Each month we share developments in the industry that are, individually, to minor to warrant their own story. Since about three-quarters of it are stories of failure and the subsequent thrashing about, it mostly gets downplayed. This month saw, in particular, the liquidation of a lot of funds that were trying to deal with a low-interest rate, high stock valuation world: their names invoke global allocations and global bonds, alternative and unconstrained income, flexible opportunities and the occasional quantamental bent.

SMALL WINS FOR INVESTORS

A handful of funds reduced their advisory fees and/or expense ratio caps this month, often enough from “extortionate” down to “exorbitant.” They shall go nameless but they do bring to mind an interesting rule of thumb: if your portfolio’s expense ratio is greater than your weight, panic.

AMG SouthernSun U.S. Equity Fund (SSEFX) and AMG GW&K Enhanced Core Bond Fund (MFDAX) will convert their “C” shares to “N” shares on May 31, 2019. How much difference does that make? Well, shareholders in SouthernSun’s “C” class will see their e.r. drop from 1.96% to 1.21%. “C” shares have, from the get-go, been one of the industry’s worst ideas; they were advertised as a no-load way to access load-bearing funds, which was great as long as you could rationalize their universally exorbitant fees. I celebrate their death.

AMG Managers Montag & Caldwell Growth Fund (MCGFX) will convert their “R” shares to “N” shares on the same date. That’s a price reduction of about 30 bps for investors.

Effective immediately, the AQR Diversified Arbitrage Fund, AQR Equity Market Neutral Fund, AQR Long-Short Equity Fund and AQR Multi-Strategy Alternative Fund are no longer closed to new investors. The folks on the MFO Discussion Board were … uhh, not leaping for their checkbooks.

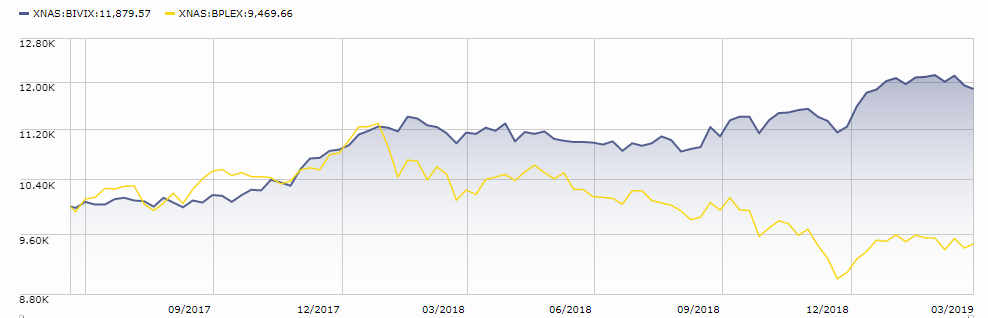

Boston Partners Long/Short Equity Fund (BPLEX) has reopened to new investors, though the adviser “has discretion to close the Fund in the future should the assets of the Fund increase by more than 5% from the date of the reopening of the Fund.” BPLEX saw hundreds of millions in outflows over the past 12 months as performance continued to flounder, while the Boston Partners complex saw outflows of $2.3 billion. After crushing the competition for years, BPLEX now has a five year record that trails 75% of its peers, with high volatility and high expenses (3.26%). I’d want to be very comfortable about my understanding of the firm’s recent travails before committing funds to it.

Fans of the fund might look a bit at Balter Invenomic (BIVIX), a long/short fund run by Ali Motamed, a former BPLEX manager. The difference in performance is pretty stark and charges a bit less than does BPLEX.

CLOSINGS (and related inconveniences)

On or about April 29, 2019, the Investor share class of Litman Gregory Masters Equity Fund (MSENX) and the Litman Gregory Masters International Fund (MNILX) will be terminated. Folks holding Investor Shares will be rolled into Institutional Class shares and, going forward, the investment minimum for institutional shares will drop to $10,000, with the minimum in for retirement accounts dropping to $1,000.

OLD WINE IN NEW BOTTLES

On June 9, 2019, the Dreyfus name will disappear from the investing world. On that date, the phrase “BNY Mellon” will substitute for the word “Dreyfus” in the name of each fund. Dreyfus has seen five consecutive years of near-continuous outflows and the name holds little brand value anymore.

Frontier Timpani Small Cap Growth Fund (FTSCX) will soon become a Calamos fund, following Calamos’ decision to buy the fund’s adviser.

On May 7, 2019, Highland Premier Growth Equity Fund (HPEAX) becomes Highland Socially Responsible Equity Fund with the predictable revisions of the investment strategy. Morningstar currently rates the fund as having a “below average” sustainability rating, despite qualifying as an ESG fund.

OFF TO THE DUSTBIN OF HISTORY

Advisorshares Madrona International ETF, AdvisorShares Madrona Domestic ETF, AdvisorShares Madrona Global Bond ETF and AdvisorShares Madrona International ETF were all liquidated on March 29, 2019.

Altrius Enhanced Income Fund (KEUAX), RAISE™ Core Tactical Fund (KRCAX) and MarketGrader 100 Enhanced Fund (KHMAX) all vanished simultaneously on March 30, 2019.

Barrow Value Opportunity Fund (BALIX) will discontinue its operations effective April 3, 2019. It’s an entirely respectable fund that gained absolutely no market traction.

CLS International Equity Fund (INTFX) has closed and will liquidate on Tax Day, April 15, 2019.

CRM Large Cap Opportunity Fund will merge with and into CRM All Cap Value Fund (CRMEX) sometime in the second quarter of 2019.

Diamond Hill Financial Long-Short Fund (BANCX) will merge into Diamond Research Opportunities Fund (DHROX) on or about June 7, 2019. Over the past 3, 5, and 10 years, BANCX has substantially outperformed its surviving sibling, though at least investors will receive a modest cost reduction after the change.

Dreyfus Unconstrained Bond Fund (DSTAX, formerly Opportunistic Income) will be liquidated on or about April 29, 2019.

Driehaus Frontier Emerging Markets Fund (DRFRX) has closed and will liquidate as soon as that can be practicably arranged; the advisor currently expects that to be April 29, 2019. The fund is modestly underwater since inception; $10,000 on Day One will have become $9,800 now.

Dunham Alternative Dividend Fund (DNDHX), likewise underwater since inception, will be liquidated on or about April 30, 2019

GALF eats FARF: Federated Global Allocation Fund (FGALF to use Federated’s abbreviation) is slated to consume Federated Absolute Return Fund (FARF) assuming shareholder approval at a special meeting currently scheduled for April 25, 2019.

Franklin California Ultra-Short Tax-Free Fund (FKTFX) will disappear on July 12, 2019.

Hartford Schroders Global Strategic Bond Fund (SGBVX), which returned $15 on a $10,000 investment of the past five years, will be liquidated on or before April 30, 2019.

The Iron Equity Premium Income Fund was liquidated on March 26, 2019.

Janus Henderson All Asset Fund (HGAAX) was supposed to be liquidated on December 31, 2018 but received a stay of execution until March 22, 2019. For reasons unstated, the Board issued another stay until June 25, 2019. Not to be blunt, but the fund has seen five months of inflows in five years and trailed between 70-90% of its peers, depending on which trailing period you examine. It’s not entirely clear whose interest is served by delaying its departure.

Neiman Balanced Allocation Fund (NBAFX) was liquidated on March 29, 2019.

Nile Africa, Frontier and Emerging Fund (NAFAX) was liquidated on March 28, 2019, after quite short notice.

Putman Global Sector Fund (PPGAX) will merge into Putnam Global Equity Fund (PEQUX) following shareholder approval. The vote is in early April, the merger shortly thereafter.

RQSI Small/Mid Cap Hedged Equity Fund (RQSAX) will cease operations and liquidate on or about April 5, 2019.

Steben Select Multi-Strategy Fund liquidated on March 30, 2019 though it will reportedly take a month or more for investors to receive their checks.

Stringer Moderate Growth Fund (SRQAX) become moderately unstrung on March 29, 2019.

The one-star record of Transamerica Multi-Cap Growth (ITSAX) will disappear as it merges into Transamerica US Growth (TADAX) on May 31, 2019.

USA Mutuals/WaveFront Hedged Quantamental Opportunities Fund (QUANX) was liquidated on March 29, 2019. If only its departure would also strike the word “quantamental” from our collective consciousness, but that regrettable term has too many fans now.

On or about April 26, 2019, Virtus Newfleet CA Tax-Exempt Bond Fund (CTESX) will be liquidated.

Voya CBRE Long/Short Fund (VCRLX) will be liquidated on or about June 7, 2019.