Updates

Three advisers are vying for this month’s “they’re doing what? Did I read this right?” award for moves where we were, literally, reading the filings aloud, slowly, to be sure we weren’t missing something.

Nominee #1 BlackRock

BlackRock Focus Growth (MAFOX) will undergo “a reorganization with another BlackRock-advised fund” in the fourth quarter of 2019. In the reorganization, the $1 billion, five-star BlackRock Large Cap Focus Growth (MALHX) “will be reorganized into” the $200 million, four star Focus Growth fund. Okay, though on face weird: the smaller, weaker fund “acquires” the bigger, stronger one. And, immediately thereafter, the surviving fund adopts the name of the deceased one: BlackRock Large Cap Focus Growth. Wouldn’t that cause BlackRock to lose the five-star record? Why not simply merge Focus Growth into Large Cap Focus Growth if, in the end, you wanted a fund named Large Cap Focus Growth?

Nominee #2: Eaton Vance

August 9, 2019: The Board of Trustees of Eaton Vance Mutual Funds Trust, on behalf of Eaton Vance Global Bond Fund (EGBIX), has approved the liquidation of the Fund, which is expected to take place on or about September 9, 2019. So Eaton Vance gets out of the global bond business after only nine months in the global bond business.

For a month.

Effective October 14, 2019, Eaton Vance Diversified Currency Income Fund (EAIIX) will change its name to Eaton Vance Global Bond Fund, at which point it will commit to investing in … well, global bonds.

Nominee #3 Guggenheim

On November 11, 2019, Guggenheim Mid Cap Value Institutional Fund (SVUIX) will (1) become Guggenheim SMid Cap Value Institutional Fund and (2) immediately merge into Guggenheim Mid Cap Value (SEVAX), Institutional share class (SVUIX) which itself changes its name to Guggenheim SMid Cap Value that same day. So, for a period of time so short that it exists only in quantum physics, holders of MCVI become holders of SCVI before becoming holders of MCV(I) which might or might not have completed the metamorphosis into SCV(I).

To be clear, these moves are perfectly legal and probably make perfect sense to those who came up with the idea – they’re simply perplexing to us mere mortals.

Briefly Noted . . .

SMALL WINS FOR INVESTORS

Aberdeen Emerging Markets Fund (GEGAX) has reopened. Morningstar rather likes the fund, but less so now (Bronze) than before some management and strategy turmoil (Silver).

American Beacon Stephens Small Cap Growth Fund (STSGX) has reduced its expense ratio by a bit. Investor shares, for example, just dropped 7 bps. Why 7? Not sure, but that might move it from Morningstar’s “high” to “above average” expense band. Woohoo!

AMG Managers CenterSquare Real Estate Fund, AMG Managers Amundi Short Duration Government Fund, AMG Managers Fairpointe Mid Cap Fund and AMG Managers Montag & Caldwell Growth Fund (MCGFX) have all posted expense reductions. MCGFX has reduced its expense ratio from 1.17% to 0.92%. Nice gesture. The fact that Ron Canarkis left in January 2019 after a quarter century as manager requires a bit on introspection on the part of prospective investors.

Effective September 1, 2019, AQR Style Premia Alternative Fund (QSPIX) and AQR Style Premia Alternative LV Fund (QSLNX) are no longer closed to new investors.

Effective immediately, the minimum initial investment amount for Cove Street Capital Small Cap Value Fund (CSCAX) has been lowered from $10,000 to $2,500. Exceptionally solid early in the decade, respectable in its second half, high sustainability score, high active share, low vol.

Crawford Dividend Opportunity (CDOFX) is a five-star small cap fund with below-average expense ratio. On September 1, the cap on their expenses fell another 6 points to 99 bps for the no-load shares. As with Cove Street, there’s a lot to like here: high sustainability score, very high active share, much higher-than-average quality portfolio for a small cap fund, and admirably low risk scores.

Effective October 31, 2019, the 2% redemption fee on Federated International Small-Mid Company Fund (ISCAX) will be eliminated. Redemption fees generally function to discourage “hot money” traders. It appears the fund has seen net inflows in six months over the past six years, which implies that hasn’t really been an issue.

The $37 billion, five-star Vanguard Dividend Growth Fund (VDIGX) is now open to all new investors.

The minimum investment amount required to open and maintain a fund account for Vanguard Market Neutral Fund (VMNFX) will be reduced from $250,000 to $50,000 on or about November 4, 2019.

CLOSINGS (and related inconveniences)

The $10 billion Invesco High Yield Municipal Fund (ACTHX) will close to new investors on September 6, 2019.

OLD WINE, NEW BOTTLES

On or about November 15, 2019 Aberdeen Global Unconstrained Fixed Income Fund (CUGAX, formerly Aberdeen Global Fixed Income) will be rechristened Aberdeen Global Absolute Return Strategies Fund with attendant shifts in the investment strategy.

Balter European L/S Small Cap Fund (BESRX) is slated to become F/m Investments European L/S Small Cap Fund. The adviser changes from Balter to F/m, but the sub-adviser (i.e., the manager) remains the same.

Effective November 27, 2019, Federated Mortgage Fund (FGFSX) becomes Federated Select Total Return Bond Fund. The name change is accompanied by a 16 bps drop in the expense ratio and a broader portfolio; mortgage-backed securities drop to about 50% of the portfolio from its primary component.

Effective on or about November 8, 2019, the Hartford Environmental Opportunities Fund (HEOMX) will be renamed as the Hartford Climate Opportunities Fund.

M.D. Sass Short Term U.S. Government Agency Income Fund (MDSHX) becomes the Integrity Short Term Government Fund sometime in the near future. Likewise M.D. Sass Equity Income Plus Fund (MDEPX) will become Integrity Dividend Harvest Fund.

Effective January 1, 2020, T. Rowe Price Personal Strategy Income Fund (PRSIX) will be renamed T. Rowe Price Spectrum Conservative Allocation Fund, while Personal Strategy Growth (TRSGX) becomes Spectrum Moderate Growth Allocation and Personal Strategy Balanced (TRPBX) is rechristened Spectrum Moderate Allocation.

OFF TO THE DUSTBIN OF HISTORY

AGF Global Equity Fund (AGXIX) will be liquidated on September 19, 2019.

AlphaOne NextGen Technology Fund (AONAX) sort of becomes a LastGen fund on September 30, 2019.

AlphaOne Small Cap Opportunities Fund (AOMAX) preceded it, having been liquidated on August 30, 2019.

Alpha Risk Tactical Rotation Fund was liquidated on August 23, 2019.

American Independence Global Tactical Allocation Fund (AARMX) will liquidate on September 12, 2019. That follows the earlier decision of the fund’s investment adviser, Manifold Partners, to withdraw from managing the portfolio. The board of trustees likely noticed two facts: that (1) it’s a four star fund with (2) no assets. Removing the managers who generated the performance left them with just the “no assets” part, and so …

BlackRock Energy & Resources Portfolio (SSGRX) will merge into BlackRock All-Cap Energy & Resources Portfolio (BACAX) at some point in the first quarter of 2020. Both funds are under $100 million AUM and the All-Cap fund has a better track record and slightly lower expenses.

On December 13, 2019, BNY Mellon Growth & Income Fund (DGRIX) will merge into Nationwide Dynamic U.S. Growth Fund (NMFAX). At the same time, BNY Mellon Disciplined Stock Fund (DDSTX) will be consumed by a newly-launched Nationwide Mellon Disciplined Value Fund.

City National Rochdale High Yield Bond Fund (CHBAX) will be liquidated on or about September 30, 2019

CrossingBridge Long/Short Credit Fund (CLCAX), formerly Collins Long/Short Credit, will be liquidated on September 6, 2019. The adviser explained that while the fund was still profitable, it had minimal upside and wasn’t delivering the downside protection now that it excelled at in the 2008 meltdown. The closure leaves Cohanzick, the manager, with three funds: ultra-short (RPHIX), short (CBIDX) and not-necessarily-so-short (RSIVX).

The Board of Trustees of the StrongVest ETF Trust authorized an orderly liquidation of the CWA Income ETF (CWAI), September 12, 2019. I appreciate the orderliness, though “StrongVest” sounds a lot like a character out of Lord of the Rings.

Destra Wolverine Dynamic Asset Fund (DWAAX) will perish heroically on September 15, 2019 after a climactic struggle with Sabretooth and a mediocre performance record that failed to inspire a fraction of the devotion that Wolverine himself did.

Destra Wolverine Dynamic Asset Fund (DWAAX) will perish heroically on September 15, 2019 after a climactic struggle with Sabretooth and a mediocre performance record that failed to inspire a fraction of the devotion that Wolverine himself did.

Goldman Sachs Absolute Return Multi-Asset Fund (GARDX) – having lost money in two of the four years of its existence, which is hardly in the spirit of “absolute return” – will be liquidated on October 15, 2019.

Harbor Funds’ Board of Trustees has determined to liquidate and dissolve the Harbor Real Return Fund (HARRX) and Harbor Target Retirement 2015 Fund (HARGX). The liquidations are expected to occur on October 30, 2019.

The one-star, $128 million Hartford International Small Company Fund (HNSAX) is merging into the unrated, $44 million Hartford Global Impact Fund (HGXAX) on or about November 22, 2019.

At the recommendation of Meritage Capital, the fund’s adviser, Insignia Macro Fund (IGMLX) will be liquidated on September 9, 2019. The fund misplaced this year’s boisterous market; its -4% return trails its peer group by 14% after leading them by 9% last year.

iShares 10+ Year Investment Grade Corporate Bond ETF (LLQD), iShares 5-10 Year Investment Grade Corporate Bond ETF (MLQD), iShares Adaptive Currency Hedged MSCI Eurozone ETF (DEZU), iShares Adaptive Currency Hedged MSCI Japan ETF (DEWJ) and iShares Edge MSCI Min Vol Asia ex Japan ETF (AXJV) were all liquidated on August 26, 2019.

Manning & Napier Equity Income (MNESX), Income (MSMSX) and International (EXITX) will all be liquidated on November 20, 2019. Very different paths to the same grave: Equity Income is relatively good (top third over five years) but unpopular, Income is great (top 10% over five years) but unpopular, and International … well, sort of earned its EXIT ticker symbol but was relatively popular ($318 million) nonetheless.

RiverFront Asset Allocation Income & Growth (RLIIX) and RiverFront Asset Allocation Growth (RMGAX) will merge into RiverFront Asset Allocation Moderate (RMIAX) and RiverFront Asset Allocation Growth & Income (RCCAX), respectively, on or about September 9, 2019.

The four-star SEI Long/Short Alternative Fund (SNAAX) will, in recognition of “low asset levels due to limited distribution and [the prospect] that there was no expectation of significant future asset growth,” be liquidated on September 27, 2019.

Stone Ridge U.S. Small Cap Variance Risk Premium Fund (VRSMX) and Stone Ridge International Developed Markets Variance Risk Premium Fund (VRMFX) will both be merged into Stone Ridge U.S. Large Cap Variance Risk Premium Fund (VRLIX) on or about October 28, 2019.

STAAR Disciplined Strategies Fund (SITAX, formerly STAAR Alternative Categories Fund), STAAR General Bond Fund (SITGX), STAAR International Fund (Ticker: SITIX), STAAR Dynamic Capital Fund (SITLX, formerly STAAR Larger Company Stock Fund), STAAR Short Term Bond Fund (SITBX) and STAAR Adaptive Discovery Fund (SITSX, formerly STAAR Smaller Company Stock Fund) will all become “formerly funds” on September 24, 2019.

T. Rowe Price has an odd step-up that is not unusual for the industry: it will offer the same strategy as both a pure institutional fund and a retail fund with institutional share class. In November 2019, they’re unwinding some of the silliness by moving shareholders from a liquidating institutional fund into institutional shares of the fund’s retail version.

| Liquidating Institutional Funds | Acquiring Retail Funds | Expected Closing Date |

| T. Rowe Price Institutional U.S. Structured Research Fund | T. Rowe Price U.S. Equity Research Fund (prior to July 1, 2019, named the T. Rowe Price Capital Opportunity Fund) | November 25, 2019 |

| T. Rowe Price Institutional Global Focused Growth Equity Fund | T. Rowe Price Global Stock Fund | November 25, 2019 |

| T. Rowe Price Institutional Global Growth Equity Fund | T. Rowe Price Global Growth Stock Fund | November 18, 2019 |

Each reorganization is expected to be consummated on or about the date indicated. WBI is doing a two-step with four of their ETFs. Step 1 is merging, Step 2 is renaming the merged entity. In each case, the “1000,” which referred to the Russell 1000 Value benchmark is being replaced with “3000,” as in Russell 3000 Value. Herewith, what you’ll need to know as of October 25, 2019:

| Acquired Fund | Acquiring Fund (New Name) | Acquiring Fund (Current Name) |

| WBI BullBear Rising Income 2000 ETF (WBIA) | WBI BullBear Rising Income 3000 ETF (WBIE) | WBI BullBear Rising Income 1000 ETF |

| WBI BullBear Value 2000 ETF (WBIB) | WBI BullBear Value 3000 ETF (WBIF) | WBI BullBear Value 1000 ETF |

| WBI BullBear Yield 2000 ETF (WBIC) | WBI BullBear Yield 3000 ETF (WBIG) | WBI BullBear Yield 1000 ETF |

| WBI BullBear Quality 2000 ETF (WBID) | WBI BullBear Quality 3000 ETF (WBIL) | WBI BullBear Quality 1000 ETF |

Westwood SMidCap Plus Fund (WHGPX) will be liquidated on September 30, 2019.

Remember Sisyphus? Woven into the Iliad and the Odyssey but brought to life for many college-educated folks of a certain generation by Albert Camus, The Myth of Sisyphus (1942). King of Corinth. By all accounts, pretty much a bastard. But, also, by all accounts, the smartest and trickiest guy ever. Got a reputation for being able to trick the gods of Olympus. That was jolly in the short term, hellacious in the long term (by which I mean “for all eternity”). Zeus sentenced him to an eternity in Hades, with the sole hope that if he could roll a boulder to the top of a hill, he could get out. Or not: enchanted boulder that always slipped from his grasp a foot from the top and rolled all the way back down.

Remember Sisyphus? Woven into the Iliad and the Odyssey but brought to life for many college-educated folks of a certain generation by Albert Camus, The Myth of Sisyphus (1942). King of Corinth. By all accounts, pretty much a bastard. But, also, by all accounts, the smartest and trickiest guy ever. Got a reputation for being able to trick the gods of Olympus. That was jolly in the short term, hellacious in the long term (by which I mean “for all eternity”). Zeus sentenced him to an eternity in Hades, with the sole hope that if he could roll a boulder to the top of a hill, he could get out. Or not: enchanted boulder that always slipped from his grasp a foot from the top and rolled all the way back down.

wine. Citing the Wine Intelligence US Landscapes 2019 report, there are apparently three million fewer wine drinkers between the ages of 21 and 35 than there were in 2015. What are they drinking? Mixed drinks and/or artisanal beers. The patience to do tastings to figure out what you like is not there. This will have implications for a number of the spirits companies that still have major wine operations, or those companies that are primarily wine producers. Wine making is a capital-intensive business that has a lot of moving pieces, as well as a number of things that can go wrong before you can actually bring product to market, including disease, weather, failed crops, pestilence, and sometimes, just bad luck. These trends were confirmed in a recent interview in the Weekend Wall Street Journal on July 20-21, 2019 with Rob McMillan, an executive vice president and founder of Silicon Valley Bank’s wine division. He indicated that his survey showed the dominant consumers of fine wine to be the baby boomers, who want to hear about how the wine was produced. And, they want to meet the Wine Whisperer who spoke to the grapes. The Millennials are avoiding wine because of price – it costs more than either beer or spirits. Unless that can change, the wine industry down the way will hit a brick wall.

wine. Citing the Wine Intelligence US Landscapes 2019 report, there are apparently three million fewer wine drinkers between the ages of 21 and 35 than there were in 2015. What are they drinking? Mixed drinks and/or artisanal beers. The patience to do tastings to figure out what you like is not there. This will have implications for a number of the spirits companies that still have major wine operations, or those companies that are primarily wine producers. Wine making is a capital-intensive business that has a lot of moving pieces, as well as a number of things that can go wrong before you can actually bring product to market, including disease, weather, failed crops, pestilence, and sometimes, just bad luck. These trends were confirmed in a recent interview in the Weekend Wall Street Journal on July 20-21, 2019 with Rob McMillan, an executive vice president and founder of Silicon Valley Bank’s wine division. He indicated that his survey showed the dominant consumers of fine wine to be the baby boomers, who want to hear about how the wine was produced. And, they want to meet the Wine Whisperer who spoke to the grapes. The Millennials are avoiding wine because of price – it costs more than either beer or spirits. Unless that can change, the wine industry down the way will hit a brick wall.  It could happen. But for those with patience, I refer you to Horizon Kinetics’ excellent Q2

It could happen. But for those with patience, I refer you to Horizon Kinetics’ excellent Q2

The launch of CNN changed all that. CNN needed to fill 24 hours a day with “news.” That forced a change from “sifting the wheat from the chaff” to “scrounging around for anything we can put on camera.” The iconic story for them is the coverage of a hostage-taking: a camera points resolutely at the front of a building (where there’s nothing to be seen) while a reporter resolutely tells us “we’re heard nothing from the police on-scene” … for three hours at a stretch.

The launch of CNN changed all that. CNN needed to fill 24 hours a day with “news.” That forced a change from “sifting the wheat from the chaff” to “scrounging around for anything we can put on camera.” The iconic story for them is the coverage of a hostage-taking: a camera points resolutely at the front of a building (where there’s nothing to be seen) while a reporter resolutely tells us “we’re heard nothing from the police on-scene” … for three hours at a stretch. Mr. Fisher is rich, famous and nearly ubiquitous. He also likely holds a Guinness world record for number of appearances in pop-up ads. But this advice (

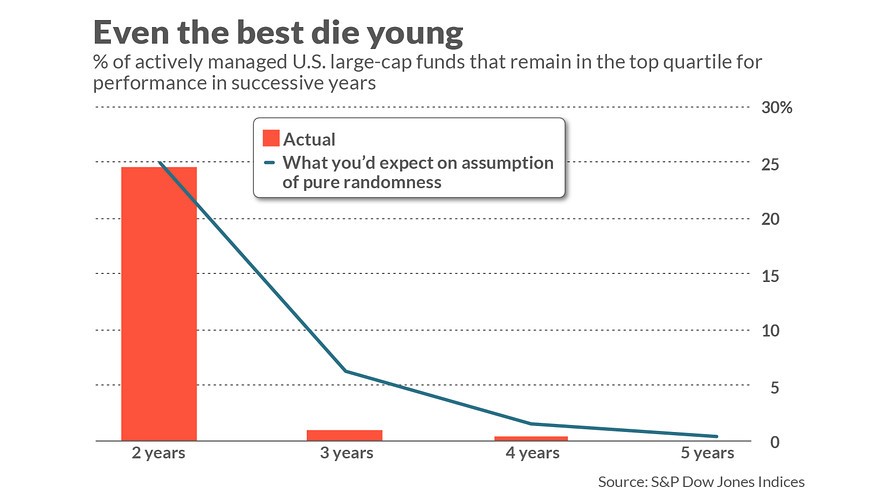

Mr. Fisher is rich, famous and nearly ubiquitous. He also likely holds a Guinness world record for number of appearances in pop-up ads. But this advice ( And still we get this freakish fetish about judging investments by whether they finish in the top XX% for XX consecutive years.

And still we get this freakish fetish about judging investments by whether they finish in the top XX% for XX consecutive years.  Ummm …. Two problems. First, this is meaningless data driven by the aforementioned stupid and destructive obsession.

Ummm …. Two problems. First, this is meaningless data driven by the aforementioned stupid and destructive obsession.

In another hit for the “follow the smart money” strategy, NYSE Pickens Oil Response ETF (BOON) will depart from the ways of the legendary T. Boone Pickens and become the properly corporatized Pickens Morningstar Renewable Energy Response ETF (RENW), tracking the Morningstar North America Renewable Energy Index at which point the “Pickens” in the name becomes a bit gratuitous.

In another hit for the “follow the smart money” strategy, NYSE Pickens Oil Response ETF (BOON) will depart from the ways of the legendary T. Boone Pickens and become the properly corporatized Pickens Morningstar Renewable Energy Response ETF (RENW), tracking the Morningstar North America Renewable Energy Index at which point the “Pickens” in the name becomes a bit gratuitous.