Dear friends,

Welcome to winter.

Dame Edith Sitwell, a poet and crank, observed, “Winter is the time for comfort, for good food and warmth, for the touch of a friendly hand and for a talk beside the fire: it is the time for home” (Taken Care Of: An Autobiography (1965)).

How could you not be drawn to someone who said of herself, “I am not eccentric. It’s just that I am more alive than most people. I am an unpopular electric eel set in a pond of catfish”?

Our local version of “good food and a talk beside the fire” has been enriched by the books folks have lately showered upon us:

The Revolutionary: Samuel Adams (2022), who is a mostly forgotten author of the American revolt in the 1760s,

Heirloom Fruits of America: Selections from the USDA Pomological Watercolor Collection (2020), which literally illustrates the long history of fruit-growing here,

Banned Books (2022) which takes us from “The Decameron Tales” to I Hate Men,

Rogues: True Stories of Grifters, Killers, Rebels, and Crooks (2022), which manages to suck in billionaire Stephen Cohen and tells the story of Mark Burnett’s resurrection of Donald Trump as a business icon,

My Inventions: The Autobiography of Nikola Tesla (1919), which ends with Tesla’s prophesy about AI: Machines “will ultimately be produced, capable of acting as if possessed of their own intelligence, and their advent will create a revolution.”

A Field Guide to Cheese: How to Select, Enjoy, and Pair the World’s Best Cheeses (2020) is touted as a “cheese lover’s dream,” featuring over 400 cheeses accompanied by illustrations.

Chip and I look forward to the next snow day with cheerful anticipation, dented only by the realization that our college’s adoption of electronically mediated remote work takes a lot of the fun out of being stranded at home.

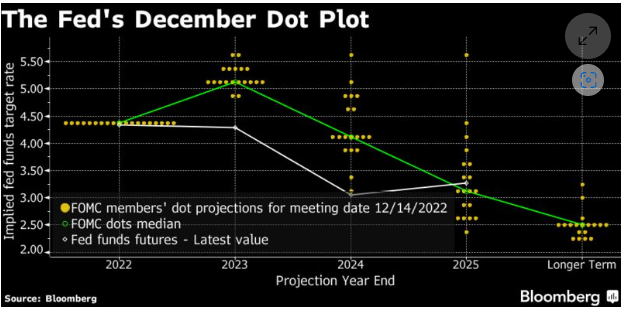

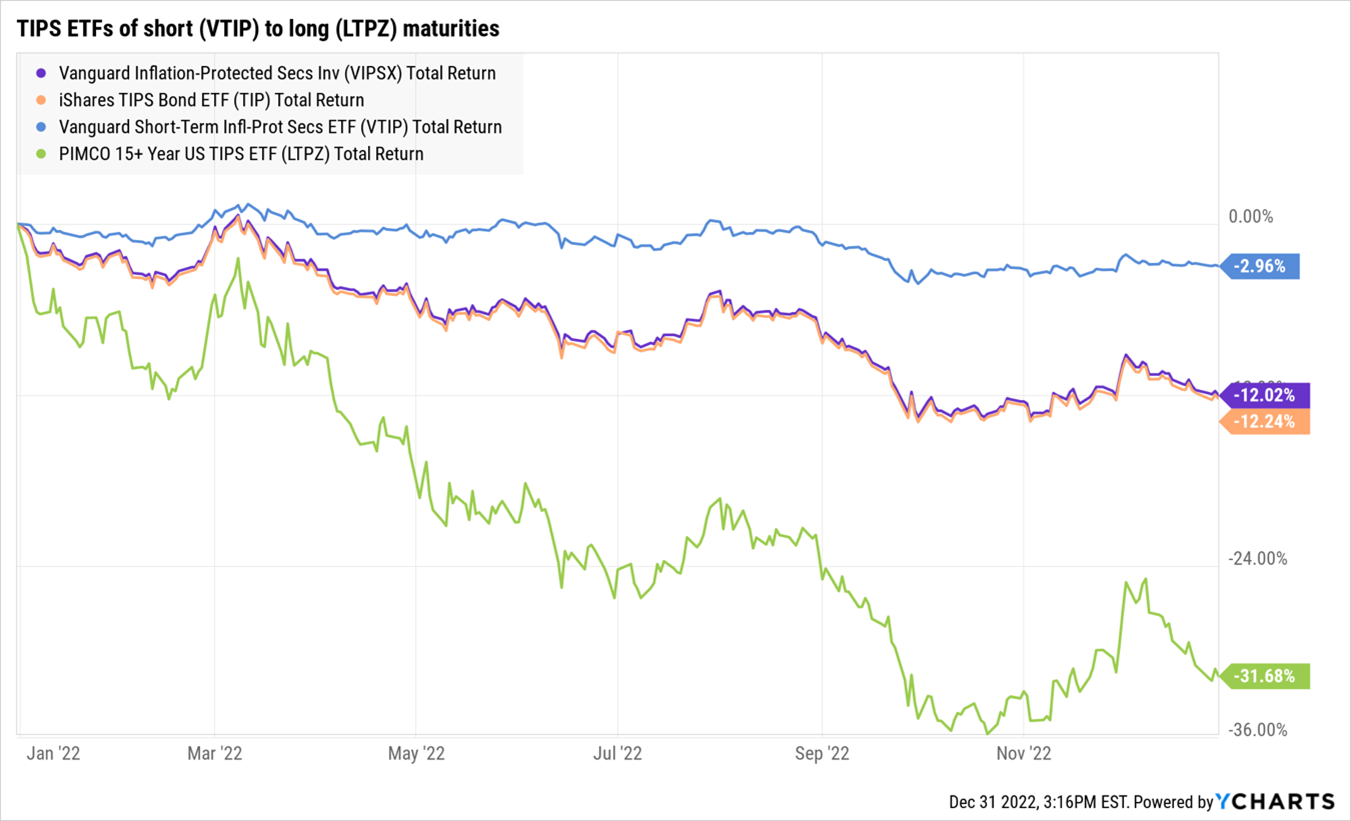

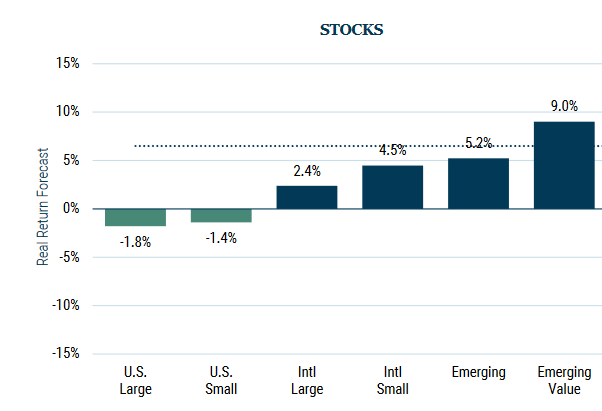

This note is organized around two questions, two announcements, three remembrances, and a request. The remainder of our New Year’s issue shares: Devesh Shah’s endorsement of long-dated TIPS as an investment whose time has come, Lynn Bolin’s warning of risky times ahead and funds that might navigate them, The Shadow’s update on the industry’s hijinks – including several well-known managers whose names are being removed from funds they piloted – and Charles’s announcement of an imminent webinar for the MFO Premium-curious. My contribution will be to suggest three places to flee from and three to wander towards.

I wonder if Elon Musk follows MFO?

In cleaning the spam directory this month, I came upon an unsigned email from an untraceable anonymous account with a nonsensical name (defund blm) and a huffy defense of Elon Musk:

Hi,

You wrote, “Investors have lost a cumulative $22 trillion in 2022 (with the sole bright spot being that Elon Musk has personally lost over $100 billion).”

Why is Musk losing billions supposed to be a bright spot can only be an attack on his politics and/or Twitter ownership. I was going to make a donation but won’t but since MFO obviously pushes a certain political ideology and it’s not neutral like a financial advice website should be.

Umm … howdy, sir! Glad to have you abroad.

Why is Mr. Musk’s relative decline worth noting? He’s symptomatic of a broader problem, the influence of plasticene billionaires on the lives of the rest of us. Our courts have ruled:

- That corporations are people,

- That money is speech, and

- That we don’t get to learn the identity of who’s speaking to us.

America’s 700 billionaires have been saying a lot lately, spending $880 million on the midterm elections. At least $300 million was channeled through untraceable “dark money” PACs. Since the task of PACs is to win elections, not to tell the truth or strengthen the country, those hundreds of millions translate into rather a lot of divisive messaging.

That class of people seems divided between the invisible (Richard Uihlein is the cycle’s #2 donor) and the iconic (George Soros is #1). There’s an entire industry built around creating those icons: heroic founders, lone-wolf geniuses, visionaries, mavericks, and saviors of the world who, just by happenstance, are rich beyond the dreams of avarice. (And who, on whole, would prefer to arrange things so that it remains that way.) The financial media – long recognized as financial pornographers – revel in the tale.

Mr. Musk has a carefully constructed myth that masks serious personality disorders. Two scholars write, “his recent behaviour belies the esteem and appeal he’s cultivated and has thrown his credibility, stability of reasoning and personal character into question.” And that was four years ago, in 2018. Mr. Musk is not unique in those flaws – imagine a heart-to-heart with Mark Zuckerberg if you dare – but he is uniquely visible. The spectacle of his flame-out at least opens the door to serious conversations about how best to rebuild a sense of shared respect and commitment to the common good.

Why does Wells Fargo have any customers left?

Really.

These people are so consistently predatory that the director of the federal Consumer Financial Protection Bureau has denounced Wells’ “rinse-repeat cycle of violating the law” and imposed nearly $4 billion in penalties. That follows the $3 billion penalty imposed by the Department of Justice and SEC two years ago. The latest crimes involve illegal repossession of people’s homes and cars, on top of profitable and illegal overdraft fees.

These people are so consistently predatory that the director of the federal Consumer Financial Protection Bureau has denounced Wells’ “rinse-repeat cycle of violating the law” and imposed nearly $4 billion in penalties. That follows the $3 billion penalty imposed by the Department of Justice and SEC two years ago. The latest crimes involve illegal repossession of people’s homes and cars, on top of profitable and illegal overdraft fees.

Ethan Wolf-Mann chronicled the complete list of Wells Fargo scandals for 2016-2019, where the firm managed a rigorous pace with nearly one scandal per month. The Congressional Research Service covers the same time range in a less engaging style. The FinanChill blog extended the scandal roster back to 2010.

The “lather-rinse-repeat” cycle mentioned above is almost reassuring in its constancy: combine rapacious impulses and a near-total disregard of the need for internal control structures, screw the people who’ve entrusted their financial security to you, get caught, flop about, then pay another couple billion in penalties while promising that this time is really is THE NEW Wells Fargo, then repeat. While other firms have been more egregious, none of them have survived.

Devesh makes better use of his free time than I do

The last book written by Thorstein Veblen (1857-1929), inventor of the term “conspicuous consumption” and author of dozens of works on economics, was not a work in economics. It was the translation of, and commentary on, The Laxdæla Saga, a 13th-century Icelandic tale of a love triangle between Guðrún Ósvífrsdóttir, Kjartan Ólafsson, and Bolli Þorleiksson. Kjartan and Bolli. (But you knew that already, didn’t you?) He seems to have translated the work in 1899, forgot about it, then remembered and published it in 1925. Described as “a lone and reluctant Viking” at war with the 20th century, he arrived at Carleton College speaking only Norwegian,  learned English, Greek, and Latin there, then later Danish, Swedish, Italian, French, Spanish, Dutch … and, finally, Icelandic. He thought we needed to understand Iceland at the end of the Viking era in order to understand the rise of the modern world, so he learned Icelandic and translated the saga for our benefit.

learned English, Greek, and Latin there, then later Danish, Swedish, Italian, French, Spanish, Dutch … and, finally, Icelandic. He thought we needed to understand Iceland at the end of the Viking era in order to understand the rise of the modern world, so he learned Icelandic and translated the saga for our benefit.

Our colleague Devesh Shah, unlikely to be seen as a Viking, much less a lone and reluctant one, has nonetheless undertaken a similar challenge. Devesh serves as the translator for Nine Children’s Plays, written by Gujarati author, playwright, and actor Prakash Lala. Devesh notes that “Children everywhere have similar problems and questions,” which Lala has been addressing in a series of stories, including “The Emperor of Fools” and “I wish I could be a Bird,” set in India over the past quarter century. The work is available on Kindle for $9.99.

The Independent Vanguard Adviser is now live on the web

As we noted in early autumn, the publisher of The Independent Adviser for Vanguard Investors rather abruptly decided to pull the plug on the venerable and well-respected newsletter. Lewis Braham lamented, “the independent voice on the world’s largest mutual fund manager … published its last issue in October – not by choice.”

The publisher offered just that “interest has waned” without elaboration.

After some deliberation and scrabbling, Dan Wiener and Jeff DeMaso relaunched their service on a new site under a slightly changed brand: the Independent Vanguard Adviser. Dan began publishing the Independent Adviser in 1991 (Forbes dubbed it “Vanguard’s alter ego”) and holds the titles of co-editor and senior adviser now. Jeff joined the operation in 2011 and is officially the editor and founder of the new publication.

Like MFO, they accept neither advertising nor sponsorships from Vanguard, its competitors, or advisers. They’re supported by reader subscriptions (the annual fee is $175/year, with a free 30-day trial available), allowing them fairly to claim “independent, honest, unbiased coverage of all things Vanguard.”

When I asked Jeff what readers might expect at the reborn site, he offered this:

In terms of features, we offer a free weekly market (and Vanguard) update email. Premium members get much more … Model Portfolios, a Performance Review with buy/hold/sell ratings on every Vanguard fund, and at least one additional (more analytical) article each week. We also tie it all together with a monthly recap.

Some of the topics we’ve explored so far are the death of the 60/40 portfolio (I don’t think it’s dead) and what does the yield curve inverting mean (probably a recession ahead, but timing the market is still difficult). We’ve also provided subscribers with all the details (estimated capital gain distributions) and key dates they need to navigate distribution season at Vanguard. We’ve also covered everything from Vanguard’s technology woes to new fund launches to inflation to ESG … we try to cover a lot of ground.

In addition to Braham’s praise, in 2020, the New York Times cited the newsletter as one of three publications – alongside Morningstar’s FundInvestor – ideal for DIY investors (D.I.Y. Retirement Investors Have a Low-Cost Friend: Newsletters, 1/30/2020). A few months earlier, Kiplinger’s named it one of the four best investment newsletters (8/21/2019). Dan’s willingness to torch Vanguard’s management when it deserved to be torched has been appreciated by folks on the MFO Discussion board as they struggled to make sense of increasingly wretched customer service.

Our colleague Sam Lee wrote a fascinating piece for us in 2015, “Why Vanguard Will Take Over the World” (9/2015), which concluded with a warning:

Vanguard is eating everything. Vanguard’s rapid growth will continue for years as it benefits from three mutually reinforcing advantages: mutual ownership structure where profits flow back to fund investors in the form of lower expenses, first-mover advantage in index funds, and a powerful brand cultivated by a culture that places the investor first. Still, Vanguard may wreck its campaign of global domination in several ways, including lagging in institutional money management, incompetence, corruption, or operational failure.

When he wrote that, Vanguard had vacuumed up $3 trillion in assets. Today, that total stands at $4.5 trillion. It seems like a group that warrants close attention. To date, no one’s been better at it than Dan and Jeff. There have been some bumps along the road to independence, occasioned mostly by their former publisher’s reluctance to help them transition to an independent existence by sharing, for example, subscriber information. If you’re affected by transition challenges, it would be prudent to reach out directly to them.

A quick confirmation: MFO has no financial stake in or ties with IVA; they’ve neither asked us to run nor compensated us for this notice. We’re sharing it because it’s worth knowing.

In Memoriam …

We’d like to note the passing of three memorable figures, all good people gone too soon.

Franco Harris, 72, the former Pittsburgh Steelers running back. Mr. Harris seemed the picture of health and vitality. He spent his last day chatting with strangers and the media in advance of the retirement of his number by the Steelers (only the third player in a century so honored) and celebrations surrounding the 50th anniversary of his most famous play. He came home, told his wife that he felt a bit out of breath, sat down, and never rose again.

Franco Harris, 72, the former Pittsburgh Steelers running back. Mr. Harris seemed the picture of health and vitality. He spent his last day chatting with strangers and the media in advance of the retirement of his number by the Steelers (only the third player in a century so honored) and celebrations surrounding the 50th anniversary of his most famous play. He came home, told his wife that he felt a bit out of breath, sat down, and never rose again.

Those of you not raised in Pittsburgh can’t quite grasp Harris’s significance to the city. NFL fans know that his “immaculate reception” play, a game-winning reception with 22 seconds left, was named the greatest play in NFL history. (Oakland Raiders fans consider it the greatest crime in the league’s history.) Few outside the city understand why Joe Greene, the greatest Steeler player ever, declared, “he taught us how to win,” and former coach Bill Cowher averred that Harris taught him “what it means to be a Pittsburgh Steeler.” His arrival was preceded by 39 years of team futility and followed by the rise of the NFL’s most iconic franchise. (The NFL offered the term “America’s team” to Steelers owner Art Rooney, Sr., who turned it down with a gruff dismissal: “we’re not America’s team, we’re Pittsburgh’s team.” The marketing slogan was bequeathed to the league’s second choice, Dallas.) Harris’s heroics and deep-seated humanity inspired the rise of Franco’s Italian Army and gave a sense of hopefulness to his adopted hometown. He was active in the city’s life and culture for the 38 years following his retirement.

Scott Minerd, 63, Guggenheim Partners global chief investment officer and long-time bodybuilder, suffered a heart attack during his regular workout. Mr. Minerd was the son of a Pennsylvania insurance salesman of modest means, worked his way up as a bond trader for Morgan Stanley, detested the insane demands, moved to California at 37 with the intent to retire … and found himself bored silly. He met the Guggenheim family in 2000, became a founding member of Guggenheim Partners, and rose to become CIO and pundit. His name often appeared on lists of “bond kings” that include Bill Gross, Dan Fuss, and Jeffrey Gundlach. Through it all, he strove to maintain balance and perspective and was celebrated for his “beautiful mind, big heart, and compassionate soul.”

Kathleen Moriarty, 69, a Chapman and Cutler partner who was instrumental in the creation of the first ETF, earning her the designation “SPDR Woman” and the sobriquet “the ETF industry’s Greatest of All Time super lawyer.” Her family has not shared information concerning her passing.

Life is uncertain, dear friends. Don’t wait until tomorrow to attempt the kindness you can do today.

Children need you, and others are willing to underwrite your generosity.

I don’t know if it’s a past life issue, a tough childhood, or something more prosaic, but I react very strongly to the prospect that children are being left cold and hungry. As we sit at the turning of the year, I’ve been particularly saddened by the events in Ukraine. Putin is no longer pursuing a war; he’s simply lashing out and crushing as many lives as he can by targeting Ukraine’s civilian utilities. UNICEF notes that essentially every child in the country is at risk:

Continuing attacks on critical energy infrastructure in Ukraine have left almost every child in Ukraine – nearly seven million children – without sustained access to electricity, heating, and water as winter deepens. (12/13/2022)

In broad climate terms, Ukraine’s winter is comparable to Chicago’s.

There is currently a 2:1 match available for contributions through the UN High Commission for Refugees, which would reach children in, and beyond Ukraine. (Charity Navigator offers a list of other highly responsible, highly effective charities in the same field.)

For folks more concerned about our own country’s children, the Donors Choose organization – which works to link individual classroom teachers in need with citizen donors – has three projects that (a) are aimed at providing food, water, or clothing to students in poor neighborhoods and (b) have a match of 2:1 or more available. If you’re willing to consider projects without a foundation’s matching grant, there are over 1400 teachers reaching out for help to keep their students warm and fed. A few of those projects expire tonight, more tomorrow, and more every day thereafter.

A quick confirmation: in the past week, Chip and I have contributed to the UNHCR and supported three classroom projects. That support does not implicate MFO’s finances; it’s personal.

Thanks, and more thanks!

First and foremost, to the 150,000 of you who read MFO this year. Your interest, as much as any direct support, keeps the lights on!

New Year’s blessings to our indispensable regulars, including the good folks at S&F Investment Advisor in lovely Encino, Wilson, Gregory, William, the other William, Brian, David, and Doug.

Our bashful mention of the possibility of a year-end contribution brought responses from a bunch of good folks. First and foremost is Joe McCollum, who shared a long and thoughtful reflection on life and personal finance over our decades together as writer and reader. His challenges, far from the trivialities of the market, are great, and we hope we can continue to offer a bit of support, cheer, and perspective as he – and you – navigate them.

Finally, to Robert M., Dick (we’re so glad you enjoy our work), Charles of Spring Lake, Thomas L., Sunny, Kevin from Brooklyn, Kevin from Chico, Donald, Mark and Sara, Mark P. (we appreciate your ongoing support), Eric G. (thanks for the note!), Joseph, and James (with a Frost quote, no less!). We thank you all.

As ever,

Rich people are different from you and me. They buy stuff we’re not able to. Good stuff. Hedge funds. (Which are mostly disasters.) Farmland. (Which was a great investment before it became a liquid investment class.) Small islands. (

Rich people are different from you and me. They buy stuff we’re not able to. Good stuff. Hedge funds. (Which are mostly disasters.) Farmland. (Which was a great investment before it became a liquid investment class.) Small islands. (