Bond Fund | WisdomTree Negative Duration U.S. Aggregate Bond Fund |

| WisdomTree Bloomberg Floating Rate Treasury Fund | WisdomTree Floating Rate Treasury Fund |

OFF TO THE DUSTBIN OF HISTORY

AlphaClone International ETF (ALFI) liquidated on June 29, 2018. Hmmm … “alpha clone” sounds rather like a type of storm trooper (“the Sith are advancing, send a squad of the alpha clones”) from Star Wars.

AlphaCore Absolute Fund (GDABX) disappears on July 27, 2018. (Absolute minus one)

Avondale Core Investment Fund was promoted to glory on June 15, 2018 (hint: they refer to it as, the “Liquidation Date”).

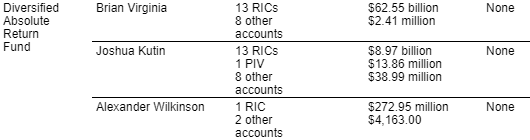

Columbia Diversified Absolute Return Fund (CDUAX) will close to new investors on July 27, 2018 and liquidate on September 7, 2018. The fund launched partway through 2015 and managed an absolute (negative) return in 2015, 2016 and so far in 2018. That presumably investors in the fund (who weren’t managers of it) and the managers of the fund (who weren’t investors in it), since the prospectus goal was to provide “absolute (positive) return.”

(Absolute minus two)

Despite posting returns in the top 1% of the multi-currency Morningstar peer group over the past decade, $41 million Columbia Absolute Return Currency and Income Fund (RARAX) will follow the same path: closed in July and really closed in September. (Absolute minus three)

Eaton Vance Multi-Strategy Absolute Return Fund (EADDX) is slated to merge into Eaton Vance Short Duration Strategic Income Fund (ETSIX) by October, 2018. Effective August 1, 2018, EADDX is closed to new investors. (Absolute minus four!)

The GAMCO Mathers Fund (MATRX) will be liquidated on or about August 31, 2018. Wow. It’s got that sort of “the last mastodon is dying” feel to it. Henry G. Van der Eb has been running this fund since the year I graduated from Wilkinsburg High School; that school was abandoned in 2016 after 106 years, victim of shrinking numbers, parlous finances and abysmal performance (the state department of education ranked it as Pennsylvania’s second-worst high school). Not that I’m suggesting parallels. The Mathers Fund launched in 1965 (no, no one named Mathers ever managed it) and become Gabelli Mathers in 1999. The fund’s goal was to make money in the long run “without excessive risk of capital loss.”

Hmmm … MATRX has posted “capital losses” over the past year, and three years, five years, ten years, twenty years and (wait for it) thirty years. For instance, over the past 10 years, MATRX would have transformed $10,000 to $4,600. Over 20 years, $10,000 would have shrunk to $4,800. A 30 year holding period would have transformed $10,000 to $6,900. Here’s the good news: if you’d bought the fund at inception in 1965 and sold June of 1981, you’d have been dancing in the street; $10,000 grew to $112,000 because of, rather than despite, the financial mess of the 1970s and early 1980s. At its peak, the fund held over a half billion in assets. Today, the remnant is $7.5 million.

The fund’s fortunes turned in 1981 because of two epochal moves: the highest interest rates and largest tax cuts in American history collided. The country spun into recession, inflation fell dramatically, and the economy rebounded quickly. Returns quickly flattened then turned negative. The titan that always and everywhere saw signs of financial ruin was undone by decades of relative prosperity.

In the fund’s defense, you could note that it’s the top performer in Morningstar’s bear market category which would be more compelling if it was a bear market fund, in the sense of being a tactical, trading vehicle for shorting the market. It, so far as I can tell, wasn’t.

You sensed Mr. Van der Eb’s exhaustion in the fund’s final annual report (12/30/2017), which eschewed talking about the fund’s present or future and focused instead on its single bright spot this century:

The Fund completed 52 years of operation during 2017 and since inception through December 31, 2017 its average annual total return was 5.84% versus 10.01% for its benchmark S&P 500 Index. During the 2008-09 credit crisis, the Fund’s risk averse position preserved capital and outperformed the S&P 500 for the two, three, five, and ten year periods ended December 31, 2009. The Fund had positive returns for the one, two, three, five, and ten year periods ended December 31, 2008 versus the S&P 500, which had negative returns for each of those periods.

IQ Hedge Multi-Strategy Plus Fund (IQHOX) will be liquidated on or about August 7, 2018. As part of the larger “falling out of love with liquid alts,” IQHOX had a solidly above average record since inception but it’s expensive, high minimum, and assets have been dribbling away for years.

iShares has resolved to cull the hedged and multifactor herd. The following ETFs are set to be liquidated on August 22, 2018:

- iShares Currency Hedged MSCI Europe Small-Cap ETF (HEUS),

- iShares Edge MSCI Min Vol EAFE Currency Hedged ETF (HEFV),

- iShares Edge MSCI Min Vol EM Currency Hedged ETF (HEMV),

- iShares Edge MSCI Min Vol Europe Currency Hedged ETF (HEUV),

- iShares Edge MSCI Min Vol Global Currency Hedged ETF (HACV),

- iShares Edge MSCI Multifactor Consumer Discretionary ETF (CNDF),

- iShares Edge MSCI Multifactor Consumer Staples ETF (CNSF),

- iShares Edge MSCI Multifactor Energy ETF (ERGF),

- iShares Edge MSCI Multifactor Financials ETF (FNCF),

- iShares Edge MSCI Multifactor Healthcare ETF (HCRF),

- iShares Edge MSCI Multifactor Industrials ETF (INDF),

- iShares Edge MSCI Multifactor Materials ETF (MATF),

- iShares Edge MSCI Multifactor Technology ETF (TCHF) and

- iShares Edge MSCI Multifactor Utilities ETF (UTLF).

Janus Henderson All Asset Fund (HGAAX) will liquidate and, just to be sure, terminate on or about December 31, 2018.

The Board of Trustees for John Hancock Natural Resources Fund (JINRX) has announced that “as of the close of business on or about October 19, 2018, there are not expected to be any shareholders in the fund, and the fund will be liquidated.” Unbidden, Carew388, one of the discussion board members, volunteers that “this fund won’t be missed.” That might be driven by the observation that over the past decade, JINRX turned $10,000 into $5,200, rather worse than 90% of its peers.

The shareholders of Lord Abbett Multi-Asset Focused Growth Fund (LDSFX) voted to merge their fund into Lord Abbett Multi-Asset Growth Fund LWSAX) which should be completed as of the close of business on July 13, 2018.

Loomis Sayles Dividend Income Fund (LSCAX) and Loomis Sayles Value Fund (LSVRX, which Morningstar designates as a “bronze medalist”) will liquidate on or about August 30, 2018. While Morningstar believes that “a consistent, low-turnover strategy, reasonable fees, and an experienced management team outweigh concerns about Loomis Sayles Value’s recent underperformance and outflows,” Loomis seems to have reached the opposite conclusion.

MainStay Absolute Return Multi-Strategy Fund (MSANX) celebrated its third anniversary by announcing its impending liquidation, on November 16, 2018. (Yikes, absolute minus five!)

Following “a strategic review of the management and operations of the Fund,” The Momentum Bond Fund (MOMBX) – yes, “The” was part of the formal name – liquidated on June 29, 2018. The “strategic review” might well have ended with (a) we’re expensive, (b) we have only $5 million in assets and (c) our performance looks like this:

Morgan Stanley’s Active Assets Government Trust (AISXX) will become noticeably less active after August 13, 2018.

On June 13, 2018, Nationwide Mutual Funds board of trustees voted to liquidate the Nationwide National Intermediate Tax Free Bond Fund (NWJOX) and the Nationwide Ziegler Wisconsin Tax Exempt Fund (NWJWX) two weeks hence. Just in case you were wondering, the board then offered up a bit of investing insight: “Because of the pending liquidations, neither Fund now represents a long-term investment solution.”

Oppenheimer Global Real Estate Fund (OGRAX), a perfectly respectable performer with about $50 million in assets, will be liquidated on or about August 24, 2018.

Rex Gold Hedged S&P 500 ETF ceased operations and liquidated on June 22, 2018.

Salient Adaptive Balanced Fund (AOGAX), Adaptive Income Fund (AILAX), Adaptive US Equity Fund (ACSIX), Adaptive Growth Fund (SRPAX), Trend Fund (SPTAX), EM Infrastructure Fund (KGIAX), International Dividend Signal Fund (FFDAX), Real Estate Fund (KREAX), Select Opportunity Fund (FSONX), and US Dividend Signal Fund (FDYAX) all become rather less salient on or around August 13, 2018.

On the next day, Salient International Real Estate gets a new name and mission. And on the day after that, Salient Tactical Real Estate Fund (KSRAX) will merge into Salient International Real Estate Fund (KIRAX).

Spirited Funds/ETFMG Whiskey & Spirits ETF (WSKY) took its final sip from the bottle on June 15, 2018.

VanEck Vectors EM Investment Grade + BB Rated USD Sovereign Bond ETF (IGEM) will close at the end of July and liquidate on August 7, 2018. One wonders if part of the problem was baked in at the fund’s inception. Its benchmark index (“the EM Investment Grade Index”) seems like it would invest in, oh, investment grade securities but in reality “includes both investment grade and below investment grade rated securities.” The fund also invested in unregistered (Regulation S) and illiquid private (rule 144A) securities which were hard enough to trade that the fund had to rely on a sampling strategy to approximate the performance of the index.

USAA Flexible Income Fund (USFIX), USAA Real Return Fund (USRRX), and USAA Total Return Strategy Fund (USTRX) are each slated for liquidation on August 17, 2018.