Dear friends,

Welcome to autumn. It’s a season of such russet-gold glory that even Albert Camus (remember him from The Stranger and The Plague?) was forced to surrender: “Autumn is a second spring when every leaf is a flower.” It’s the time of apples and cinnamon, of drives through the Wisconsin countryside, and of gardens turning slowly to their rest.

Open the windows, unpack the flannel, raise high the cup of cider. Summon the children, light the bonfires, deploy the marshmallows!

Welcome to the redesigned Observer. When I first started writing this column as the FundAlarm Annex nearly 12 years ago, our monthly issue represented one voice and was barely two pages long. The Observer today speaks through many voices and our combined offering to you sometimes runs to 40 pages. (Uhh … gratis.) Our traditional format, a single scrolling screen over 1000 lines long, was no longer able to serve you as well as you deserve.

Welcome to the redesigned Observer. When I first started writing this column as the FundAlarm Annex nearly 12 years ago, our monthly issue represented one voice and was barely two pages long. The Observer today speaks through many voices and our combined offering to you sometimes runs to 40 pages. (Uhh … gratis.) Our traditional format, a single scrolling screen over 1000 lines long, was no longer able to serve you as well as you deserve.

And so, we changed. A year ago, we decided to create a distinct magazine feel for the Observer to allow for much easier reading downloads and tracking. Chip, working with her stalwart chief programmer Andrew Beck, has been devoting nights and weekends to perfecting the layout you see now.

Well, okay, to “imperfecting the layout,” since we know you’ll discover glitches just as we have. When you do, for goodness sake, let us know. We’ll fix it if we can. I am, in any case, grateful to them both.

Here’s what you need to know:

- The overview of each month’s issue appears on what we’re called “the issue page.” That will give you snippets from every feature, a table of contents (in the far left column) and easy access to past issues (in the far right column). The design is responsive, so it will try to accommodate itself to whatever technology (desktop, laptop, tablet, phablet, phone or parchment) that you use to read us.

- This essay now serves as a sort of “letter from the publisher,” sharing reflections, plans and bits of information that don’t fit elsewhere. My longer articles, like this month’s story about emerging market returns, will appear separately. You’ll see them in our table of contents and on the first page of each issue.

- Each of my colleagues will be identified more easily now, since each story by Ed, Charles, Sam or Leigh will be standing alone. Within the next month, we hope to have an Author’s Page for each of them, which will share a bit of biography, links to their other sites and a compendium of everything they’re written.

- Fans of the long scroll haven’t been abandoned! We are also presenting each issue as a single long page. Here, for example, is the scroll for this issue. In general, just look on the

right-hand side of any page and select the “long scroll” option. - The table of contents will follow you wherever you go. No matter which article you click on, you’ll still see a table of contents on the left-hand side of your screen. If you want to go back to the issue page, just look to the right side for the “Issues: Magazine Layout” menu.

Updates

Grandeur Peak does cool stuff.

Earlier this year, Seafarer established a policy that equalized the investment minimums for their Investor and Institutional share classes. If a small investor (a) invested directly through Seafarer and (b) established an automatic investing plan with the intention of one day reaching the normal institutional minimum, Seafarer would grant them access to the lower-cost institutional shares for just the normal Investor minimum.

Grandeur Peak has followed suit, establishing the policy that the Investor and Institutional class minimums are identical ($2000) for individuals investing directly through Grandeur Peak.

The Fund offers two classes of shares, Investor Class and Institutional Class shares. The minimum initial investment for both share classes is $2,000 for each account, or $1,000 if an Automatic Investment Program is established; except that the minimum to open an UGMA/UTMA or a Coverdell Education Savings Account is $100. There is no subsequent minimum investment amount for either share class.

Existing Grandeur Peak direct shareholders just need to call the firm and they’ll move your investment into Institutional shares. Several folks on our discussion board found the process quick and pleasant.

Except for Global Stalwarts (GGSOX) and International Stalwarts (GISOX), their two “alumni” funds, the Grandeur Peak funds are closed to new investors. The latest prospectuses contain the reminder to Global Micro Cap investors that the fund will become somewhat more closed in the proximate future:

As of the close of business on December 31, 2016, the Fund is closed to both new and existing investors seeking to purchase shares of the Fund either directly or through third party intermediaries, subject to certain exceptions for participants in certain qualified retirement plans with an existing position in the Fund and direct shareholders with existing accounts who may purchase up to $6500 per year in additional shares.

They also promoted Mark Madsen and Brad Barth to the role of Industry Portfolio Manager on the Grandeur Peak Global Reach Fund (GPROX).

Royce Funds does cool research

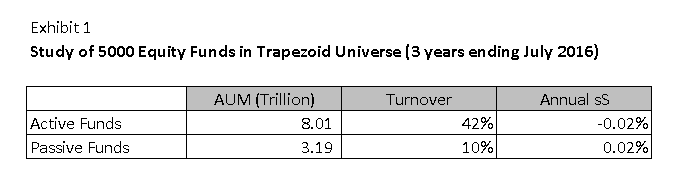

Royce recently released a white paper entitled, “The Undiscovered Connection: Value-Led Periods and Active Management” (2016). They begin with the surprising revelation that active management works in the small cap stocks:

Contrary to some investors’ perceptions, active small-cap managers actually have a strong relative performance record. Comparing Morningstar’s Small Blend category average (our proxy for active small-cap management) to the Russell 2000 Index over rolling five-year periods reveals that the Small Blend average beats the index 66% of the time.

As they delved deeper into the data, it appeared that active managers had their strongest performance in markets were value led growth. Active management outperformed in 83% of value-led periods. That makes a world of sense since market cap-weighted indexes are primarily growth and momentum driven.

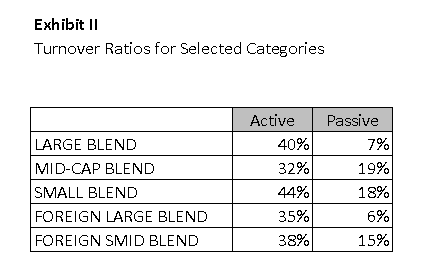

This follows the Leuthold Group’s intricate but still preliminary analysis, published in August 2016, of the characteristics of markets in which active managers succeed.

It’s also consistent with MFO’s own research findings. We looked at the equity categories where passive strategies should have their greatest advantage: domestic, global and international large-cap core funds. Unlike the ETF pundits, we chose to look at the funds’ risk-adjusted performance over the entire market cycle. That is, we asked “since markets go up and down, and funds make and lose money, doesn’t it make sense to look directly at periods that capture both up and down and measures that balance both gains and losses?”

We identified the 50 large core funds with the highest Sharpe ratios over the course of the entire market cycle. Of those, 42 were actively-managed funds. Only six were traditional cap-weighted index funds while two were smart beta products. Several of the actively-managed funds, e.g., DFA, had index-like properties.

More evidence that “the smart money,” ain’t.

If a guy had recently, oh, say, jammed his foot on the gas and driven his car off a cliff, I might hesitate to hire him as my chauffeur. You know, I might give him a while to establish a subsequent good driving record before hopping in the back seat and waving him on. Which, I guess, separates me from “the smart money.”

The Wall Street Journal reports that Rory Priday, the analyst whose work was behind the decision by Sequoia Fund (SEQUX) to stake its future on Valeant, has launched a new hedge fund and promptly received $75 million from rich people. We wish them, and him, only the best.

In Closing . . .

We’re always grateful for your support, verbal and financial, direct and indirect. It makes the many hundreds of hours that go into the Observer both possible and meaningful.

We’d like to thank, especially, Dan Wiener (he of the Independent Advisor for Vanguard Investors) for his generous gift and Jonathan Best (who, literally, is The …), who joins us as our third PayPal subscriber. Jonathan, with Deb (see ya in Albuquerque!) and Greg (hi, guy!), has chosen to express his support for MFO by setting up an automatic monthly contribution from his PayPal account. We’re grateful for the vote of confidence that it represents. Many thanks also to Gary, Thomas and Kent. We couldn’t do it without you.

We’d like to recognize a signal gift from Andrew and Michelle Foster of Seafarer Capital Partners. It will allow us to launch two long-anticipated projects, including making each month’s Observer available as a Kindle e-book on the Amazon marketplace. We’re hopeful that will extend our reach and serve our mission of helping investors and advisors think more calmly about the opportunities they might otherwise skip over. With SFGIX growing beyond our coverage universe and closing, the Fosters concluded that conditions that a contribution to the Observer would not pose a material conflict-of-interest. That leaves only the question of the Value fund (SFVLX), which we plan to approach carefully and with clear disclosure.

Thank you all, go raibh míle maith agat!