Dear friends,

Welcome to Spring. Some diehards erroneously insist that they’re “officially” winter-bound until the Spring equinox, March 20th this year. It need not be so.

There are two springs. Meteorological spring, which is aligned with temperatures and growing seasons, is March 1st. Astronomical spring, which is aligned with the wobble of the earth on its axis (called “precession”), begins with the spring equinox.

To get a reading on what the season was, I cruised the grounds outside of Old Main. Based on my extensive survey of hyacinths, hostas, and croci… it’s spring. That’s my story, and I’m sticking to it. Even when it snows.

It’s a time when my students’ fancy turns lightly to … well, you know, sorority rush, summer, and pretty much anything other than the projects I’ve assigned them. But it is also, Tolstoy declared, “the time of plans and projects.” We have some!

Celebrate spring by making a difference

The Russian war in Ukraine seems to have devolved into simple genocide. As with the First World War, the utter inability to formulate a plan that allows either decisive victory or clean withdrawal has led to a simple equation: if we Russians die by the tens of thousands and the Ukrainians die by the thousands, we might eventually “win” by attrition.

The Russian war in Ukraine seems to have devolved into simple genocide. As with the First World War, the utter inability to formulate a plan that allows either decisive victory or clean withdrawal has led to a simple equation: if we Russians die by the tens of thousands and the Ukrainians die by the thousands, we might eventually “win” by attrition.

Consider donating, as we’ve done on several occasions in the past month, to the UN Commission for Refugees or one of the groups vetted by Charity Navigator. Victoria Odinotska, a native of Ukraine and president of a really good media relations firm, Kanter Public Relations, believes that the two of the most compelling Ukraine-based options for those looking to offer support is Razom for Ukraine (where “razom” translates as “together”) and United Help Ukraine, which has both humanitarian aid for civilians and a wounded warriors outreach.

There are small children who will remember the conflict for the rest of their lives; I’m hopeful that they have cause to remember the unstinting kindness of strangers as well.

In this issue …

Our modestly late launch reflects a modestly chaotic week for us. Many adventures, some of which will surely turn out well for us. For now, here’s the 411:

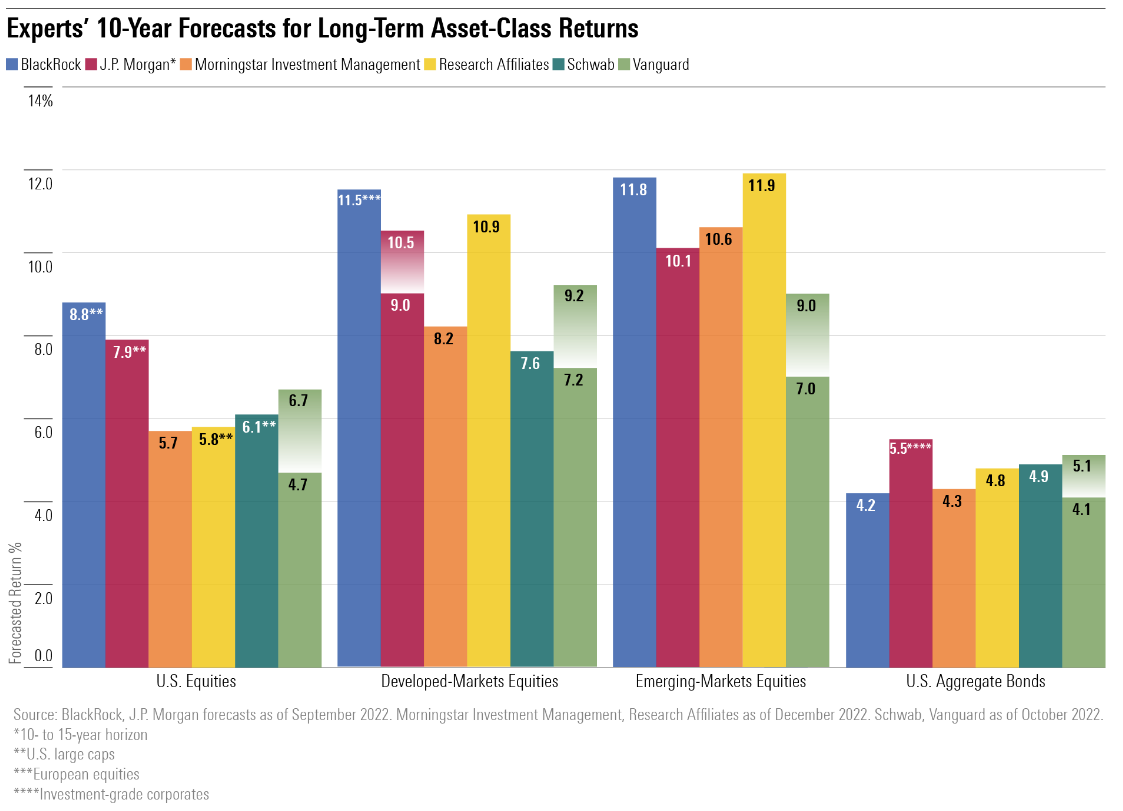

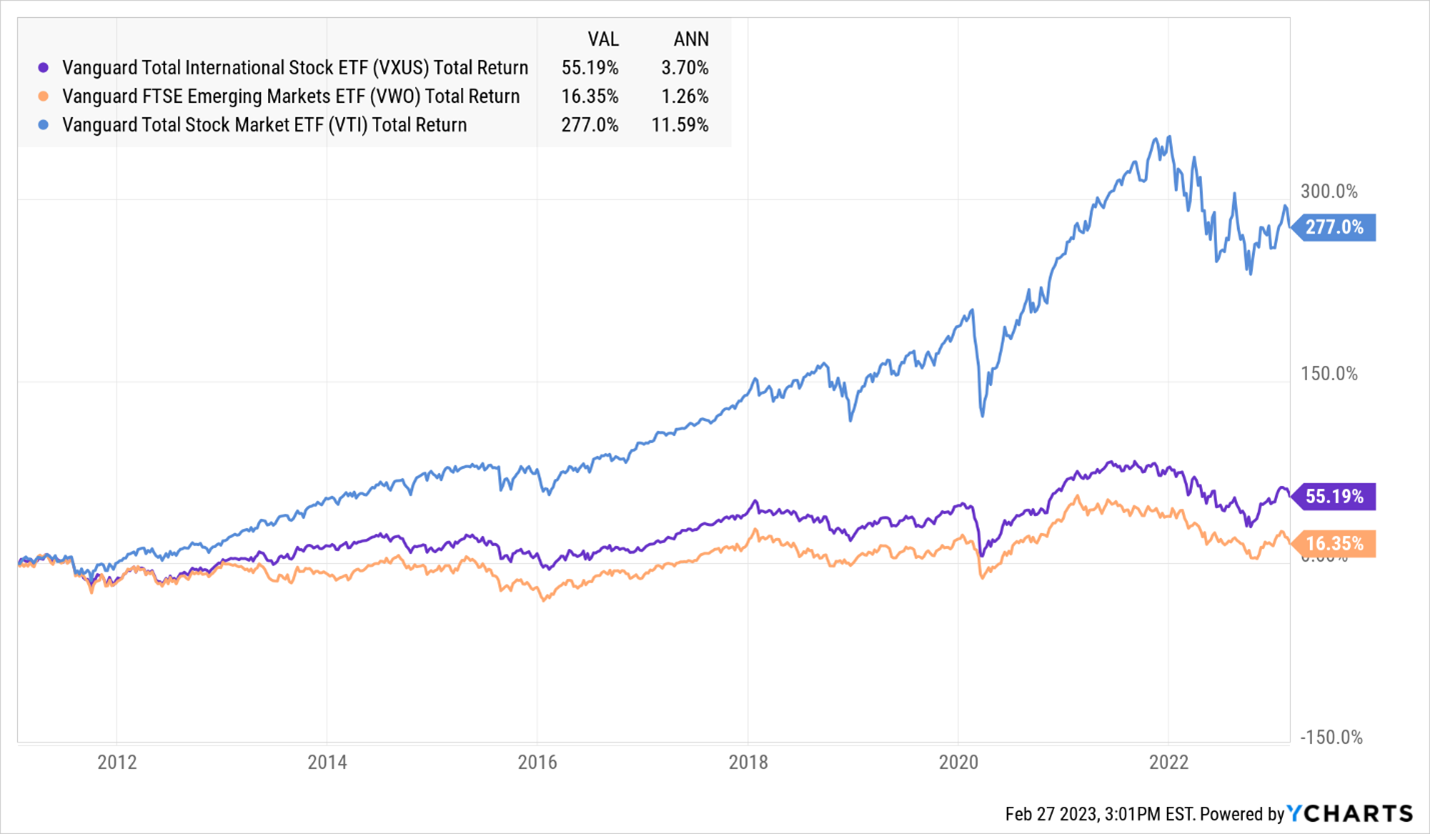

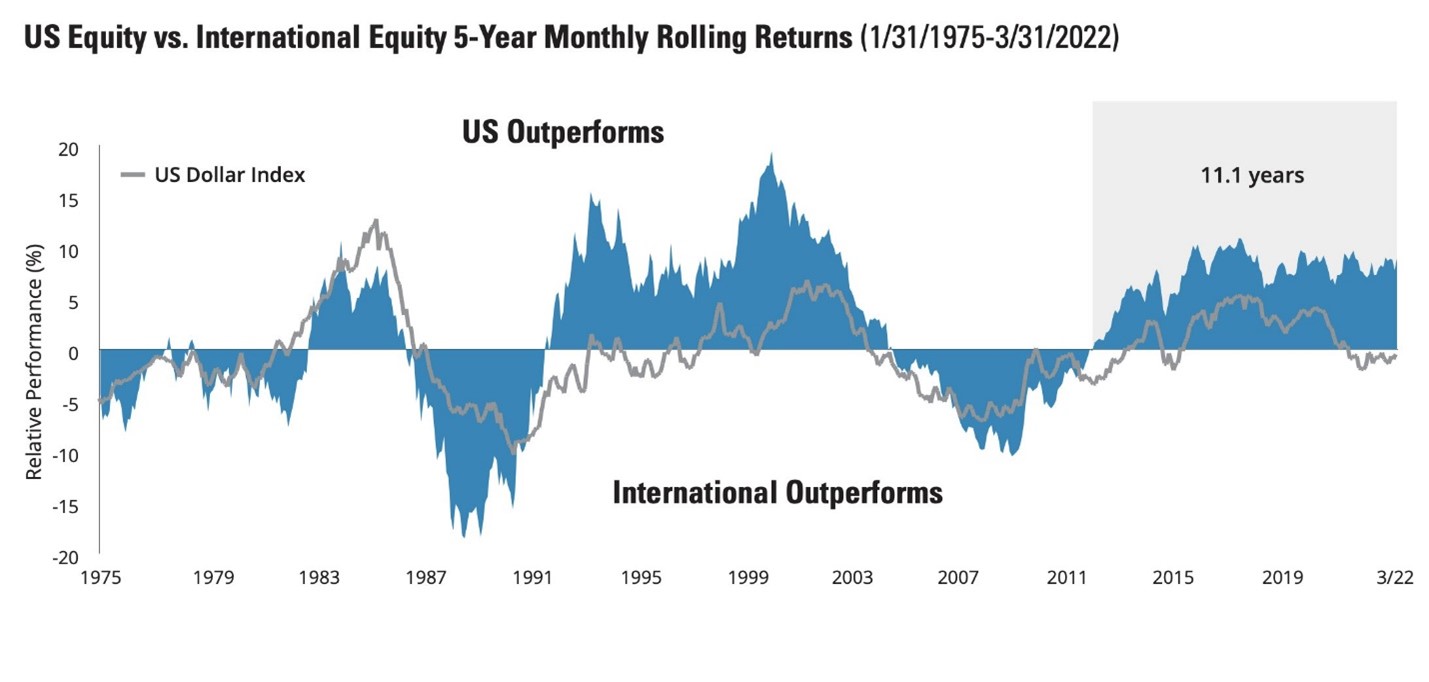

Devesh has been thinking about international investing and the heretical, for him, notion that active investors might be the way to go. He offers a limited endorsement of the notion in “Just short of two cheers for active, international investing.”

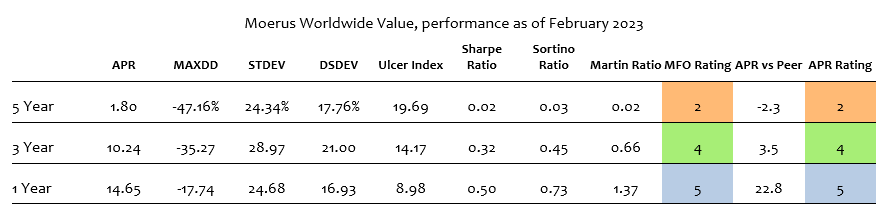

Devesh’s most recent conversations on the subject have been with Amit Wadhwaney, founder of Moerus Capital Management and manager of the resurgent Moerus Worldwide Value fund. Devesh shares a detailed summary of Mr. Wadhwaney’s career and his take on how best to invest in “Interview with Amit Wadhwaney.”

Lynn Bolin tries to untangle some of the threads from the tapestry of the maddening uncertainty and contradictions we’re confronting in the market, in “Looking Beyond 2023 Investing – Lies and Statistics.”

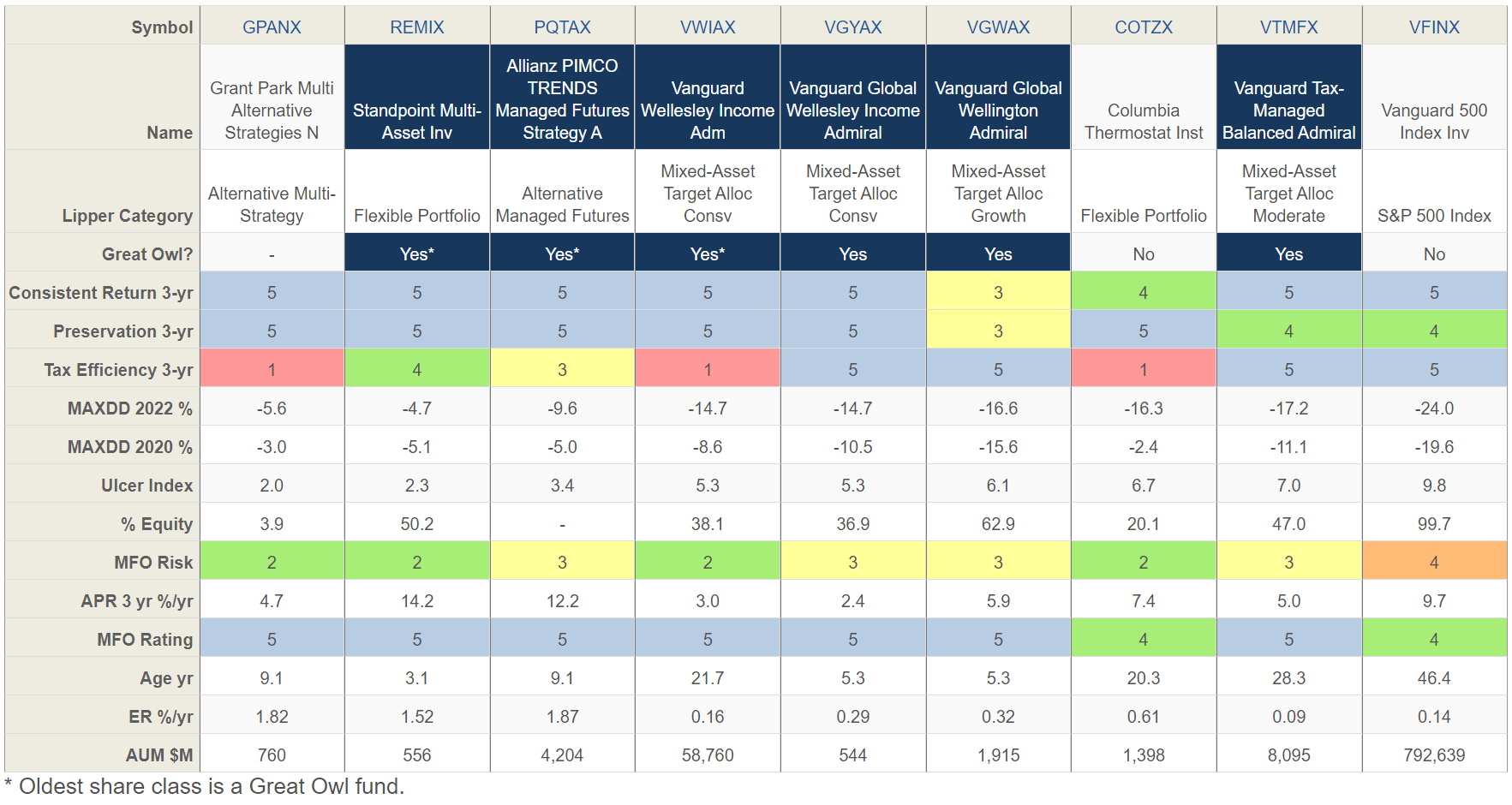

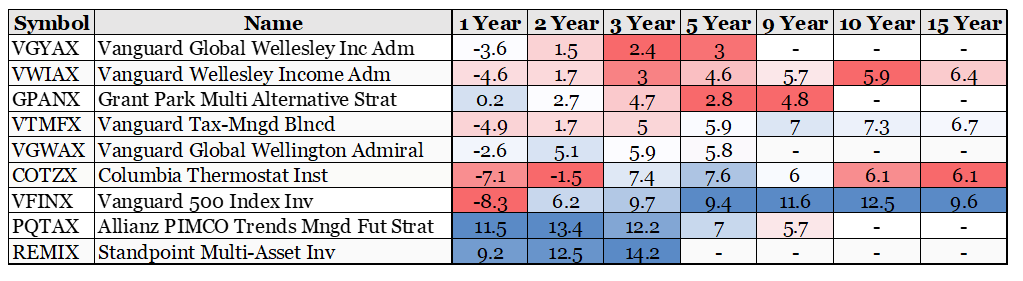

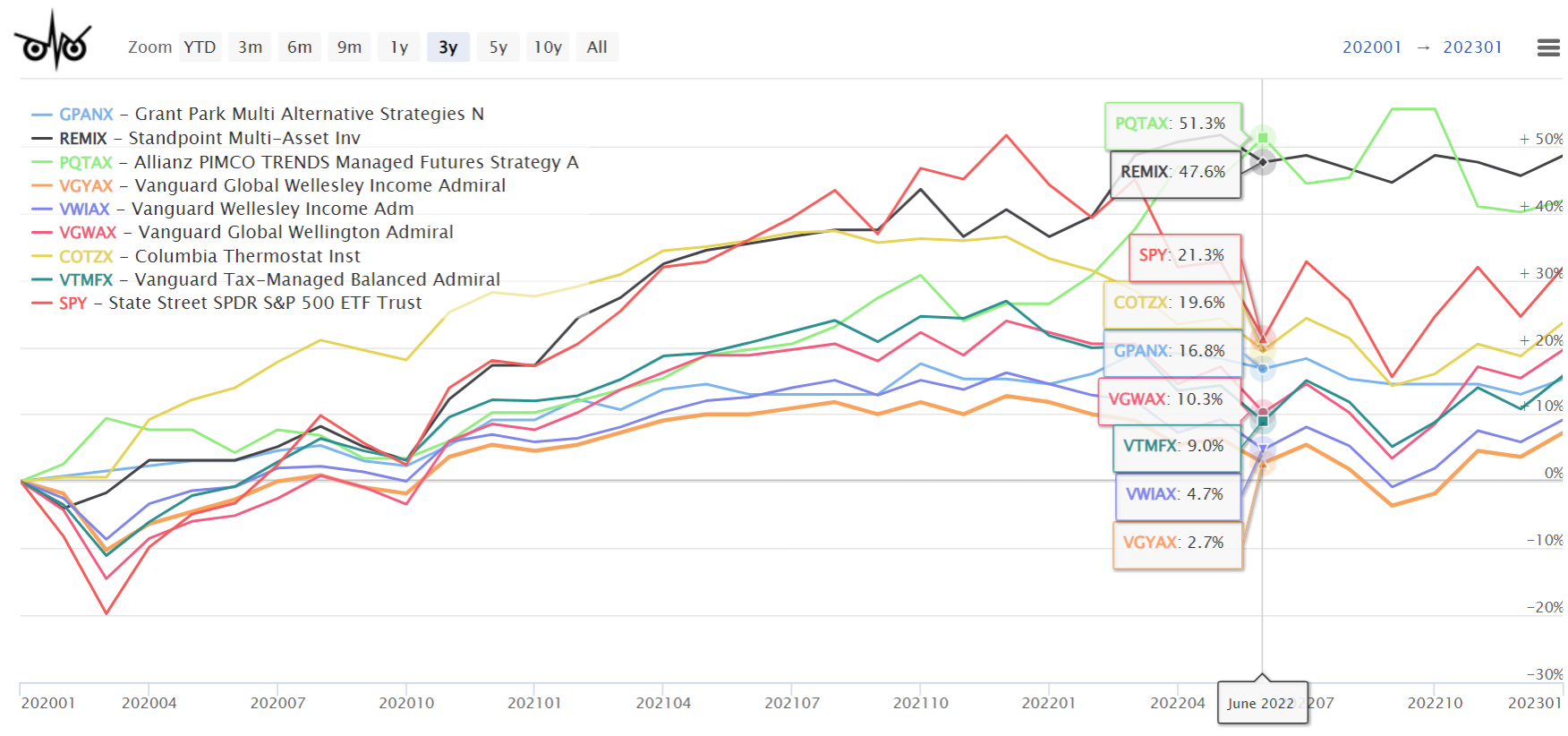

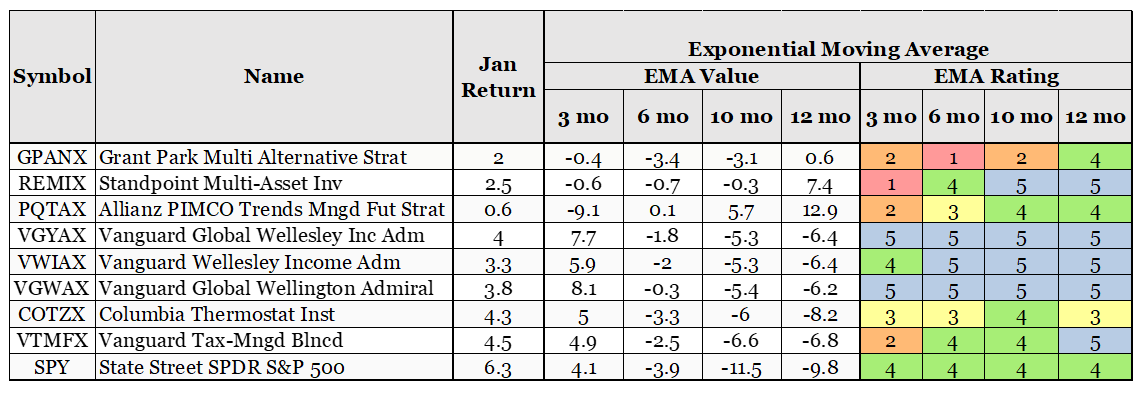

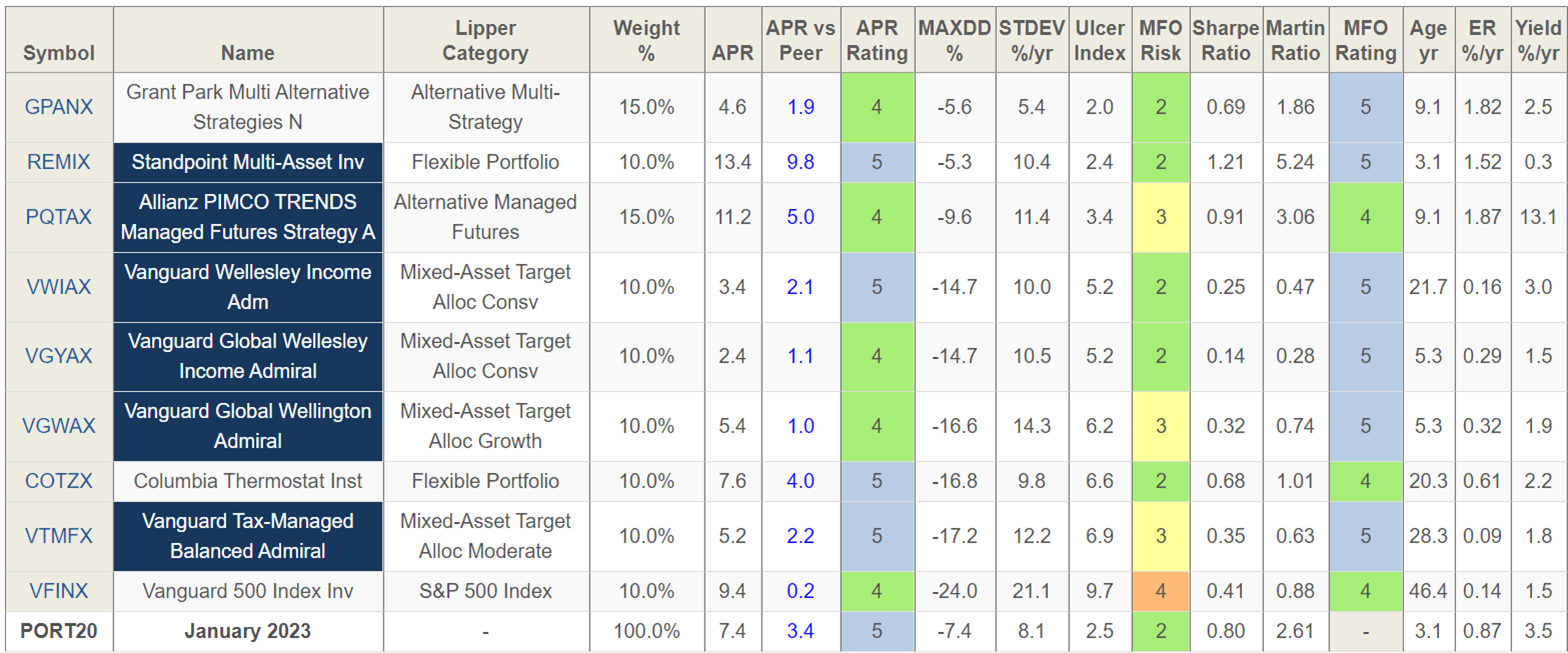

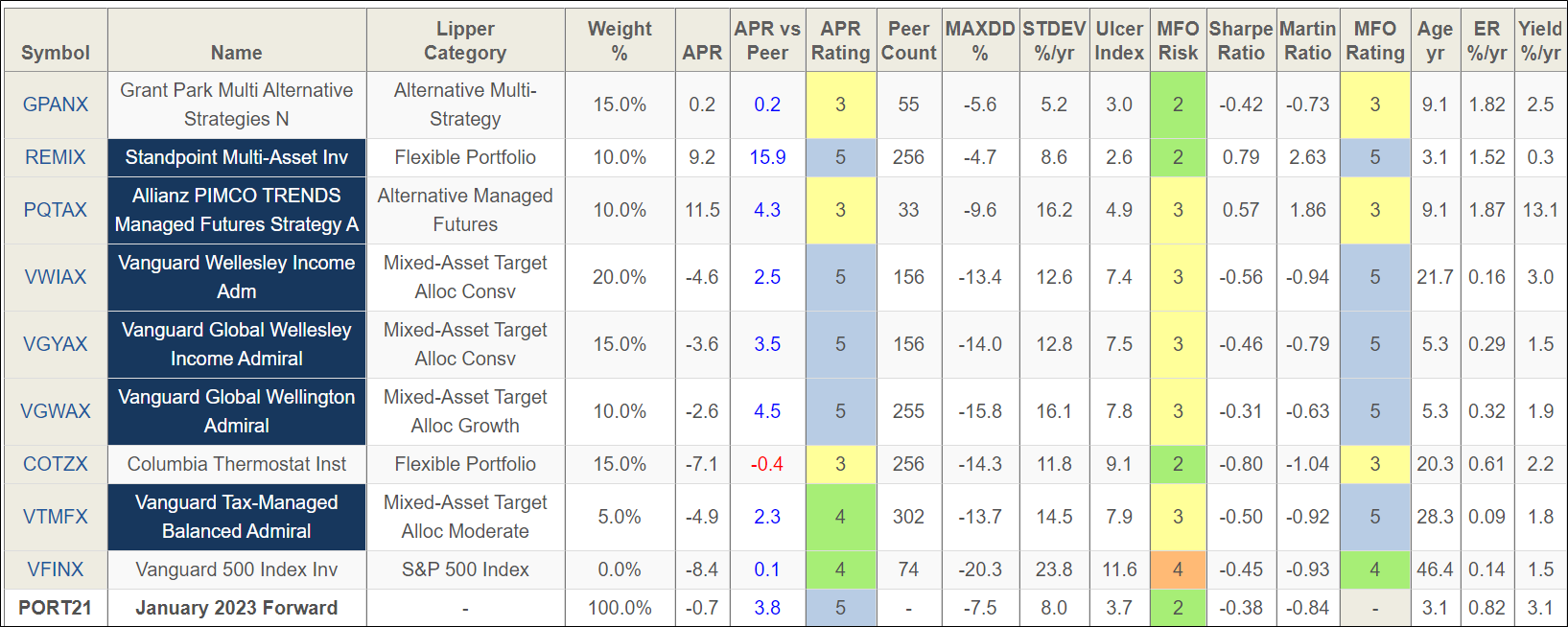

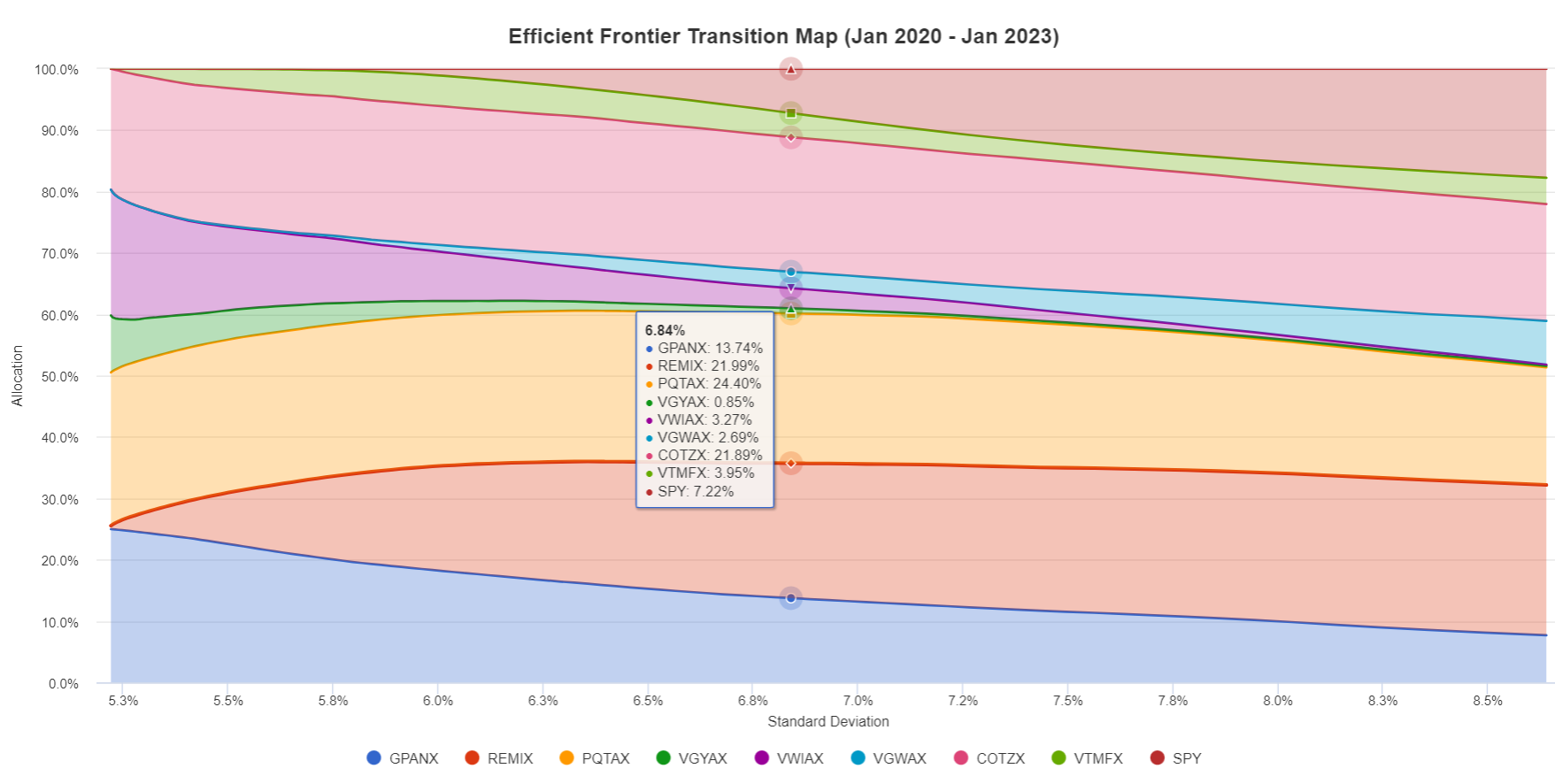

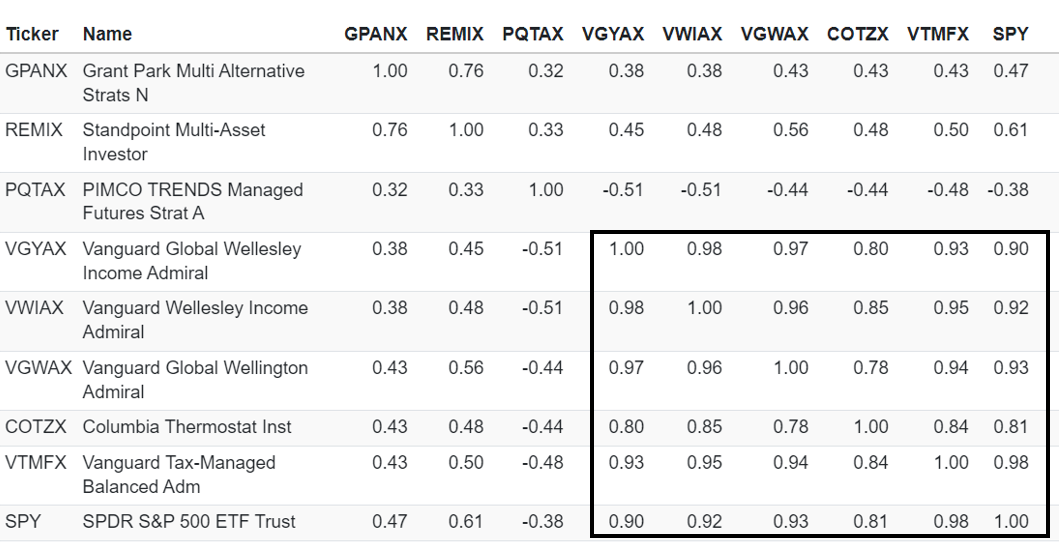

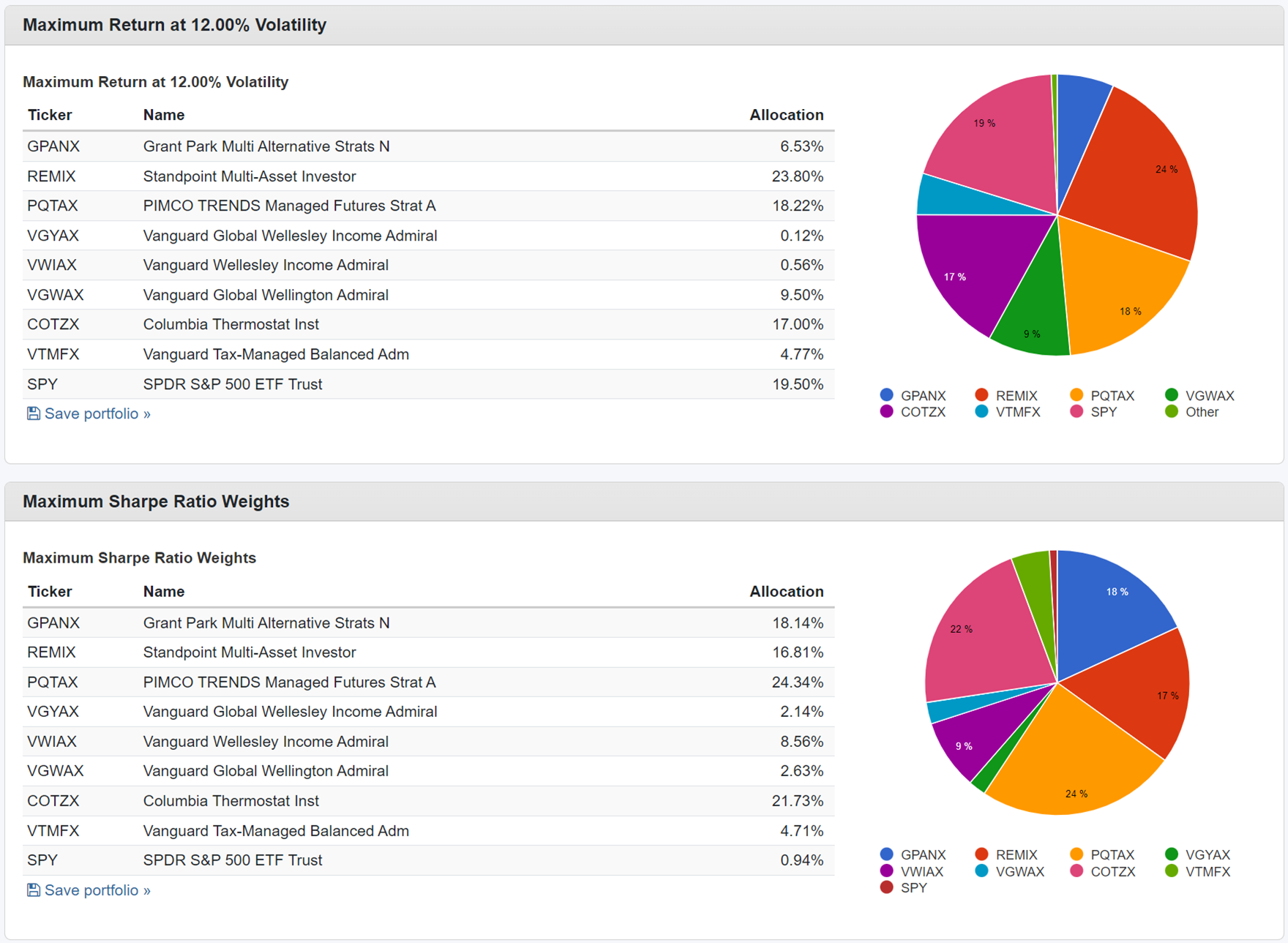

Lynn, at the same time, approached the question of whether his own portfolio was overdue for a haircut. He walks us through the process of assessing the continued attractiveness of individual funds in “To Sell or Not to Sell? (REMIX, PQTAX, GPANX, COTZX)” If you don’t recognize the symbols, they are

- REMIX: Standpoint Multi-Asset

- PQTAX: Allianz PIMCO TRENDS Managed Futures Strategy

- GPANX: Grant Park Multi Alternative Strategies

- COTZX: Columbia Thermostat

Spoiler alert: It’s good news for COTZX, okay news for PQTAX, and a holding pattern for REMIX and GPANX. Even okay news is good news for REMIX: Lynn decided that his current position was substantial and justified, even if it didn’t need to grow.

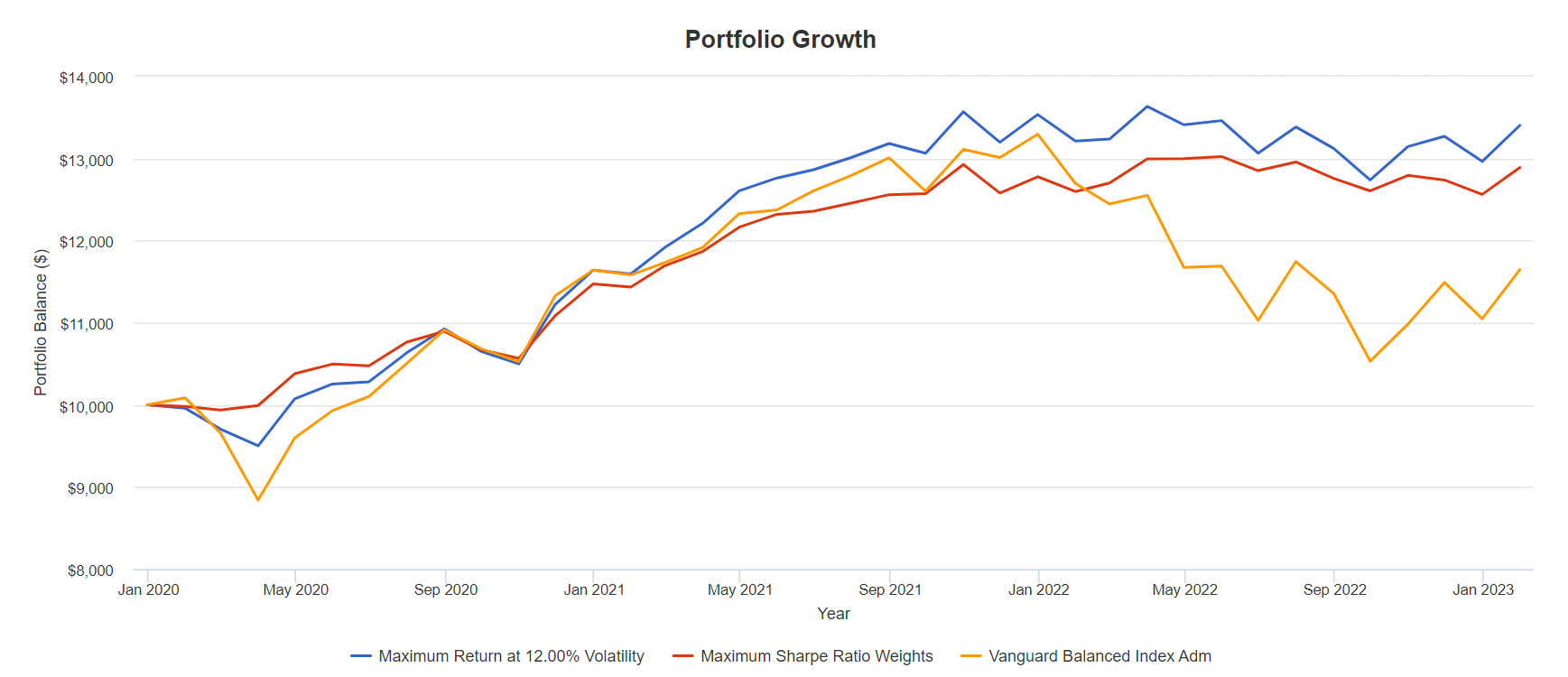

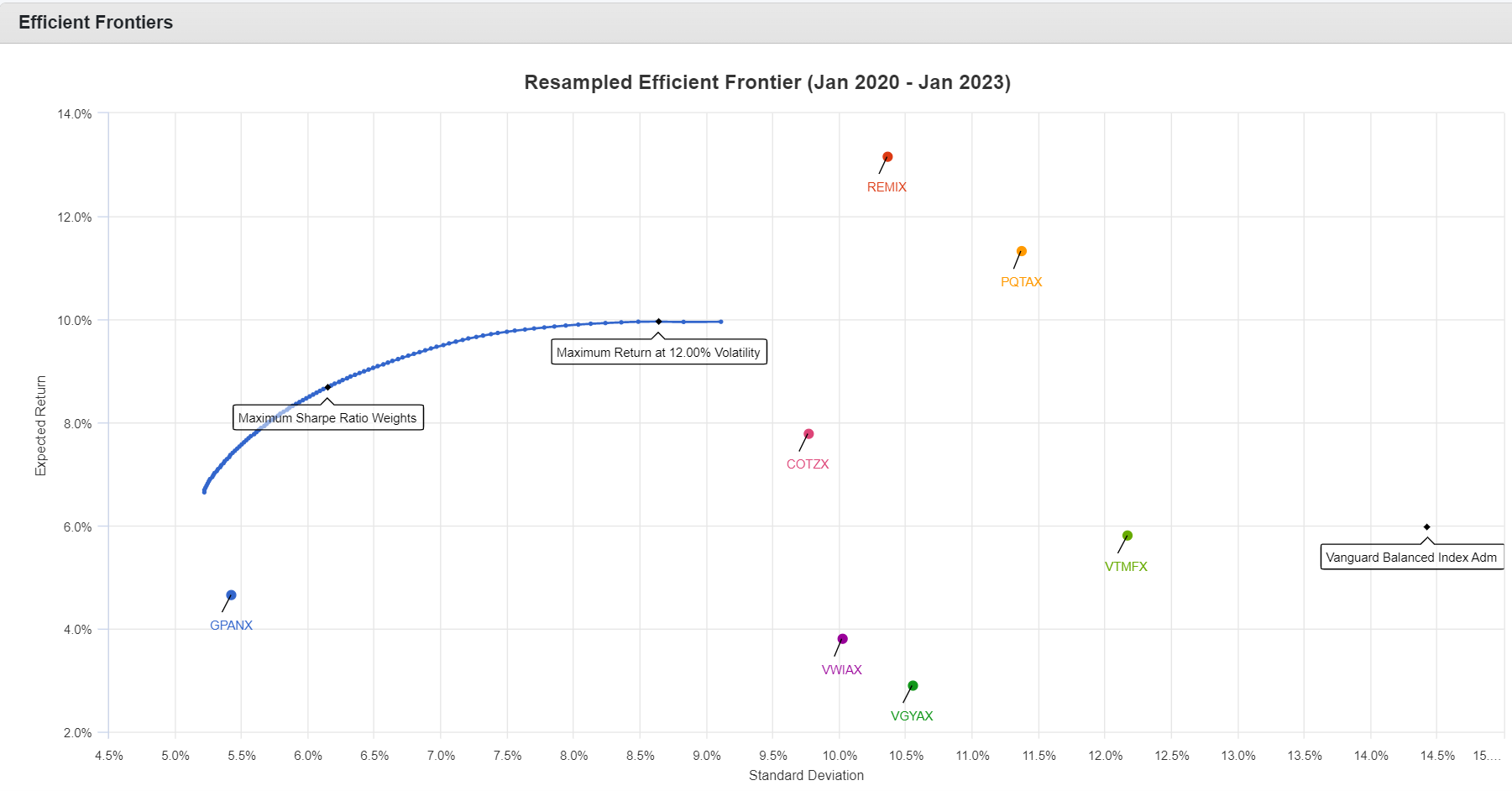

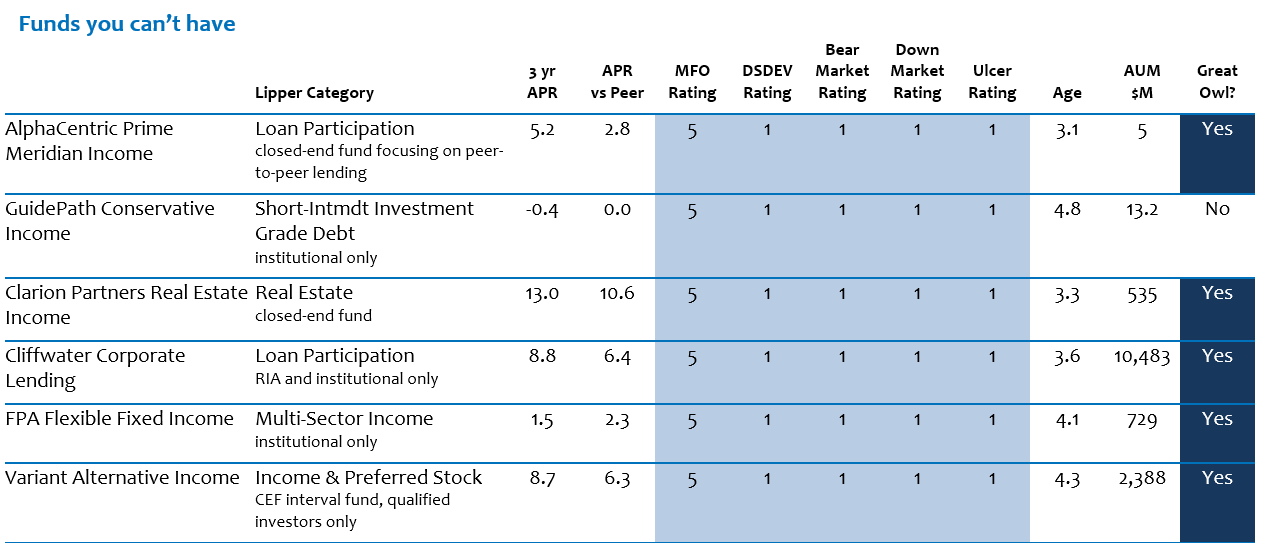

I build off of Lynn’s concerns and, to some extent, his portfolio, in “Two strategies for navigating unstable markets.” It seems likely that the current market euphoria is likely to end … badly … soonly. That said, timing in and out of the market is a disaster for most people who try it (even the ones who swear to their brothers-in-law that they totally killed it in 2022). We searched for funds that proved their ability to protect you in the short term and outperform in the long term. And so we share The Young Defenders – funds under five years old with impeccable risk-return records – and The Wizards – flexible funds that have been making money and protecting investors for a quarter century or more.

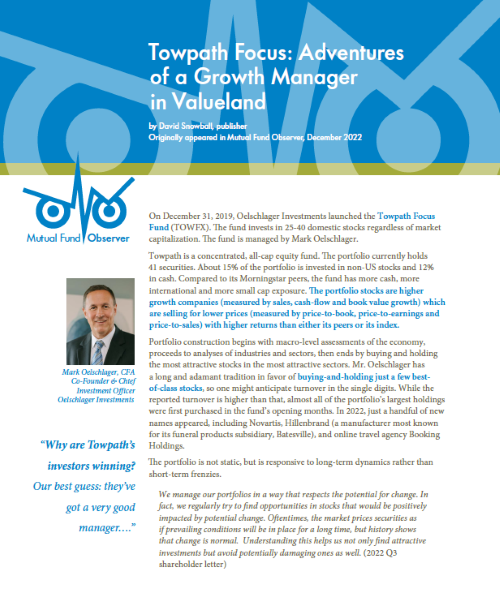

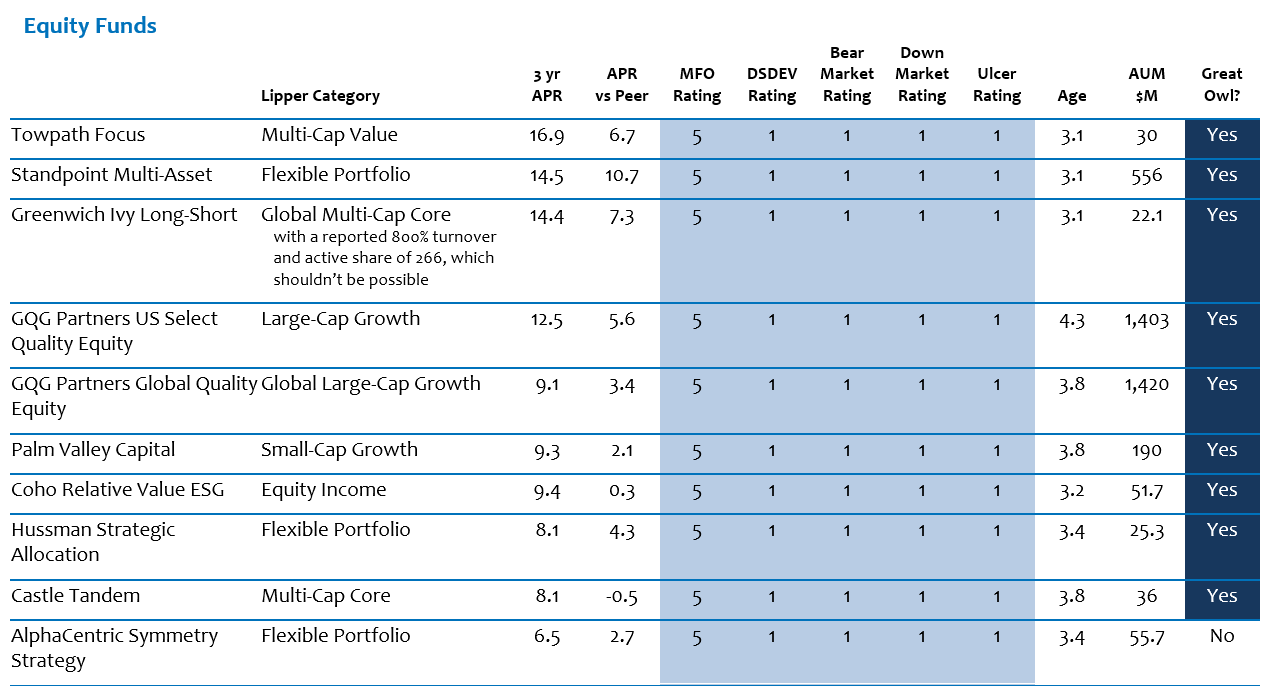

Two funds that we’ve written about recently stand out from The Young Defenders screen: Towpath Focus and Standpoint Multi Asset. We commend them both for your consideration.

|

|

As ever, The Shadow chronicles the endless osmotic process of turning funds into ETFs and living funds and ETFs into mere memories and footnotes, in Briefly Noted.

Finally, one of this issue’s essays was written by one of our robot overlords-in-training, ChatGPT. Increasingly, humans are turning in work completed by chatbots as their own; this includes a flood of fraudulent student papers, the prospect of entire news websites appearing out of thin air, and (lazy) cybercriminals using it to write phishing emails. We wanted to give MFO readers a chance to see what such programs produce, and we offer a short self-defense guide.

Kudos to Ariel Investments

Ariel Investments, adviser to America’s first black-owned mutual fund, celebrated its 40th anniversary by announcing the successful closing of their venture capital fund. “Closing,” in this sense, means “reached their capitalization goal.” Ariel raised $1.45 billion from Qatar’s investment fund and a set of corporate partners – from Amerisource Bergen to Walmart – who each anted up at least $100 million.

The venture capital fund, dubbed Project Black, will seek to invest in six to 10 midsize Black and Latino-owned companies with $100 million to $1 billion in revenue. The vast majority – 95% – of America’s 9.5 million minority-owned enterprises have under $5 million a year in revenue. Ariel believes that their active investment in, and support of, the best of them will allow them to acquire the scale necessary to meet vendor needs for large companies across a range of industries. The success of those businesses will ultimately benefit their employees, their investors, and their communities.

At the same time, Ariel also snagged a large and well-respected emerging markets team from Alliance Bernstein and announced plans to launch a global long/short strategy. Details are in Briefly Noted. More importantly, they’ve updated the turtle in their logo and have adopted the marketing motto, “Active Patience.”

At the same time, Ariel also snagged a large and well-respected emerging markets team from Alliance Bernstein and announced plans to launch a global long/short strategy. Details are in Briefly Noted. More importantly, they’ve updated the turtle in their logo and have adopted the marketing motto, “Active Patience.”

Oh, right … and their funds are very solid. Rupal Bhansali, in particular, has done a fine job leading Ariel Global and Ariel International. One of the most useful and least-used metrics from risk-conscious investors is the Ulcer Index. That index looks at two factors – how far a fund has fallen and how long it took to recover from its fall – to calculate the Ulcer Index. The name derives from the observation that funds that fall less and recover quickly give their investors far fewer ulcers than the others do. So, lower index = fewer ulcers. By that measure, Ms. Bhansali’s funds have far outstripped their peers since inception:

| Fund’s Ulcer Index | Peers’ Ulcer Index | 10 year rank | |

| Ariel Global | 4.2 | 8.8 | #1 of 39 |

| Ariel International | 6.3 | 9.7 | #1 of 50 |

In each case, the fund’s pure returns are “solid” rather than “spectacular,” but they’ve been achieved with exceptional risk management as Ms. Bhansali navigates “a market on opioids.” We profiled Global in 2019.

Snowball’s portfolio: Schwab and Osterweis

With the completion of its TD Ameritrade acquisition, I now have a brokerage account at Schwab. I’ll work hard to learn their system, though my “do something once every couple of years or so” investing style doesn’t warrant much exploration o the intricacies of my (money’s) new home.

One change that is likely to happen in March will be the purchase of shares of Osterweis Strategic Income. My portfolio review in January showed that I was well below my target allocation to bonds. There’s a strong case to be made that bonds are far better investments than stocks just now, but my tendency is to find managers who are flexible, successful, experienced, and risk-conscious. Osterweis seems to fit that to a “T.” Mostly short duration high yield with a dollop of other income-producing securities, from distressed equities to busted convertibles. (No, that’s not a Camaro.)

Lipper (hence MFO Premium) categorizes them as a multi-sector income fund, one of 67 such funds with a track record of at least ten years. Here’s where they stack up against those peers over ten years.

| Annual return | Standard deviation | Sharpe ratio | Ulcer Index | Maximum drawdown | Capture ratio – US bond mkt |

| 5th of 67 | 14th | 5th | 9th | 8th | 3rd |

They have earned MFO’s Great Owl designation for top quintile risk-adjusted performance for the trailing 3-, 5-, 10- and 20-year periods. Morningstar rates it as a four-star fund, though they’re a bit sniffy about the team’s prospects.

It’s not a done deal, but I like their independence, and professionals I trust, trust Osterweis. I’ll do the research and share the results.

Thanks, as ever …

To our stalwart regulars Wilson, S &F Investment Adivsors, Gregory, William, Brian, William, David, and Doug – we thank you. Also, thank you to Dennis from Columbia!

To the folks who have been sharing story ideas and bits of industry news with us. The Shadow and I both appreciate the support and suggestions, and we’ve incorporated what you’ve shared into this month’s Briefly Noted.

As ever,

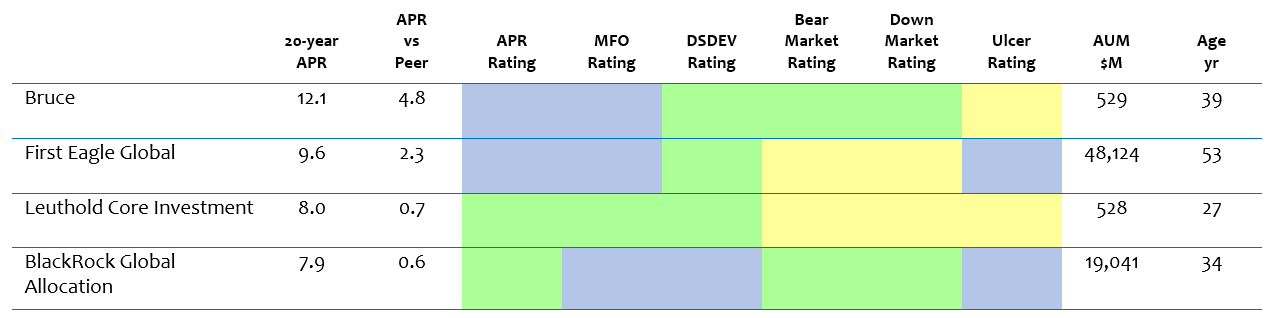

At the other end of the extreme are an even smaller handful of funds that have two virtues. First is the freedom of maneuver. Their managers, by prospectus and discipline, have the ability to change the shape of their portfolios, possibly moving from 90% European equities in one market to a split between short-term bonds and real estate in another. Second is a demonstrable record of getting it right. While a fund’s returns profile changes unpredictably (it’s about impossible to “beat the market” year in and year on), a manager’s risk profile is really consistent. Managers who have a discipline that values absolute returns over relative ones and a willingness to shy away from overpriced assets tend to demonstrate that perspective consistently over time.

At the other end of the extreme are an even smaller handful of funds that have two virtues. First is the freedom of maneuver. Their managers, by prospectus and discipline, have the ability to change the shape of their portfolios, possibly moving from 90% European equities in one market to a split between short-term bonds and real estate in another. Second is a demonstrable record of getting it right. While a fund’s returns profile changes unpredictably (it’s about impossible to “beat the market” year in and year on), a manager’s risk profile is really consistent. Managers who have a discipline that values absolute returns over relative ones and a willingness to shy away from overpriced assets tend to demonstrate that perspective consistently over time.